Every loan file hides hundreds of pages. Every page hides data. And every data point decides whether a borrower moves into their dream home, or waits three more weeks for someone to type numbers into a system.

That’s why mortgage data extraction has become a priority for lenders. It turns a slow, people-heavy workflow into a cleaner, faster, more predictable process. And the industry is waking up fast. Nearly 48% of mortgage lenders list AI and automation as their top tech priority. That’s almost half the market saying, “Please, someone help me deal with these files.”

2025 has proven to be the year of smarter digital work. And mortgage data extraction sits right at the center of that shift.

What is Mortgage Data Extraction?

Mortgage data extraction is the process of pulling important information from documents inside a loan file a key step to revolutionize mortgage lending. Think of it as taking a blender to paperwork, except the output is clean, structured data instead of a mess.

Loan files contain a wide mix of documents: applications, tax forms, pay stubs, bank statements, credit reports, appraisal documents, and disclosures. Each one holds fields that underwriters need. Today, most of those fields are still typed in by humans.

This is why cost-per-loan numbers are brutal. Mortgage production costs reached $11,258 per loan in 2023, up from $10,624 in 2022, and double what lenders spent a decade ago. The main reason? Manual data entry and manual document checks which make up almost two-thirds of total origination costs.

Mortgage data extraction solves this problem by converting messy, multi-format pages into clean data that systems understand.

Examples of mortgage data extraction workflows

Here are a few common flows lenders deal with every day:

- Pulling borrower name, SSN, address, and employer from a 1003

- Extracting gross and net income from pay stubs

- Gathering deposits, withdrawals, and ending balances from bank statements

- Reading tax transcripts to calculate qualifying income

- Capturing rates, fees, and cash-to-close details from LEs and CDs

- Gathering appraisal values, comps, and property details

- Extracting credit scores and liabilities from credit reports

If a document has a field, someone probably types it somewhere. And if someone types it, errors follow. This is where automation makes a huge difference.

Types of mortgage documents commonly extracted

Mortgage teams typically extract data from:

- 1003 / URLA

- Loan Estimates

- Closing Disclosures

- Pay stubs

- W-2s and 1099s

- Bank statements

- Tax returns (1040, Schedule C, Schedule E, etc.)

- Verification forms (VOE, VOD, VOI)

- Credit reports

- Appraisal reports

- Purchase contracts

- Conditions and supplemental docs

Loan files often exceed 500–2,000 pages, depending on complexity. No wonder teams get buried in work.

Challenges of Mortgage Data Extraction (Manual & Traditional Methods)

Before we talk solutions, it’s worth looking at the problems lenders face today. These issues drain time, money, and patience across operations teams.

Key challenges in manual extraction

Manual extraction sounds simple: look at the document, type the field, keep moving. But anyone who works in mortgage knows the pain behind that idea.

Here’s what slows teams down:

1. Huge loan files: A single loan can include more than 300–700 pages. Some reach 1,500–2,000.

2. High error rates: Industry studies show 10–15% error/defect rates in early-stage manual mortgage processes. These are not small mistakes; they often cause repurchase risk, delays, and extra QC cycles.

3. Repetition: Underwriters and processors re-check the same values across multiple documents. Income, assets, identities, addresses, everything gets reviewed again and again.

4. Heavy labor costs: Human work is expensive. With cost-per-loan already above $11K, relying on large operations teams creates a ceiling on efficiency.

5. Time pressure: Borrowers expect quick approvals. Investors expect clean files. Loan officers expect smooth closings. Teams often feel squeezed, especially during busy cycles.

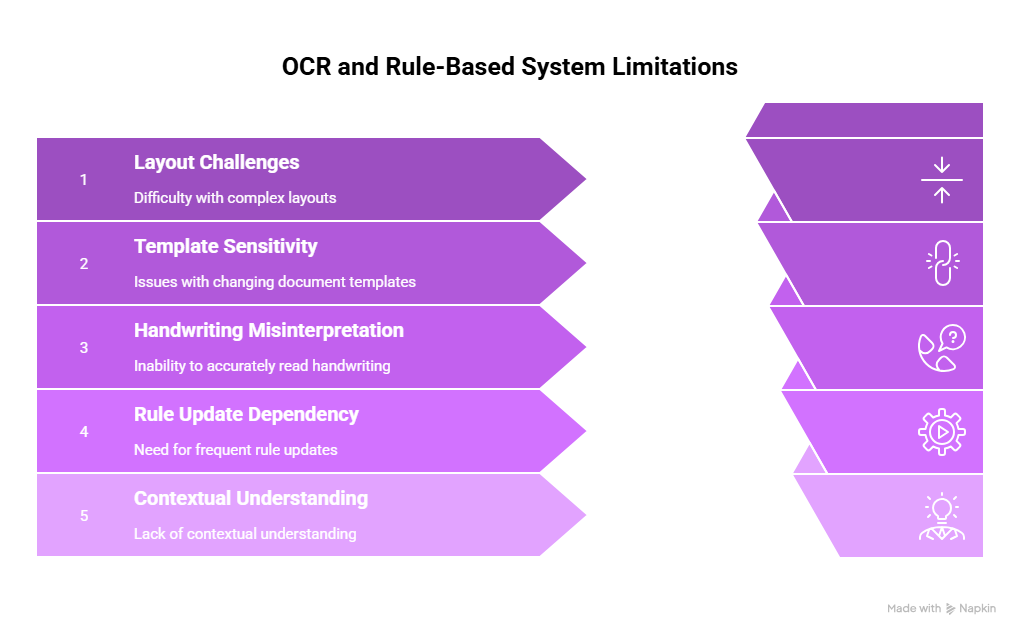

Limitations of OCR and rule-based systems

Many lenders tried OCR years ago. It worked fine for simple, predictable documents. Mortgage documents are not simple or predictable.

OCR falls short because:

- It struggles with tables, multi-column layouts, and dense forms.

- It breaks when document templates change.

- It misreads handwritten notes, signatures, and stamps.

- It needs constant rule updates.

- It doesn’t understand context as an underwriter does.

Rule-based tools have the same limitations. The moment formatting changes, everything breaks.

Mortgage documents shift often, and OCR can’t keep up. This pushes lenders toward more flexible solutions built on machine learning and large language models.

Why Lenders Still Use Manual or Semi-Manual Data Extraction?

If automation is so helpful, why does manual extraction still dominate the industry? A few reasons:

1. Legacy systems: Many LOS platforms weren’t built for modern automation. Integrating new tools can feel like rewiring an old house.

2. Risk concerns: Mortgage is a regulated industry. Teams want clean data and full audit trails. Anything new must prove it can handle sensitive documents safely.

3. Past disappointments: OCR and early automation tools overpromised and under-delivered. Some lenders still remember those painful rollouts.

4. Edge cases: Self-employed borrowers, gig workers, multi-borrower files, and investment properties create unusual document patterns. Teams fear that automation may miss these details.

5. Comfort with manual review: Humans trust their own eyes. Even if the process is slow, many teams stick with what feels “safe.”

But the industry is shifting. As costs rise and staffing becomes more difficult, mortgage leaders are turning to Intelligent Document Processing (IDP) and AI automation.

How to Automate Mortgage Data Extraction

Automated mortgage data extraction starts with one goal: reduce manual effort without hurting quality. The best systems read documents the way a skilled mortgage professional would, but at machine speed.

Step-by-step workflow of IDP-driven mortgage data extraction

Here’s what a modern workflow looks like:

1. Document intake: Loan files arrive in PDFs, images, or zip folders. Automation tools scan all pages instantly and prepare them for processing.

2. Classification: Each page is sorted into a category: LE, CD, pay stub, W-2, bank statement, and so on.

This prevents mix-ups and helps downstream extraction.

3. Field extraction: IDP models pull the right values from the right locations. Example: “Gross YTD Income” on a pay stub or “Cash to Close” on a CD.

4. Verification: Extracted data is checked across multiple documents to detect mismatches.

If an employer name differs between a 1003 and a pay stub, the system flags it.

5. Exception handling: Edge cases and unclear fields route to a human for review. Humans only see what needs attention, not the full file.

6. Output: Clean, structured data feeds into LOS, QC, servicing, and downstream systems.

The cycle is fast, consistent, and scalable.

How agentic AI enhances extraction in loan files

Agentic AI takes automation further by acting like a helpful coworker that never gets tired.

It can:

- Re-run extraction when new pages appear

- Reviews of the extracted data & initial verification against compliance rules

- Flag missing documents

- Ask for supporting info

- Check values across documents

- Suggest corrections

- Fix common formatting issues

- Compare versions of disclosures

- Prepare data packages for underwriting

It’s far more flexible than fixed rules. It adapts to the document instead of forcing the document to fit its design.

This gives teams speed without sacrificing control.

Advantages of Automated Mortgage Data Extraction

Automated mortgage data extraction cuts out the slow, repetitive work that weighs teams down. It turns long loan files into clean data without the constant typing, double-checking, and backtracking that drain time and energy. Lenders get faster turn times, fewer errors, lower costs, and smoother workflows.

Now let’s break the benefits down.

Faster loan processing & shorter cycle times

Every minute saved on data entry helps teams move loans faster. Automation cuts down the time spent on:

- Document classification

- Field typing

- Data validation

- Multi-document comparisons

- Rework for mismatched values

When teams finish faster, loans close faster. Borrowers feel relief. LOs feel supported. Everyone wins.

Fewer defects and higher accuracy

Automation reduces simple human errors:

- Wrong digits in income

- Mis-typed addresses

- Missing fields

- Values pulled from the wrong page

With lower defects, lenders face fewer investor findings and fewer repurchase risks. Operations leaders sleep a little easier.

Lower cost-per-loan and reduced repurchase risk

With rising production costs, efficiency is no longer optional. Automation lowers costs by:

- Cutting repetitive work

- Reducing QC cycles

- Reducing rework

- Preventing errors that lead to investor pushback

Given today’s numbers, even a small reduction in manual effort has a huge financial impact.

Better experience for underwriters, processors, and QC teams

Underwriters want clean files, not digital scavenger hunts. Automated extraction:

- Delivers data in clean formats

- Reduces noise

- Shortens the “hunt for documents” stage

- Helps teams focus on judgment work

It turns stressful workflows into smoother ones.

Top Technologies Used for Mortgage Data Extraction

Mortgage data extraction keeps improving because the tech behind it keeps getting smarter. Most lenders already know that old OCR can’t handle modern loan files. Today’s tools use a mix of machine learning, language models, and pattern recognition to understand documents the way humans do, only faster.

Let’s break down the main technologies that power this shift.

Intelligent Document Processing (IDP)

IDP is the core of modern mortgage automation. It reads, extracts, and organizes information from documents with far more accuracy than rule-based tools.

Here’s why lenders rely on it:

- It learns from real mortgage documents instead of relying on templates.

- It can read complex layouts like pay stubs, tax forms, and bank statements.

- It adapts to document variations.

- It can process thousands of pages without tiring or getting distracted.

IDP models consume millions of data points during training. This helps them recognize fields like “Net Pay YTD” on a pay stub, even if the layout changes. That flexibility is exactly what mortgage teams need, since every borrower brings a new mix of documents.

As the global market shows, this technology is growing fast. Neutral market research estimates that intelligent document processing will grow from about $10.5B in 2025 to nearly $67B by 2032, with annual growth of around 30%. Investment follows demand, and demand is exploding.

AI/ML-based classification

Classification decides what each page is. It’s the first step in a good extraction process. Without strong classification, the rest of the workflow collapses.

Old methods used templates or manual tagging. Today, AI handles the job using pattern recognition.

AI classification helps lenders:

- Separate LEs from CDs

- Identify bank statements

- Detect tax forms

- Distinguish VOEs from VOIs

- Tell income documents apart

- Spot appraisal pages and photos

Classification also reduces QC headaches. When pages are placed in the right buckets, downstream extraction is easier, cleaner, and more consistent.

Natural Language Processing (NLP)

Mortgage documents contain a lot of text. Some are structured (like LEs). Others look like someone squeezed a novel into a form (like tax returns). NLP helps systems understand language, context, and meaning.

NLP handles:

- Borrower names

- Employer details

- Address changes

- Fee descriptions

- Closing instructions

- Notes and conditions

It’s especially helpful when documents use different wording to say the same thing. Humans understand that “Employer Name” and “Company You Work For” mean the same field. Now systems do too.

Computer Vision & Advanced Parsing Models

Computer Vision helps systems read what the eye sees. Mortgage documents contain:

- Stamps

- Signatures

- Tables

- Columns

- Handwritten values

- Scanned pages

- Photos of IDs

Computer Vision makes sense of these elements. It’s the only way to read bank statements that look like they were designed by three different people who never spoke to each other.

Parsing models go further. They don’t just read—they interpret. They detect relationships between values, such as:

- Income amounts across multiple pay periods

- Loan amounts across early and final disclosures

- Fee changes across versions

- Repeated entries in bank statements

Together, these technologies allow extraction tools to do what the industry always wanted: read documents like experienced mortgage staff.

How Infrrd Automates Mortgage Data Extraction

Infrrd supports mortgage teams through a simple idea you shouldn't have to start your day sifting through a 2,000-page loan file. The AI-powered mortgage document handling and processing guide shows exactly how automation makes that a reality.

Instead, automation handles the heavy work before you log in. Here’s how Infrrd makes that possible:

No-touch processing for 500–2,000-page loan files

No-touch processing means the system prepares the loan file automatically. Humans step in when needed, not for every page.

Here’s how that looks in practice:

- The system receives a loan file in any format.

- It organizes pages into correct document types.

- It extracts fields with high accuracy.

- It checks data across documents.

- It flags mismatches or missing items.

- Human-in-the-loop systems address any errors or mismatches

- It delivers a clean data package.

This helps reduce the long hours teams spend gathering information. Underwriters can focus on judgment instead of manual review.

Ally: Agentic workflows that auto-review, cross-check, and validate

Infrrd’s Agentic AI, Ally, acts like a digital teammate. It doesn’t just extract. It “thinks” through the tasks a human would handle.

For example, agentic workflows can:

- Re-check income if a new pay stub arrives

- Compare versions of disclosures

- Spot missing signatures

- Flag conditions before the file goes to underwriting

- Identify data gaps

- Run quality checks on every document

This approach replaces endless back-and-forth emails and manual checks. It’s like having a junior analyst who never forgets a step.

Human-in-the-loop for final mortgage audit accuracy

Automation doesn’t remove people from the process. It frees them from repetitive steps.

Human-in-the-loop review helps teams:

- Validate uncertain fields

- Handle complicated borrower scenarios

- Manage exception cases

- Oversee final quality checks

- Document each decision for compliance

Automation and human oversight work together. Systems handle the bulk. Humans guide the edge cases. This balance keeps audit quality strong while improving speed.

Why the Future of Mortgage Data Extraction Is Bigger Than the Tech Behind It

Even though mortgage data extraction relies on deep tech—IDP, computer vision, and machine learning, the real value shows up in the day-to-day lives of the teams who handle loan files.

A processor who once spent hours typing from bank statements now starts with clean data. An underwriter who used to compare disclosures by hand now gets clear summaries of differences. A QC analyst no longer hunts for missing pages at the end of the month. They see flags before the file reaches them.

This is where automation shines. It protects teams from burnout and helps lenders operate with more confidence.

The Human Side of Mortgage Data Extraction

Even the strongest automation doesn’t remove the human element from lending. It does the opposite; it gives people more time to do the parts of the job that truly matter.

- Loan officers get more time with borrowers.

- Processors spend less time clicking through PDFs.

- Underwriters spend more time evaluating risk.

- QC teams spend more time ensuring files are ready for investors.

Automation handles the repetitive parts. People handle the judgment.

This balance brings the best results. It also creates a healthier workplace. Anyone who has ever typed numbers from a bank statement knows how draining that can be. When teams no longer face that volume of manual work, morale rises, and error rates drop.

How Lenders Can Get Started With Mortgage Data Extraction

Starting is often simpler than it appears. Many lenders imagine automation as a massive platform shift. It doesn’t need to be.

Most successful teams follow a clear path:

1. Start with a single document type: Income documents or bank statements are good starting points. They are high-volume and high-effort.

2. Run a small pilot: A few dozen loans are enough to test extraction quality and workflows.

3. Measure value early: Focus on metrics like time saved, error reduction, and effort removed.

4. Expand step by step: Once the first workflow proves value, teams add more documents.

LEs. CDs. Tax documents. Appraisals. Conditions. You build momentum one workflow at a time.

5. Integrate deeper over time: Once extraction works well, lenders connect it to LOS systems, QC tools, or audit screens.

This design keeps risk low. It also builds internal confidence, which helps teams adopt automation with less friction.

Where Mortgage Data Extraction Delivers the Most Impact

Lenders usually see the biggest gains in four categories. These improvements appear fast, even in the first 60–90 days of using automation.

Benefits of Mortgage Data Extraction:

1. Speed

When data flows into systems without manual typing, turn times shrink. This benefits everyone: borrowers, loan officers, processors, and investors. Turn times can drop by days. Sometimes more. A simple cut of two or three days can increase pull-through and reduce fallout.

2. Accuracy

Manual processes struggle with consistency. Repetition leads to fatigue. Fatigue leads to errors. Automated extraction catches mismatches much earlier. It also checks values against each other, which helps prevent bad data from moving deeper into the file. Clean data means fewer investor findings and fewer repurchase threats.

3. Cost Reduction

This is where leaders pay close attention. Lenders fight the rising cost-per-loan every year. Cuts in manual work help reverse that trend. Even removing a few hours of manual data entry per file has a meaningful effect. Multiply that across thousands of loans. It becomes a major line item shift.

4. Better Workload Balance

Underwriters and processors don’t need more pressure. They need fewer repetitive tasks. They want space to think and make solid decisions. Automation gives them that space. Teams spend time where it matters. They also avoid the burnout that often comes with intense periods of volume.

Why Some Lenders Still Hesitate to Automate Mortgage Data Extraction, and How to Move Past It

Some lenders still pause before adopting automation, even though the benefits are clear. Past tech failures, older systems, edge-case borrowers, and fear of change can make teams cautious. These concerns are understandable, especially in a business where accuracy matters. But most of these obstacles fade once lenders test modern extraction tools in a small, controlled pilot and see how much manual effort they can remove without adding risk. The following are some of the concerns that lenders have when it comes to automation and their answers.

“Our past OCR project didn’t go well.”

Old tools created frustration. New tools work differently. They learn from real loan files instead of fixed templates.

“Our LOS is old.”

Modern extraction tools connect to most LOS systems through standard interfaces.

“We have too many edge cases.”

Every lender does. That’s why human review stays in the loop.

“We’re worried about compliance.”

Audit trails, data visibility, user tracking, and secure handling are standard features today.

A Practical Look at Life After Data Extraction Adoption

Here’s a quick snapshot of how work feels after teams adopt mortgage data extraction:

- Loan files arrive and organize themselves.

- Income values appear in structured fields.

- Bank statement anomalies are flagged early.

- LE and CD changes show up clearly.

- QC teams receive cleaner files.

- Underwriters start with 80% of the work already done.

Summary

Mortgage teams are under pressure from every angle. Volumes rise and fall. Staffing costs remain high. Compliance rules tighten. Borrower expectations climb. Meanwhile, loan files keep growing, both in size and variety. Some days it feels like every borrower arrives with a different version of a pay stub, a tax return, and a bank statement.

This is exactly why data extraction has become a strategic priority. Mortgage data extraction gives lenders the breathing room they need. It takes the hardest part of the job, the paperwork, and turns it into something faster, cleaner, and easier to manage.

FAQs about Mortgage Data Extraction

Below are the core questions lenders ask when thinking about data extraction. Each answer is written in a simple, direct style to support clarity.

Q1. What type of mortgage data can be extracted automatically?

Most fields in a loan file can be extracted through automation. These include borrower names, SSNs, income values, account balances, liabilities, property information, fees, rates, and closing figures. Systems also handle multi-page documents and recurring tables found in bank statements or tax forms.

Q2. How accurate is automated mortgage data extraction?

Accuracy depends on document quality and the models behind the extraction. Manual processes show 10–15% error rates based on neutral industry studies. Automated systems reduce many of these manual mistakes by checking values across documents and producing consistent results. Human review handles edge cases.

Q3. What documents are included in mortgage data extraction?

The most common include:

- 1003

- LEs

- CDs

- Pay stubs

- Bank statements

- W-2s / 1099s

- Tax returns

- VOE / VOI / VOD forms

- Appraisal reports

- Credit reports

- Purchase contracts

Automation can extract values from most of these formats.

Q4. How does mortgage data extraction improve underwriting speed?

It saves time by removing data entry and manual document hunting. Underwriters receive structured data instead of a long stack of PDFs. This shortens cycle times and reduces the rework associated with mismatched values across documents.

Q5. What is the difference between OCR and IDP?

OCR captures text. That’s it. It cannot understand meaning, context, or document structure.

IDP reads documents the same way humans do. It identifies fields, understands context, checks values, and interprets information. This makes it far more useful for mortgage files.

Q6. Can automation handle handwritten or low-quality mortgage documents?

Yes, but with limits. Computer Vision and machine learning can read many handwritten or noisy forms. If a field cannot be interpreted with confidence, it is routed to a human reviewer. This keeps quality high.

Q7. How long does it take to implement mortgage extraction automation?

A focused pilot can run in a matter of weeks. A broader rollout takes longer, depending on integrations, training, and the variety of documents used by the lender.

Q8. Is mortgage data extraction secure for regulated workflows?

Yes. Modern systems follow security standards and provide complete audit trails. Access control, encryption, and version tracking are part of standard deployments in lending environments.

Q9. Do lenders still need humans in the loop?

Yes. Humans review uncertain fields, confirm edge cases, and complete final checks. Automation does the heavy lifting, while humans guide decisions.

Q10. What are the real-world ROI benefits of mortgage data extraction?

A few key benefits lenders often see:

- Lower cost-per-loan

- Fewer manual defects

- Lower repurchase-related risk

- Faster turn times

- More capacity without adding staff

Combined, these help lenders stay competitive in a tight market.

Priyanka Joy is a product writer at Infrrd who approaches automation tech like a curious detective. With a love for research and storytelling, she turns technical depth into clarity. When not writing, she’s immersed in dance, theatre, or crafting her next narrative.