Insurance companies process thousands of documents and transactions daily, from policies and claims to inspection reports and customer forms, with each document passing through multiple systems before a decision is reached. Every manual step in this chain slows the process down and increases the likelihood of errors.

Straight-through processing addresses this by automating data movement across systems, applying validation rules, and reserving human involvement only for exceptions. For many insurers, it has become the foundation of modern operations — driving faster decisions, better customer experiences, and measurably lower operational costs.

Industry research highlights the potential that remains. A report from McKinsey found that up to 95% of insurance policies could pass through underwriting without human involvement when supported by advanced analytics and automation.

Despite this opportunity, most insurers have yet to achieve high STP rates. Documents still arrive in different formats, many systems operate in isolation, and data often requires manual verification.

This guide explains how straight-through processing insurance works, where it applies, and how insurers move toward higher automation rates.

What Is Straight Through Processing In Insurance?

Straight-through processing (STP) in insurance refers to the automation of end-to-end insurance workflows without human intervention. Data moves automatically from input to final decision through integrated systems and rules.

The system captures incoming documents or digital data, extracts relevant fields, validates information, and processes the transaction. Human reviewers only examine cases that require clarification or additional information.

Straight-through processing helps insurers reduce delays, minimize errors, and increase operational efficiency.

Examples Of Straight Through Processing In Insurance

Several insurance workflows already support partial straight-through processing (STP), especially in digital policy issuance.

For example, a customer applies for an insurance policy by filling out an online form and uploading required documents such as identity proof, income details, or medical information. Once the submission is complete, automated systems capture the data from these inputs and validate it against predefined rules.

The system checks eligibility based on factors such as age, location, and policy criteria. It also evaluates risk using available data and applies pricing models to determine the premium. If all inputs fall within acceptable thresholds and no exceptions are detected, the system proceeds without manual intervention.

In this case, the platform automatically processes insurance application forms with high-level speed and accuracy. Human review is only required if the system identifies missing information, inconsistencies, or higher-risk cases that fall outside standard rules

Claims processing offers another example. When a policyholder submits a claim with clear documentation and matching policy details, automated systems extract and verify coverage and process payment.

Types Of Insurance Processes Suitable For Straight-Through Processing

Not every workflow fits full automation immediately. However, several processes show strong potential for straight-through processing in insurance. These processes typically share common characteristics like standardized inputs, consistent decision rules, and predictable outcomes, which makes them well-suited for end-to-end automation with minimal human intervention.

Challenges Of Straight Through Processing In Insurance

While automation promises greater efficiency, several obstacles continue to slow its adoption across the insurance industry. Many insurers still operate on legacy systems that struggle to communicate with newer technologies, leaving data fragmented across multiple platforms.

Beyond infrastructure limitations, the sheer variability of incoming documents, whether they are scanned PDFs, photos, emails, or handwritten forms, makes it difficult for automated systems to consistently extract structured, usable information. When that data arrives with errors or incomplete fields, the system must pause and route the case to a human reviewer, breaking the straight-through flow entirely.

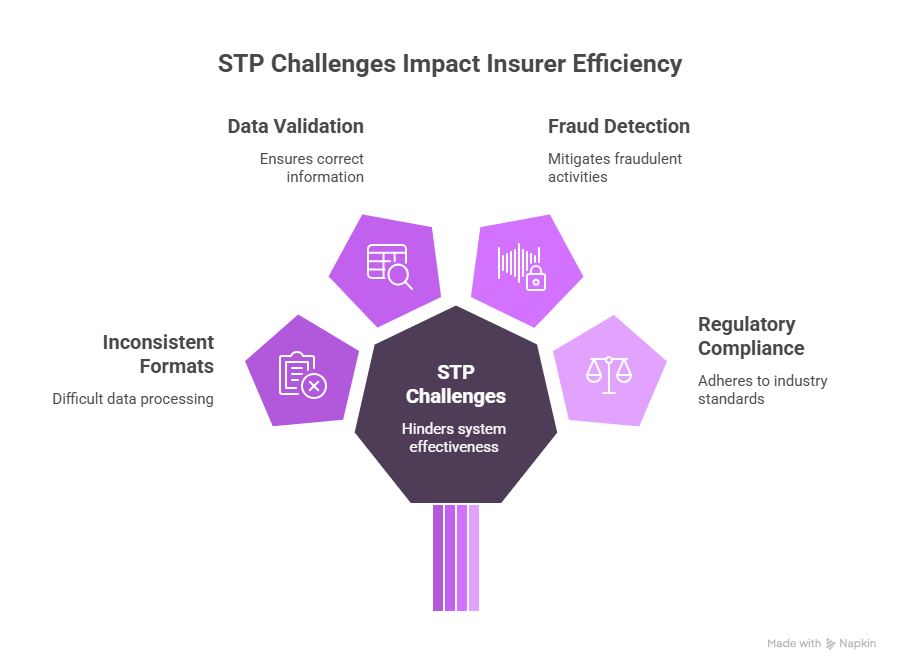

Common Challenges Insurers Face When Implementing STP

Inconsistent Document Formats: Claims reports, repair estimates, and policy documents rarely follow a uniform layout. When document structures vary significantly, automated systems find it difficult to locate and interpret the right information reliably.

Data Validation: Before any claim can be approved or a policy issued, systems must accurately verify policy numbers, coverage limits, and customer details. Even minor discrepancies can trigger manual intervention, slowing down the entire process.

Fraud Detection: Identifying suspicious claims before processing payments adds a meaningful layer of complexity to automation. Systems must be sophisticated enough to flag anomalies without disrupting legitimate cases.

Regulatory Compliance: Insurers are required to maintain detailed records and audit trails for every automated decision made. Meeting these compliance standards while sustaining processing speed remains an ongoing balancing act.

Because of these compounding challenges, most companies achieve partial automation well before reaching full straight-through processing in insurance.

Why Insurance Companies Still Struggle With Straight Through Processing?

Despite significant investment in automation, most insurers find themselves navigating a web of document challenges, disconnected systems, and data quality issues that collectively prevent end-to-end automation from becoming a reality. Understanding these obstacles is the first step toward addressing them effectively.

Insurance Document Variations

Despite major advances in automation technology, many insurers continue to process large volumes of transactions manually. A significant part of this comes down to the document-heavy nature of insurance workflows. Claims frequently arrive bundled with photos, inspection reports, handwritten forms, and invoices; all containing valuable information but lacking the structured formatting that automated systems need to function efficiently. This gap between rich content and machine-readable structure remains one of the most persistent bottlenecks in the industry.

A study examining insurance claims processing found that only about 7% of claims pass through complete straight-through processing without any human involvement. The overwhelming majority require manual review, largely because systems still struggle to interpret and act on unstructured content with sufficient accuracy and confidence.

Integration Across Systems

Beyond document challenges, insurers also face significant friction when connecting the various platforms that underpin their operations. Policy administration systems, claims management platforms, and document repositories often operate in silos. When these systems fail to communicate smoothly with one another, automation pipelines slow down or break entirely, forcing staff to bridge the gaps manually.

Data Quality

Even well-integrated systems are vulnerable to poor data quality. Missing information, inconsistent entries, or incorrectly formatted fields force automated workflows to pause and await human correction before they can continue. Without clean, complete data flowing in, straight-through processing cannot reach its full potential.

Workflow And Organizational Readiness

Technology alone is not enough. Automation fundamentally changes how employees engage with claims, underwriting files, and customer requests, requiring organizations to rethink internal processes and retrain their teams accordingly. Without this structural adaptation, even the most capable automation tools will underperform in practice.

Taken together, these factors explain why most insurers adopt automation incrementally rather than pursuing full straight-through processing from the outset.

How Straight Through Processing In Insurance Works?

Straight-through processing insurance relies on a sequence of automated steps. Each step moves data through systems without manual entry. Modern insurance platforms combine document processing technology, artificial intelligence models, and workflow automation tools to support this flow.

Step 1: Data Ingestion And Document Capture

The process begins the moment the system receives data from any one of several entry points. Customers may submit documents through digital portals, mobile applications, or email, while insurers also capture incoming files directly from partner systems such as repair shops or healthcare providers. Regardless of the source, the system automatically organises all incoming files and prepares them for the next stage of processing.

Step 2: Data Extraction And Validation

Once documents have been captured, extraction technology goes to work identifying the relevant data fields within each file. These fields typically include policy numbers, customer information, claim descriptions, and financial values.

Advanced document processing tools are capable of reading both structured and unstructured content, pulling information from standard forms, scanned documents, and images alike. The extracted data is then cross-referenced against internal records, with validation rules confirming policy status, coverage limits, and claim eligibility before the workflow can proceed.

Automated Decision Workflows

With validation complete, decision engines take over and apply a set of predefined business rules to determine the appropriate outcome. A system might, for instance, automatically approve a claim if the payout value falls below a specified threshold and all relevant policy conditions satisfy the eligibility criteria.

When every rule is met, the system advances the case through the pipeline without any need for manual review, keeping the process both fast and consistent.

Exception Handling And Human Review

Not every transaction is straightforward enough to qualify for full automation. When the system encounters missing information, unusual patterns, or policy conflicts that fall outside its predefined rules, it flags the case and routes it to a human reviewer for closer examination. Reviewers analyse these exceptions and make the final call where automated judgment falls short. This hybrid model allows insurers to progressively expand their use of straight-through processing while preserving the operational oversight needed to handle complexity responsibly.

Insurance Workflows That Can Be Automated With STP

Insurance companies manage workflows that depend on repeated data entry, document handling, and rule-based validation. Because these tasks follow predictable structures, many of them are well-suited for straight-through processing when paired with the right automation technology. The result is faster turnaround times and higher transaction volumes without a proportional increase in staffing.

Claims Processing Automation

Claims processing is one of the most impactful areas for straight-through processing in insurance. Traditionally, staff manually reviewed claim forms alongside supporting documents such as photos, invoices, and repair estimates before entering data into claims systems. Automation replaces this by extracting relevant fields, verifying policy coverage, and applying eligibility rules automatically. When all conditions are met, the system approves the claim and triggers payment without human involvement.

Research indicates that combining artificial intelligence with robotic process automation can increase straight-through processing rates by approximately 25% while reducing claims cycle times by roughly 45% — allowing insurers to process more claims faster while maintaining full operational control.

Underwriting Automation

Underwriting has traditionally relied on manual review of customer applications and supporting documentation to evaluate risk. Straight-through processing automates a significant portion of these decisions, particularly where risk parameters are predictable and data inputs are standardised. Low-risk policies such as travel insurance move through the system without underwriter involvement, while more complex cases are routed to human review, allowing underwriters to focus their expertise where it matters most.

Policy Issuance And Renewal Automation

When customers submit information through digital portals, systems can verify identity, confirm coverage, and validate eligibility without manual input. Once complete, the platform generates policy documents automatically and stores them in the relevant systems. Renewals follow a similar path; if the customer record and risk conditions remain stable, the policy renews automatically. Both processes reduce administrative overhead and shorten turnaround times considerably.

Insurance Document Processing

Insurance operations generate large volumes of documents, including claim forms, inspection reports, invoices, and policy records. Document processing tools read incoming files, extract relevant data fields, and transfer that information directly into the appropriate systems. While structured digital forms are straightforward to automate, advanced processing systems are also capable of interpreting unstructured content, making them a foundational component of any STP strategy.

Technologies That Enable Straight Through Processing

Several technologies work in concert to enable straight-through processing in insurance, each addressing a different stage of the workflow. Together, they form a connected automation environment capable of moving information reliably across systems from start to finish.

Intelligent Document Processing (IDP)

Intelligent Document Processing sits at the core of STP adoption in insurance. IDP systems extract information from claims forms, invoices, inspection reports, and policy records, converting document content into structured formats that downstream automation platforms can readily process. By eliminating manual data entry at the document stage, IDP prepares transactions for automated workflows from the very first step.

Artificial Intelligence And Machine Learning

Artificial intelligence enables systems to apply decision rules with far greater sophistication than traditional rule engines. Machine learning models analyse historical data to identify patterns in claims behaviour and underwriting outcomes, supporting more accurate validation and stronger fraud detection. AI also improves document interpretation accuracy over time by continuously learning from past examples.

Workflow Orchestration And APIs

Workflow automation tools define and coordinate every step of an insurance transaction, from document capture and data extraction through to validation, approval, and payment. Application programming interfaces complement this by enabling different systems to exchange data in real time, connecting policy platforms, claims systems, and customer portals into a unified operational environment.

Core System Integrations

For straight-through processing to work effectively, policy administration systems, claims management platforms, and document repositories must communicate seamlessly with one another. This integration allows automation platforms to retrieve policy details, validate claim data, and update records without manual intervention. Where integration is absent, automation workflows stall, and the efficiency gains of STP are significantly diminished.

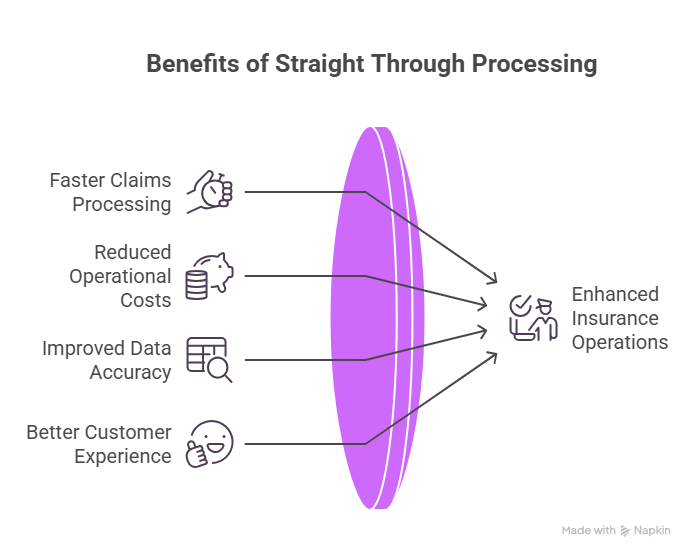

Benefits of Straight Through Processing in Insurance

Straight-through processing delivers measurable improvements across multiple operational dimensions, from speed and cost reduction to data accuracy and customer experience. The benefits extend well beyond simple efficiency gains and compound as automation scales across the business.

Faster Claims Processing

Automated claims processing significantly shortens decision times, allowing customers to receive faster responses and quicker payouts. This directly reduces claim backlogs and raises customer satisfaction levels across the board.

Reduced Operational Costs

By automating routine transactions, insurers can manage growing workloads without a proportional increase in headcount. The cost savings are meaningful and continue to scale as transaction volumes rise over time

Improved Data Accuracy

Automated extraction and validation rules detect inconsistencies and verify information before any transaction is completed, eliminating the transcription errors that manual data entry inevitably introduces. Higher data quality improves reporting reliability and reduces operational disputes.

Better Customer Experience

Automation enables insurers to respond promptly to policy requests and claims submissions while keeping customers better informed through timely updates. Faster, more transparent service builds trust and contributes to stronger long-term customer relationships.

How Insurance Companies Can Implement STP Successfully?

Successfully implementing straight-through processing requires careful planning, honest assessment of existing workflows, and a disciplined approach to gradual deployment. Organisations that approach STP strategically are far better positioned to realise its full potential.

Assessing Automation Readiness

The first step is a thorough analysis of current workflows to identify processes that rely on repetitive tasks, structured inputs, and consistent decision rules. These represent the strongest candidates for automation and form the foundation of a prioritised and realistic implementation roadmap.

Selecting The Right Automation Platform

Insurers should evaluate technology providers on their ability to handle document-heavy workflows, integrate with existing systems, and scale as transaction volumes grow. The right platform should complement existing operations rather than disrupt them.

Running Pilot Implementations

A focused pilot program allows teams to measure real performance improvements, surface operational challenges early, and refine workflows and validation rules before broader deployment. The insights gained at this stage are invaluable for informing enterprise-wide rollout decisions.

Scaling Automation Across Insurance Workflows

With a successful pilot in place, insurers can extend automation progressively across underwriting, policy renewals, customer onboarding, and claims processing. Scaling gradually allows organisations to manage operational risk while steadily increasing efficiency across the business.

How Infrrd Helps Achieve Straight Through Processing In Insurance

Straight-through processing insurance depends heavily on the ability to interpret documents and convert them into structured data. Infrrd focuses on automating document-heavy workflows that appear across insurance operations.

Automating Document-Heavy Insurance Workflows

Insurance documents contain critical information required for claims decisions, underwriting assessments, and policy processing. Infrrd processes these documents and extracts relevant fields so systems can process transactions automatically. This automation reduces manual data entry and prepares transactions for automated workflows.

Improving STP Rates Using AI-Driven Data Extraction

Unstructured documents often prevent full automation. Inspection reports, invoices, and handwritten forms require advanced processing technology. Infrrd interprets these documents and converts them into structured data that automation systems can validate and process. As a result, insurers can increase straight-through processing insurance rates across claims and policy workflows.

Enabling No-Touch Document Processing

Automation platforms often require manual intervention when document data remains unclear.

Infrrd reduces these interruptions by extracting and validating document information before workflows begin. This capability allows insurance systems to process more transactions automatically and reduces the number of cases routed for manual review.

Conclusion

Achieving high straight-through processing rates is no longer a luxury, it is the baseline for insurance competitiveness in 2026. By integrating Intelligent Document Processing and AI-driven workflows, insurers can finally bridge the gap between fragmented legacy data and rapid, "no-touch" decision-making. Transitioning to STP doesn't just lower operational costs; it fundamentally transforms the customer experience by turning weeks of waiting into minutes of clarity. As automation technology continues to evolve, the insurers who prioritize seamless data flow today will lead the market tomorrow.

FAQs About Straight Through Processing in Insurance

What Is Straight-Through Processing In Insurance?

Straight-through processing in insurance refers to workflows that move insurance transactions from input to final decision through data extraction, capture, and validation steps. Systems collect information from submitted documents, validate it against predefined rules, and complete the transaction based on those conditions. Human review is required only for exceptions, such as missing information or data that falls outside defined thresholds.

What Insurance Processes Can Use STP?

Several insurance workflows support straight-through processing. These include claims processing, policy issuance, underwriting decisions, policy renewals, and customer onboarding processes.

What Is The Difference Between STP And Manual Insurance Processing?

Manual processing requires staff to review documents, enter data, and approve transactions. Straight-through processing insurance automates these steps through integrated systems and validation rules.

What Technologies Enable Straight-Through Processing?

Key technologies include intelligent document processing, artificial intelligence models, workflow automation platforms, and system integrations that connect insurance applications.

What Is A Typical STP Rate In Insurance?

STP rates vary across insurance companies and workflows. Some simple claims achieve high automation rates, while complex claims require human review. Industry research indicates full automation remains limited for many claim types.

Why Do Insurers Struggle To Achieve Full Straight-Through Processing?

Several factors limit automation adoption. Insurance documents often contain unstructured content. Legacy systems also restrict integration between platforms. Data quality issues may require manual verification. Automation technologies continue to improve these limitations, allowing insurers to increase STP rates gradually.