Mortgage lending is document-intensive. A single loan file can include hundreds of pages. For decades, processors manually entered data and cross-checked figures, a process that is slow, costly, and difficult to scale.

Intelligent mortgage processing solves this by using AI to automatically extract data, validate information across documents, and flag exceptions for human review. The result is faster processing times, lower operational costs, and higher document accuracy, with less manual effort across underwriting, quality control, and audits.

Industry data also reflects the growing importance of automation in mortgage operations. According to research from nCino, 97% of mortgage lenders plan to implement intelligent automation, yet only 14% have achieved full enterprise-wide deployment close that gap with the AI mortgage document processing guide and implementation resource. Another 81% of lenders are currently working on intelligent automation initiatives, highlighting a major gap between adoption intent and operational execution.

What Is Intelligent Mortgage Processing?

Intelligent mortgage processing refers to the use of artificial intelligence and document automation to read mortgage files, extract information, verify document data, and prepare loan files for review.

The system analyzes documents such as bank statements, pay stubs, tax forms, disclosures, and appraisal reports. It identifies important data fields and converts them into structured data that systems can process.

Traditional processing requires employees to read documents line by line. Intelligent mortgage processing uses AI to perform most of this work automatically. The platform then sends only exceptions or unusual cases to human reviewers.

This model reduces manual work while improving consistency and accuracy.

Where it Fits in Mortgage Workflows?

Mortgage lending is a multi-stage process, and each stage carries its own document review and data verification requirements. A typical mortgage workflow moves through loan application intake, document collection, income and asset verification, underwriting preparation, compliance validation, quality control review, loan closing, and post-close audits. At every one of these stages, teams must check documents and confirm borrower information, making the overall process highly labor-intensive by nature.

Intelligent mortgage processing supports each of these stages by automating the document tasks that would otherwise consume the most time and effort. Rather than acting as a single-point tool, the technology works across the entire loan lifecycle, reducing manual work at every step along the way.

During document intake, for instance, the system automatically sorts incoming files and routes them into the correct loan categories, eliminating the need for processors to manually organize each submission. As the file moves into underwriting preparation, the platform extracts key borrower data and presents it in a structured format that is ready for review, saving underwriters significant setup time. By the time the file reaches quality control, the system has already begun comparing data across documents, flagging any inconsistencies where borrower information does not align across forms.

This end-to-end automation means that mortgage teams are not simply saving time at one point in the process; they are building efficiency into the loan lifecycle from the moment a file enters the pipeline to the final post-close audit.

Difference Between Mortgage Automation and Intelligent Processing

Both technologies improve mortgage operations, but they serve different purposes, and the distinction matters because most mortgage work centers on documents, not workflow actions.

Together, the two technologies work best in combination with automation, managing file movement and system updates, while intelligent processing handles what is actually inside those files.

Why Intelligent Mortgage Processing Matters in 2026?

Mortgage lenders face rising pressure from borrowers, regulators, and investors. These pressures drive interest in intelligent processing technologies. Several industry trends explain this shift.

Rising Document Complexity in Loan Files

Mortgage documents vary widely in format and structure, arriving from employers, financial institutions, and government agencies. A typical loan file includes pay stubs, bank statements, W-2 forms, tax returns, employment verification letters, property appraisals, mortgage disclosures, and closing statements, each carrying critical borrower data that must align across the entire file.

Confirming that numbers match across these varied documents is where manual review becomes a bottleneck. Employees must open each file individually, locate the relevant fields, and verify the values by hand, which is a time-consuming process that grows harder as document volumes increase. Intelligent mortgage processing eliminates much of this friction by automatically identifying data fields and organizing information for review, allowing teams to handle larger loan volumes without a proportional increase in effort.

Faster Loan Turnaround Expectations

Borrowers today expect mortgage approvals to move quickly, largely because online lenders and digital platforms have raised the bar across the industry. Yet research shows that closing a conventional mortgage still takes around 47 days on average, with up to 60% of that time consumed by collecting, reviewing, and verifying borrower documents alone.

Intelligent mortgage processing directly targets this bottleneck, which is why teams invest in intelligent mortgage processing systems to scale operations. The system reads documents immediately after upload, extracts borrower data, and validates information across files, delivering processors a prepared loan file rather than a stack of raw documents. Underwriters can begin risk evaluation earlier in the process, and shorter document review cycles translate into faster approvals, helping lenders stay competitive without overburdening their teams.

Compliance and Audit Pressures

Mortgage lending operates under strict regulatory oversight, with lenders required to follow guidelines from agencies such as Fannie Mae, Freddie Mac, and federal regulators. Every loan file must contain accurate, complete documentation because missing pages or mismatched borrower data can create serious compliance exposure.

Manual review is not always reliable enough to catch these issues before they become problems. Intelligent mortgage processing strengthens this layer of oversight by automatically comparing information across documents and flagging missing files, mismatched data, and inconsistent borrower details in real time. Mortgage teams can resolve discrepancies before the loan advances, improving compliance readiness and significantly reducing risk when files come under audit scrutiny.

How Intelligent Mortgage Processing Works?

Intelligent mortgage processing combines several technologies to automate document workflows. Each component performs a specific function in the processing pipeline.

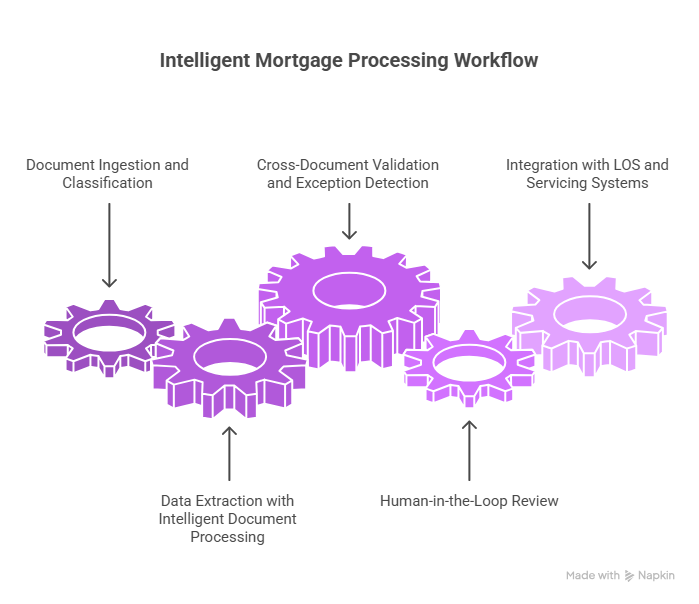

Step 1: Document Ingestion and Classification

Mortgage documents enter systems through multiple channels, like borrower portals, email attachments from loan officers, and third-party services delivering credit reports or appraisal data. Once collected, the platform analyzes each file and uses artificial intelligence to identify its document type based on structure and content, distinguishing between bank statements, tax returns, pay stubs, and more.

The system then organizes these files directly within the loan record. This automatic classification eliminates hours of manual document sorting, ensuring every file lands in the right place from the moment it enters the pipeline.

Step 2: Data Extraction with Intelligent Document Processing

Once documents are classified, the platform extracts key data fields, which include borrower name, employer name, income values, bank balances, property details, and loan amounts, and converts them into structured data ready for underwriting or compliance checks.

Unlike traditional OCR, which struggles with document variation, intelligent document processing uses machine learning models that understand document structure and locate relevant fields even when formats differ. This capability significantly improves extraction accuracy across large, varied document sets.

Step 3: Cross-Document Validation and Exception Detection

Mortgage files frequently report the same data across multiple documents, like income figures that appear in tax returns, pay stubs, and employment letters, while bank balances surface in both asset statements and loan applications. The platform automatically compares these values and marks matching fields as verified. Where discrepancies exist, the system flags the case as an exception for processor or underwriter review. This targeted approach means teams focus their attention only where it is needed, helping lenders detect errors early and maintain data accuracy throughout the loan file.

Step 4: Human-in-the-Loop Review

Automation handles the majority of document tasks, but human judgment remains essential. Some documents arrive as low-quality scans or handwritten forms that fall outside standard processing parameters. In these cases, the system routes files to human reviewers, who verify the data and correct any errors before the loan moves forward. This human-in-the-loop model strikes the right balance; routine work flows through automation while professionals handle the exceptions, which improves overall efficiency without removing the oversight that mortgage operations require.

Studies on document automation show that automated document processing can reduce human error rates by up to 90% and speed document workflows by roughly four times compared to manual processing methods, making it highly valuable for document-heavy industries such as mortgage lending.

Step 5: Integration with LOS and Servicing Systems

Mortgage lenders depend on multiple enterprise platforms, including loan origination systems for managing applications and servicing systems for handling payments and escrow accounts. Intelligent mortgage processing integrates directly with these platforms, pushing extracted data into loan records without requiring manual entry. This eliminates transcription errors and ensures that underwriting, servicing, and quality control teams are all working from the same accurate, up-to-date information, creating a more connected and reliable operational environment across the loan lifecycle.

Mortgage Processes that Benefit from Intelligent Processing

Intelligent mortgage processing delivers measurable value across multiple departments, streamlining document-heavy tasks at every stage of the loan lifecycle.

Loan Origination Document Review

Origination teams collect borrower documents and prepare applications for underwriting. Automation organizes incoming files and extracts key borrower data, giving processors structured information rather than raw documents, which speeds up file preparation and reduces the time it takes to move loans forward.

Underwriting Verification

Underwriters evaluate borrower risk by confirming income stability, employment status, assets, and property details. Intelligent mortgage processing prepares and structures this data in advance, allowing underwriters to focus entirely on risk decisions rather than spending time manually reading through documents.

Post-Close Quality Control

Quality control teams review closed loans for compliance with guidelines. Automation scans the full loan file, verifies document completeness, and flags missing or mismatched items for review, allowing QC teams to complete audits faster and with greater consistency.

Mortgage Servicing Document Handling

Servicing departments manage escrow updates, borrower communications, and loan modifications, all of which require document review. Automation organizes servicing documents and extracts relevant data, giving servicing teams faster access to borrower information and a cleaner document history.

Investor and Regulatory Audits

Investors and regulators require lenders to maintain accurate, complete loan documentation. Intelligent mortgage processing verifies that required documents are present and borrower information is consistent, keeping loan files organized and audit-ready at all times. Industry research also shows that 73% of mortgage lenders consider AI adoption a priority for improving operational efficiency and maintaining competitiveness, indicating that intelligent processing technologies are becoming central to mortgage operations.

Key Challenges in Mortgage Processing

Even with automation in place, mortgage processing continues to face operational obstacles that require careful management.

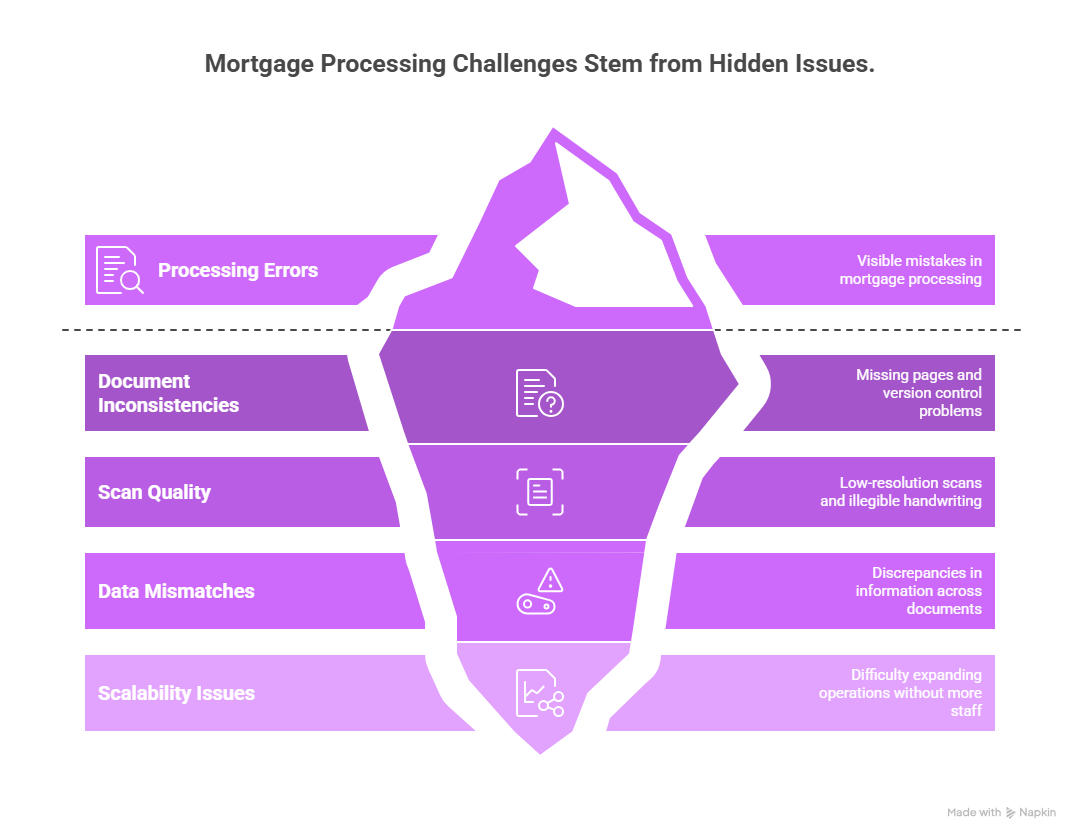

Missing Pages and Inconsistent Document Versions

Incomplete loan files are a common challenge; borrowers may upload only part of a bank statement or submit an outdated disclosure without realizing it. Manual review often misses these gaps. Automation systems detect missing pages and identify outdated forms early in the workflow, allowing processors to resolve issues before they cause downstream delays.

Low-Quality Scans and Handwritten Forms

Borrowers frequently upload documents captured on mobile devices or low-grade scanners, resulting in files with shadows, skewed text, or handwritten content. Traditional OCR tools struggle with these inconsistencies. AI-based processing systems are better equipped to analyze varied document quality and extract readable data more reliably, improving accuracy across the full range of document types a lender is likely to receive.

Data Mismatches Across Documents

Borrower information often appears inconsistently across documents — names may be spelled differently, addresses formatted differently, and financial values may not align between statements and applications. Cross-document validation detects these discrepancies automatically and surfaces them for review, allowing mortgage teams to correct the data before it creates problems during underwriting or compliance checks.

Scaling Mortgage Operations Without Hiring More Staff

Loan volumes fluctuate with market conditions, and peak periods demand faster throughput without the option to rapidly expand headcount. Automation platforms address this directly by enabling existing teams to process higher loan volumes without a proportional increase in staffing costs. Employees shift their focus to high-value tasks while the system handles routine document work.

Implementation Checklist for Lenders

Lenders typically adopt intelligent mortgage processing gradually. A structured implementation plan makes the transition smoother and improves long-term adoption success.

Assess Document Volume and Workflow Complexity

The first step is a thorough analysis of existing workflows. Lenders should measure current document volumes, average processing times, and review workloads across teams. This assessment reveals where bottlenecks are most severe and helps prioritize where automation will deliver the greatest immediate value.

Identify Automation Candidates

Not all mortgage tasks are equal candidates for automation. Repetitive, document-heavy tasks such as classification and data extraction are natural starting points. Identifying these workflows early allows lenders to introduce intelligent mortgage processing where it will have the most immediate and measurable impact.

Pilot Automation with One Loan Workflow

Before a full rollout, a focused pilot project allows teams to evaluate system performance in a controlled environment. Starting with a single use case, such as income verification or document classification, generates measurable results and practical insights that teams can use to refine workflows before broader deployment.

Roll Out Across Origination and QC Teams

Following a successful pilot, lenders can expand automation across additional departments. Origination teams adopt the system for document intake, while quality control teams apply it to loan audits. A gradual, phased expansion supports smoother adoption and gives staff adequate time to build confidence with the new workflows.

ROI of Intelligent Mortgage Processing

Intelligent mortgage processing delivers clear, measurable returns across the key dimensions that matter most to lenders.

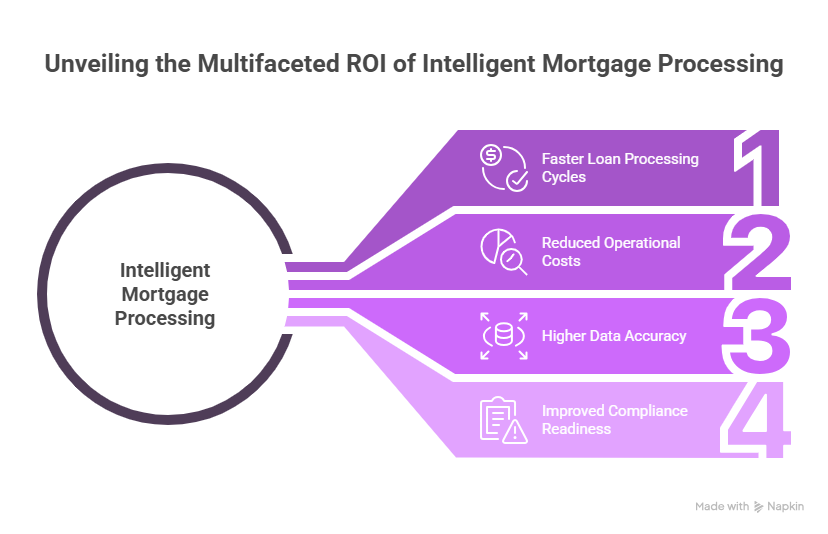

Faster Loan Processing Cycles

Automated document review significantly shortens the time it takes to move loan files through the underwriting and approval stages. By eliminating manual document handling, lenders can compress processing timelines and deliver faster decisions, which is an increasingly important competitive advantage in a market where borrower expectations continue to rise.

Reduced Operational Costs

Automation reduces the volume of manual work required to review and verify documents, allowing mortgage teams to handle higher loan volumes without increasing staffing levels. As productivity rises and labor demands stabilize, operational costs decrease, improving the overall economics of the lending operation.

Higher Data Accuracy

AI systems extract data consistently and apply the same validation logic across every document, eliminating the variability that comes with manual data entry. This consistency reduces errors, strengthens underwriting decisions, and improves the quality of reporting, all of which contribute to a more reliable and defensible loan file.

Improved Compliance Readiness

Automation platforms continuously verify document completeness and data consistency throughout the loan lifecycle. This keeps loan files well-organized and aligned with regulatory and investor expectations at every stage, significantly reducing the risk of compliance gaps when files come under audit scrutiny.

To calculate the ROI for automating your work, check: ROI Calculator

Infrrd’s Approach to Intelligent Mortgage Processing

Infrrd develops intelligent document processing (IDP) technology that supports document-heavy industries such as mortgage lending. The platform focuses on automation, document intelligence, and operational accuracy.

Infrrd has built a focused mortgage suite under the "Infrrd for Mortgage" umbrella, with two flagship products:

- MortgageCheckai: MortgageCheckai sits at the heart of Infrrd's mortgage automation offering. Its primary goal is to take the grunt work off auditors' plates, things like manual data entry and document sorting, so they can spend their time on what actually matters: reviewing and auditing loans.

- Ally: Ally is Infrrd's flagship Agentic AI, designed specifically for the mortgage industry. Unlike conventional processing tools, Ally reasons through complex audit tasks from start to finish, bringing the accuracy and contextual judgment of an experienced human auditor to every loan file it reviews.

Conclusion

Intelligent mortgage processing is no longer a future consideration; it is an operational necessity. As document complexity grows, borrower expectations rise, and regulatory demands tighten, lenders need technology that works across the entire loan lifecycle. By automating document intake, extraction, validation, and compliance checks, mortgage teams can process more files with greater accuracy and far less manual effort. For lenders looking to scale efficiently and stay competitive, intelligent mortgage processing is the foundation worth building on.

FAQs

Q. What is intelligent mortgage processing?

Intelligent mortgage processing uses artificial intelligence and automation to read mortgage documents, extract data, and validate borrower information across loan files.

Q. How does AI improve mortgage loan processing?

AI reads documents, extracts key data fields, and identifies inconsistencies across files. Mortgage teams spend less time reviewing documents manually.

Q. What technologies power intelligent mortgage automation?

Technologies include artificial intelligence, machine learning, intelligent document processing, and workflow automation systems.

Q. How does intelligent document processing help lenders?

Intelligent document processing extracts data from mortgage documents and converts it into structured data for loan systems.

Q. How long does mortgage processing take with automation?

Automation reduces document review time and helps lenders process loan files faster.

Q. What challenges do lenders face with manual mortgage processing?

Manual processing often leads to slower loan approvals, higher labor costs, and increased risk of data entry errors.

Q. What is the role of AI in mortgage underwriting?

AI prepares loan files by extracting borrower data and validating information across documents before underwriting review.

Q. Can intelligent mortgage processing reduce compliance risk?

Yes. Automated document validation helps lenders detect missing documents and data inconsistencies early.

Q. How does cross-document validation work in mortgage automation?

The system compares data fields across documents such as tax returns, pay stubs, and bank statements to detect inconsistencies.

Q. What is the ROI of mortgage document automation?

Lenders benefit from faster processing cycles, lower operational costs, improved data accuracy, and stronger compliance readiness.

Q. How do lenders implement intelligent mortgage processing systems?

Lenders begin by identifying document-heavy workflows, running pilot programs, and gradually expanding automation across departments.