Finance relies heavily on documents. Invoices, bank statements, loan applications, KYC records, and audit trails are part of everyday operations. This results in a high volume of paper and PDF documents that need to be processed and stored.

For many years, extracting data from these documents required manual effort. Teams had to read each document and enter the data into systems, which was time-consuming and error-prone.

Optical Character Recognition (OCR) changed this process. It allowed financial institutions to automatically read documents and convert scanned images into usable text, reducing the need for manual data entry. This was a major step forward in improving efficiency.

However, OCR has its limits. Teams that have used it over time understand where it works well and where it struggles, especially with complex or unstructured documents.

This guide explains both the strengths and limitations of OCR, and why the industry is now moving toward more advanced document processing approaches.

What Is OCR, and Why Did Finance Adopt It Early?

OCR (Optical Character Recognition) is a technology that reads text from images or scanned documents and converts it into machine-readable, editable data. A scanned invoice becomes a text file. A photograph of an ID card yields a name, date of birth, and document number. A stack of paper bank statements becomes a structured dataset.

Finance adopted OCR early because the math was obvious. Manual data entry is slow, expensive, and error-prone. Automating even a portion of document intake, converting paper to digital at the point of arrival, reduced labor costs and accelerated workflows that the business depended on.

Think of it like a post room that suddenly gained the ability to read. Instead of sorting and handing off documents for someone else to transcribe, the room itself could convert content into usable information before it even reached a desk.

For standardized, high-volume documents on clean paper, printed invoices from known vendors, typed application forms, and machine-generated statements, OCR delivered on that promise consistently.

Where OCR Genuinely Helps in Finance?

OCR performs reliably when used in the right conditions, and its strengths are clear in structured, high-quality document environments. Understanding where it works best helps explain why it became a core part of financial operations.

Accounts Payable and Invoice Processing

High-volume invoice processing is where OCR has historically delivered the clearest ROI. When an organization receives thousands of invoices monthly from a stable set of vendors in consistent formats, OCR can extract vendor names, invoice numbers, amounts, and line items with minimal intervention. Processing time drops from days to hours. Manual keying is eliminated from the intake layer.

Bank Statement Digitization

Converting physical or image-based bank statements into structured transaction data is well within OCR's capabilities, particularly when statements follow a predictable machine-generated format. This is foundational for lending workflows, credit assessments, and financial audits that require historical transaction data at scale.

KYC Document Capture

Know Your Customer (KYC) processes require extracting identity data: names, addresses, identification numbers, dates from passports, national ID cards, and utility bills. For printed, machine-issued documents in good condition, OCR handles this extraction reliably and at speeds that support same-day onboarding workflows.

Audit Trail and Record Digitization

Regulatory compliance often requires digitizing historical records: contracts, correspondence, and financial statements that exist only on paper or in legacy image formats. OCR makes this possible at scale, creating searchable, auditable digital archives without manual transcription.

The Real Limits of OCR in Financial Workflows

Here is where most OCR conversations stop being comfortable. The technology works, but within a narrower range of conditions than financial organizations typically encounter in practice.

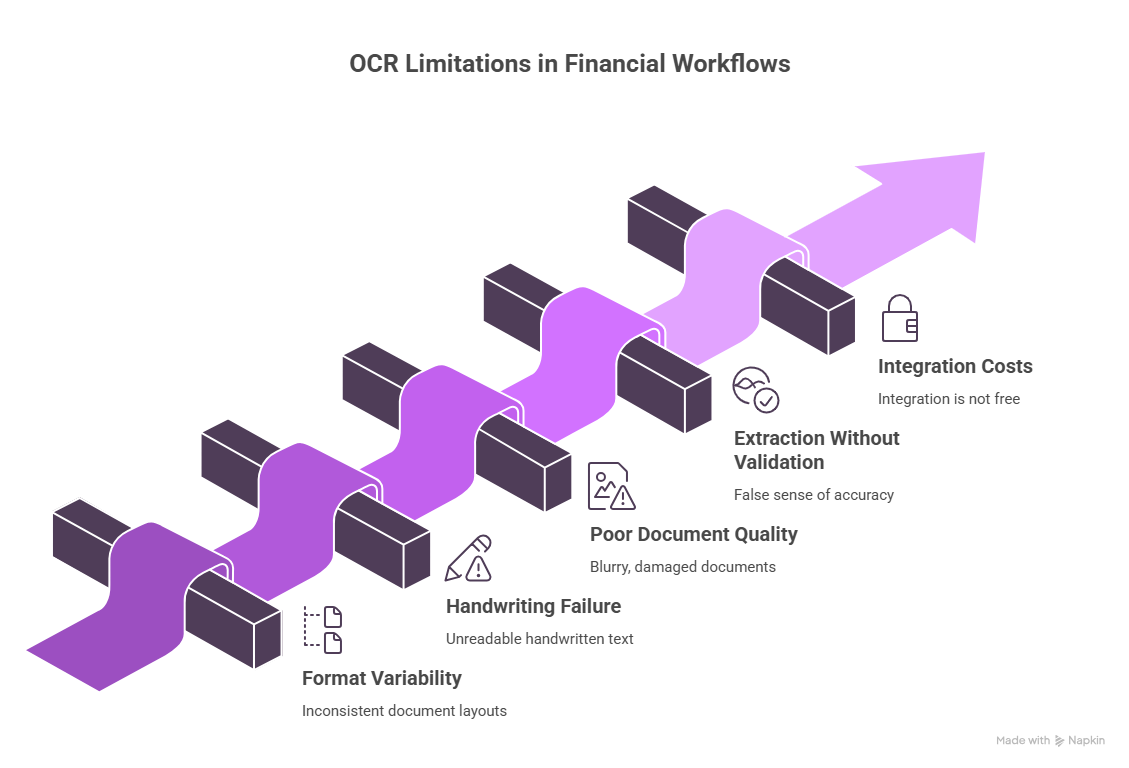

The Format Variability Problem

OCR was built to read. It was not built to understand. When an invoice from a new vendor uses a different layout, different column order, different label names, or different positioning of the total field, traditional OCR either misreads or misroutes the data. It extracted the characters correctly but had no idea what those characters meant in context.

Financial institutions do not work with a fixed set of document formats. A mid-sized AP team may receive invoices from hundreds of vendors, each formatted differently. A lending operation processes applications from borrowers who fill out the same form in entirely different ways. OCR alone cannot bridge that gap.

Handwriting Is a Consistent Failure Point

A significant portion of financial documents still contain handwritten content: loan applications with handwritten notes, claim forms with patient-scrawled signatures and descriptions, and compliance documents with manual annotations. Traditional OCR accuracy on handwriting drops sharply compared to printed text.

In a field where data accuracy directly affects credit decisions, fraud detection, and regulatory compliance, that accuracy gap is not a minor inconvenience. It is a liability.

Poor Document Quality Compounds Every Problem

Documents in financial services arrive from the real world: faxed, photocopied, scanned from aging hardware, photographed on mobile phones, watermarked, stamped, and folded. OCR accuracy degrades meaningfully with image quality. Below a certain resolution threshold, even sophisticated pre-processing cannot recover the data reliably.

The documents most likely to be low-quality are often the most consequential: aged financial records, documents from underserved or remote applicants, and claim forms submitted under emergency conditions.

Extraction Without Validation Creates a False Sense of Accuracy

OCR extracts what it sees. It does not know whether what it extracted is correct. A misread numeral in an invoice total passes through the system as cleanly as an accurate one. Without a validation layer, OCR outputs carry inherent risk that compounds at volume.

Studies across financial services operations consistently show manual document processing error rates of 1 to 2%, which might be a small number but affects significantly on a large scale. OCR reduces that, but without intelligent validation built on top, it does not eliminate it. Teams often discover this the hard way, when downstream reconciliation surfaces errors that made it through the intake layer undetected.

Integration Rarely Comes for Free

OCR converts documents to text. Getting that text into an ERP, a loan origination system, a core banking platform, or a compliance database requires additional work, mapping extracted fields to system fields, handling format mismatches, and building exception queues for values that do not fit. This integration layer is consistently underestimated and frequently becomes the primary implementation cost.

Why These Gaps Matter More Now Than They Did Before?

The volume of documents flowing through financial institutions is not shrinking. In 2024, commercial banks found that they had lost 63% clients due to slow and inefficient onboarding process and KYC, which is up 19% from 2023.

As organizations push for faster loan decisions, real-time KYC, same-day AP processing, and continuous audit readiness, the tolerance for OCR's failure modes decreases. A 10% error rate that was acceptable at 1,000 invoices a month becomes operationally untenable at 50,000.

The limitations of OCR are not flaws in the technology. They are boundaries. OCR was designed to read text from images, and it does that well. The challenge is that financial document processing requires more than reading — it requires understanding, validating, classifying, and routing. That is a different problem.

What Comes Next: Where IDP Picks Up

This is where the conversation shifts. Intelligent Document Processing (IDP) is the category that has emerged to address what OCR alone cannot do. It is not a replacement for OCR; it incorporates OCR as its foundational extraction layer. What it adds is the intelligence that turns extracted text into reliable, actionable data.

The distinction matters. OCR reads. IDP understands.

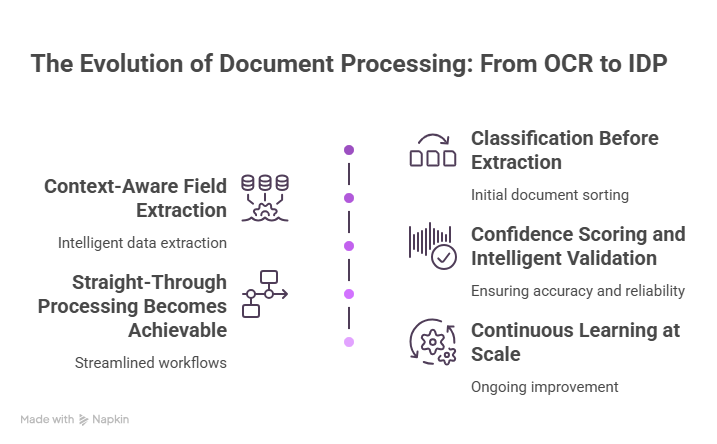

Classification Before Extraction

IDP systems classify documents before attempting extraction. When a batch of documents arrives, a mix of invoices, bank statements, and identity documents, an IDP platform identifies what each document is before applying extraction logic. This means the right model handles each document type, rather than applying a single template that breaks on anything unexpected.

Context-Aware Field Extraction

Rather than reading characters in sequence, IDP uses AI models trained on financial document types to locate and extract specific fields based on meaning, not just position. It recognizes that "Total Due," "Amount Payable," "Balance," and "Net Amount" all refer to the same field across different invoice formats and extracts accordingly.

Confidence Scoring and Intelligent Validation

Every field extracted by an IDP system carries a confidence score. High-confidence extractions pass through automatically. Low-confidence values are flagged for human review, not the whole document, just the specific field in question. This targeted exception model means reviewers touch only what genuinely needs attention.

Straight-Through Processing Becomes Achievable

When extraction is accurate and validation is automated, documents can move from intake to system entry without any human involvement. For high-volume, standardized document types, a common scenario in AP, trade finance, and bank statement processing, this means straight-through processing rates that were simply not achievable with OCR alone.

Continuous Learning at Scale

IDP models improve with volume. Every document the system processes, including exceptions reviewed by humans, becomes a training signal that refines future extraction accuracy. Over time, the system gets better at the specific document types and formats that the organization handles most, rather than staying static at its initial deployment accuracy.

OCR vs. IDP: Understanding the Capability Gap

The table above is not an argument against OCR. It is a map of when OCR is sufficient and when the problem requires more. For organizations processing clean, standardized documents at moderate volume, OCR remains a reasonable solution. For organizations dealing with format variability, handwritten content, regulatory validation requirements, and growing document volumes, IDP is where the calculus changes.

How Infrrd Bridges OCR and Intelligent Document Processing for Finance

Infrrd's IDP platform is built for financial organizations that have outgrown what traditional OCR can deliver. It combines advanced OCR with AI-powered classification, extraction, validation, and integration into a single, cohesive workflow, purpose-built for the complexity of financial document environments.

Accuracy That Holds Across Document Variability

Infrrd handles the full range of financial documents: invoices, bank statements, KYC packs, loan applications, and insurance claim forms, without requiring separate template configurations for every format variant. Extraction accuracy is consistent, including on semi-structured and variably formatted documents that defeat template-based OCR systems.

Exception Management That Targets the Right Documents

Infrrd's confidence scoring model ensures that human reviewers only see the extractions that genuinely need attention. Rather than routing every document through a manual queue, the platform surfaces only the specific fields that fall below confidence thresholds, leaving the rest to move through automatically. Finance teams spend their review time where it actually matters, not on documents the system already handled correctly.

Pre-Built Models for Core Financial Workflows

Infrrd offers pre-configured extraction models for accounts payable, mortgage processing, KYC compliance, trade finance, and audit documentation. Rather than building extraction logic from scratch, finance teams can deploy against real document volumes in weeks. The models continue improving as they process more documents from that organization's specific document landscape.

Compliant Architecture for Regulated Environments

Infrrd is built with enterprise-grade security at its foundation. The platform holds SOC 2 Type II certification, supports GDPR-aligned data practices including regional hosting options and EU data subject rights, and maintains end-to-end encryption, role-based access controls, and complete audit logging across every extraction event.

Finance teams that deploy Infrrd move from OCR as a fragile intake tool to IDP as a reliable operational backbone with measurable gains in processing speed, cost efficiency, and data accuracy from the first quarter of production.

Case Study

State National partnered with Infrrd to automate document-intake and data extraction, which helped in reducing processing time, error rates, and cost without increasing headcount. With advanced adaptability and learning from massive variation. Infrrd’s OCR helped to automate data extraction with maximum accuracy and ease.

To know more about this digital transformation of State National, visit: Beyond OCR Data Extraction

Summary

OCR earned its place in financial services by solving a real problem: getting data off documents and into systems faster than human hands could. For clean, structured, standardized document types, it still delivers. But financial document environments are rarely that clean or that standardized for long.

The organizations hitting the ceiling of what OCR can do are not dealing with a technology failure. They are dealing with a scope problem. OCR reads. What modern financial document processing requires is a system that reads, understands, validates, and learns.

That is what Intelligent Document Processing is for and why the industry is moving toward it, not as a replacement for OCR, but as its necessary evolution.

FAQs About OCR in Finance

What is OCR in finance?

OCR in finance refers to Optical Character Recognition technology used to convert financial documents: invoices, bank statements, KYC forms, and loan applications from image or PDF format into machine-readable digital data, eliminating the need for manual data entry at the intake layer.

Where does OCR work best in financial services?

OCR performs most reliably on high-volume, standardized document types with clean, printed text, machine-generated bank statements, invoices from recurring vendors, and government-issued identity documents in good condition. Performance degrades with handwriting, format variability, and poor image quality.

Why does OCR fail on some financial documents?

Traditional OCR reads characters but does not understand context. When document formats vary, with different invoice layouts, mixed handwritten and printed content, and low-resolution scans, OCR extraction accuracy drops significantly. Without classification and validation logic built on top, it also has no way to detect or flag the errors it produces.

What is the difference between OCR and IDP in finance?

OCR is the character recognition layer that converts document images to text. Intelligent Document Processing (IDP) incorporates OCR as its foundation and adds AI-based document classification, context-aware field extraction, confidence scoring, validation, and continuous learning. IDP is what makes OCR reliable at scale across variable document types.

Can OCR handle handwritten financial documents?

Traditional OCR handles handwriting poorly, particularly across different styles and languages. AI-powered IDP platforms with dedicated handwriting recognition models perform significantly better, though accuracy still varies by document quality and handwriting legibility.

What is straight-through processing, and how does OCR relate to it?

Straight-through processing (STP) means a document moves from intake to system entry without any human involvement. Traditional OCR can support STP for clean, highly standardized documents, but breaks down on variability. IDP makes STP achievable across a much broader range of document types by adding classification, intelligent extraction, and automated validation.

How accurate is OCR for invoice processing in finance?

On clean, consistently formatted invoices from known vendors, OCR performs well at the character extraction level. AI-powered IDP systems go further, handling new vendor formats, validating extracted values against business rules, and routing exceptions intelligently rather than passing errors downstream.

Häufig gestellte Fragen

IDP verarbeitet effizient sowohl strukturierte als auch unstrukturierte Daten, sodass Unternehmen relevante Informationen aus verschiedenen Dokumenttypen nahtlos extrahieren können.

IDP nutzt KI-gestützte Validierungstechniken, um sicherzustellen, dass die extrahierten Daten korrekt sind, wodurch menschliche Fehler reduziert und die allgemeine Datenqualität verbessert wird.

IDP (Intelligent Document Processing) verbessert die Audit-QC, indem es automatisch Daten aus Kreditakten und Dokumenten extrahiert und analysiert und so Genauigkeit, Konformität und Qualität gewährleistet. Es optimiert den Überprüfungsprozess, reduziert Fehler und stellt sicher, dass die gesamte Dokumentation den behördlichen Standards und Unternehmensrichtlinien entspricht, wodurch Audits effizienter und zuverlässiger werden.

IDP kombiniert fortschrittliche KI-Algorithmen mit OCR, um die Genauigkeit zu erhöhen und ein besseres Verständnis des Dokumentenkontextes und komplexer Layouts zu ermöglichen.

Ja, IDP kann Daten aus gescannten Urkunden, Immobilienprüfungsberichten und Steuerdokumenten extrahieren und sie zur weiteren Analyse in strukturierten Formaten organisieren.

IDP bezieht sich auf den Einsatz von KI, maschinellem Lernen und OCR zur Automatisierung der Extraktion, Klassifizierung und Verarbeitung von Daten aus verschiedenen Dokumenttypen wie PDFs, Bildern und gescannten Dokumenten.