As loan files grow thicker and compliance demands rise, lenders are facing a critical question: Can we keep up with manual processing? The answer is a clear and blunt NO.

Each mortgage file contains hundreds of pages - 1003s, VOEs, pay stubs, disclosures, tax forms, all needing to be reviewed, verified, and entered with precision, which is exactly what a mortgage document processing guide helps streamline. That’s hours of repetitive work for every loan. And one small error? It can mean delays, buybacks, or compliance issues that ripple through your entire pipeline.

That’s where mortgage document automation comes in.

Powered by AI and intelligent document processing (IDP), automation tools can read, classify, extract, validate, and route data across massive document sets in minutes. No more manual sorting. No more double data entry. Just clean, accurate information delivered straight into your LOS.

In this beginner’s guide, you’ll explore what mortgage document automation actually is, why it’s becoming essential for lenders, how automation fits into real-world mortgage workflows, and what to look for in a solution.

If your team is still buried in PDFs and spreadsheets, this is your path out.

Let’s get started.

What is AI Mortgage Document Automation?

Mortgage document automation is the process of using software powered by AI and machine learning to handle mortgage paperwork from start to finish. It doesn't just scan documents. It understands them.

Think of it like a super-fast, always-on assistant that knows how to:

- Recognize what type of document it's looking at

- Extract the right fields (names, income, dates, account numbers)

- Cross-check for missing or inconsistent data

- Sort files into logical stacks for your LOS

- Deliver clean, verified data with little human help

And it does all of this in minutes, not hours.

Why Mortgage Document Automation Matters in 2025?

The demand for automation didn’t appear overnight. It built up over years of slow closings, staffing shortages, rising compliance pressure, and growing borrower expectations.

In 2024, the global Intelligent Document Processing (IDP) market was valued at $7.89 billion. That’s not just about mortgage; it covers every industry that handles large volumes of unstructured data. But mortgage is one of the key sectors driving this growth.

The same Fortune Business Insights report projects the market will grow to $66.68 billion by 2032, at a CAGR of 30.1%. North America leads this charge, holding nearly 48.04% of the market share in 2024.

From Paper Stacks to AI Speed: How Automation Works

Let’s take a basic example. A borrower submits a single PDF with 200 pages. That file contains pay stubs, a credit report, a signed loan estimate, a 1003, and some scattered bank statements.

Without automation, someone would:

- Scroll through every page

- Label each document

- Identify and extract values manually

- Enter those details into the LOS or a tracking sheet

- Double-check for missing fields

- Flag discrepancies

- Repeat for the next loan file

Now, imagine all that happening in under 10 minutes, automatically.

Mortgage document automation systems:

- Classify each page: “This is a 1003. This is a VOE. This is a CD.”

- Split the file: Break it into organized, stackable chunks

- Extract key fields: Like borrower name, SSN, loan amount, income, etc.

- Validate entries: Is the CD signed? Is the VOE expired? Does the income match the pay stub?

- Flag missing data: So teams can fix it before it becomes a problem

That’s the power of automation, not just faster processing, but cleaner, more complete files.

Supporting Non-Traditional Borrowers with Automation

Mortgage document automation isn’t just for W-2 employees and standard loans.

It’s built to handle complexity, making it easier to process applications from non-traditional borrowers with speed and accuracy.

Here’s how intelligent automation helps:

- Self-Employed Borrowers

Extracts income from tax returns like 1040s and Schedule C, even when formats vary across years or providers. - Real Estate Investors

Pulls rental income, mortgage liabilities, and property details from supporting documents automatically. - Gig Economy Workers & Contractors

Handles 1099 forms, bank statements, and payment histories across multiple income sources—no manual entry needed. - Foreign Income & Assets

Reads non-U.S. documents, supports currency conversion, and recognizes international pay stubs and account statements. - Multiple Borrower Files

Identifies each borrower in shared loan files and correctly separates income, debts, and documentation for each one. - Alt-Credit Documentation

Processes non-traditional credit data like rent receipts, utility bills, and cash flow summaries, often used in alternative underwriting.

By removing the manual work, automation makes it easier to serve more borrowers, without sacrificing accuracy or compliance.

Core Benefits of Automating Mortgage Documents

Let’s be clear. This isn’t about replacing people. It’s about letting smart people do smart work, not click buttons all day.

Here’s what teams get:

- Less grunt work: No more digging through PDFs for that one missing signature

- Faster cycle times: Loans move from intake to underwriting quicker

- Fewer errors: Automation spots inconsistencies that humans might miss

- Lower costs: Processing more files without needing more people

- Happier staff: Auditors and processors aren’t burned out by page flipping

- Stronger compliance: Systems can auto-flag expired disclosures or mismatched forms

Mortgage document automation doesn’t just help one department. It supports operations, risk, compliance, and audit teams all at once.

Manual vs Automated Mortgage Workflows: A Side-by-Side Comparison

Let’s compare and see why mortgage document automation is and should be preferred.

That time saved adds up. Over weeks. Over months. Across dozens of teams.

How Mortgage Document Automation Works: Step-by-Step

Many people think automation means pushing a button and getting perfect results. That’s close, but not quite. Behind the scenes, mortgage document automation follows a structured process. Each step removes manual effort while keeping data quality high.

Let’s break it down.

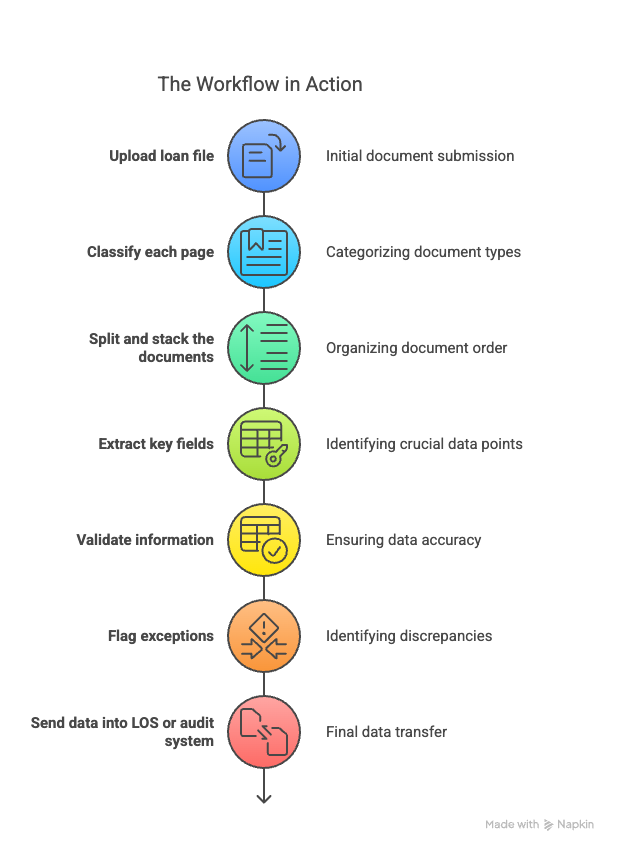

Step 1: Document Classification

It all starts with identification. When a loan file comes in, the system has to recognize what each page is.

This is called classification.

The system uses AI to “read” the content on each page. It doesn’t care how the document looks. It looks for text patterns, structure, and data. From that, it can identify:

- “This is a 1003 loan application”

- “This is a W-2”

- “This is a bank statement”

- “This is a Closing Disclosure (CD)”

Whether the documents are rotated, scanned poorly, or missing headers, it still figures it out.

Why this matters: classification is the foundation. If the system gets this part wrong, everything after breaks. Good automation tools get this step right, fast.

Step 2: Splitting and Stacking

Once the system knows what each page is, it needs to organize them.

Most loan files come in as one giant PDF. But processors don’t want to scroll through 400 pages. They need files split and grouped properly.

Splitting means breaking a large PDF into individual documents.

Stacking means putting those documents into logical bundles.

For example:

- Stack 1: Loan Application (1003 + addendum)

- Stack 2: Income Documents (W-2s, pay stubs, VOEs)

- Stack 3: Disclosures (CDs, LE, loan estimate)

The system also bookmarks the documents so your team can jump to what they need instantly.

This is a huge time-saver.

Step 3: Data Extraction

Once files are organized, it’s time to extract the data.

Data extraction pulls specific fields from the documents—just like a processor would. This includes:

- Borrower name, address, and contact details

- Loan amount and terms

- Gross income, net income, deductions

- Bank account numbers and balances

- Employment dates and employer info

- Closing costs and APR

The system doesn’t rely on templates. Instead, it reads the layout dynamically. That’s important because forms change over time. Rigid template systems break. AI-powered platforms adapt.

Good tools can pull data from:

- Typed text

- Scanned images

- Rotated pages

- Low-quality faxes

It’s accurate, fast, and doesn’t need manual setup.

Step 4: Data Validation

Once data is extracted, it needs to be verified.

This is where validation comes in.

The system checks the extracted data for logic and consistency. For example:

- Is the employer name the same across the VOE and pay stubs?

- Does the income on the 1003 match the income on the W-2?

- Is the CD expired?

- Is the document signed where needed?

If there’s a mismatch, it flags it for review.

Instead of manually double-checking everything, your team only reviews exceptions.

Step 5: Exception Flagging

Not all files are perfect. That’s why smart systems include exception flagging.

If a VOE is missing, it’s flagged.

If a document is unreadable, it’s flagged.

If two forms show different incomes, the system calls it out.

Flagged issues are added to a checklist so your team can review them fast. No more guessing what went wrong. The system tells you exactly what needs attention.

Step 6: Data Delivery

Finally, the system sends the clean data where it needs to go.

That might be:

- Your LOS (Loan Origination System)

- A document repository

- A compliance engine

- A risk tool

- A downstream audit process

This step is where automation shines. Instead of copying and pasting data or exporting spreadsheets, everything is already in the right place.

The result: faster processing, fewer errors, and a better experience for your team and your borrowers.

Compliance & Fraud Detection in Mortgage Document Automation

Automating mortgage documents isn’t just about speed. It also improves compliance, reduces fraud risk, and boosts data security. Here’s how intelligent mortgage automation handles these tasks:

Fraud and Tampering Detection

AI checks every document for signs of fraud.

It looks for:

- Signature mismatches

- Altered or fake documents

- Conflicting values across forms

- Signs of editing in scanned images

Mortgage automation software uses pattern recognition to detect unusual behavior early, before it becomes a problem.

Built-In Audit Trails for Mortgage Documents

Every action in the automation process is logged.

That includes:

- Document classification

- Data extraction

- Exceptions flagged

- Manual reviews

Audit logs are stored automatically and are ready for any compliance checks. Lenders can trace every change, reducing audit risk.

Human Review and Bias Controls

Even with AI, human oversight matters.

Smart systems allow human-in-the-loop review. That means:

- You control sensitive decisions

- Your team reviews flagged issues

- AI bias is monitored and corrected

This adds a layer of safety and fairness in mortgage document processing.

Mortgage Document Security and SOC 2 Compliance

Security is a top priority for document automation in mortgage.

The best systems follow strict protocols:

- Role-based access (RBAC)

- Data encryption at rest and in transit

- Secure storage with full access logs

- SOC 2 Type II certified infrastructure

That means your data stays protected, and you stay compliant.

Supported Mortgage Document Types in 2025

Modern mortgage document automation platforms can handle over 600 document types. Some of the most common include:

- 1003 loan application

- VOE (Verification of Employment)

- VOD (Verification of Deposit)

- W-2s, 1099s, pay stubs

- Bank statements

- Tax returns (1040, Schedule C, etc.)

- Closing Disclosures

- Loan Estimates

- Appraisals

- Credit reports

Each of these has its own structure and quirks. A good automation tool knows what fields to look for in each and where to find them, even when the layout varies. See what happens inside the IDP workflow.

How Modern Document Automation Understands Context Beyond OCR

Some teams think they already use automation, but they’re still working with basic OCR (Optical Character Recognition) tools. These systems scan text, but they don’t understand context.

Modern automation goes beyond OCR. It doesn’t just extract data. It knows what that data means and what to do with it.

Instead of just pulling “$5,200” from a form, it knows: “This is gross monthly income from Line 1 of a VOE.”

That’s the level of intelligence teams need today.

The Workflow in Action

To summarize, here’s the complete automation path:

Each step replaces a manual task that used to take minutes or hours. Now, it happens in seconds.

Market Growth & Business Impact of Mortgage Document Automation

What started as a back-office upgrade is now a boardroom priority.

The rise of mortgage document automation isn’t about hype. It’s about survival.

Lenders are under pressure to do more with less. Cost-per-loan is rising. Loan cycles are longer. Compliance reviews take up more time. And borrower expectations? They’re higher than ever. In this environment, speed and accuracy are no longer perks. They’re necessities.

How Big is the Mortgage Document Automation Market?

Let’s look at the numbers.

According to Fortune Business Insights, the Intelligent Document Processing (IDP) market hit $7.89 billion in 2024. In 2025, it’s projected to grow to $10.57 billion.

By 2032, the number jumps to $66.68 billion.

That’s a compound annual growth rate of 30.1% in any sector. In document-heavy industries like mortgage lending, it’s a signal. A signal that the days of manual document work are numbered.

North America is leading the charge. It owned 48.04% of the global market share in 2024. U.S.-based lenders are actively investing in automation platforms to stay competitive and compliant.

What’s Driving the Adoption of Mortgage Document Automation?

Several factors are pushing lenders toward automation.

1. Rising Loan Volumes

Even with market swings, many lenders are dealing with high volumes of loan files. Each loan contains dozens of documents, and each document contains dozens of data points.

Manual teams can’t scale that quickly. Automation can.

2. Increased Audit Pressure

Regulators and investors require clearer audit trails. Every signature, every disclosure, every timestamp needs to be traceable. Document automation provides this automatically.

3. High Error Rates

Manual review is prone to error. Studies show defect rates in manual mortgage processes can reach 10% to 15%. That’s huge, especially when automation can reduce those errors to fractions of a percent.

4. Staffing Challenges

Good processors and auditors are hard to find. And when you do find them, they’re overworked. Automation doesn’t replace them it reduces the noise so they can focus on judgment work.

5. Borrower Expectations

Today’s borrowers expect fast approvals. They’re used to digital banking. They won’t wait days for someone to key in their pay stub data manually.

What Mortgage Document Automation Actually Delivers

Let’s get practical. What does automation look like in real-world mortgage operations?

Here’s a breakdown.

✅ Faster Processing

Loan files are sorted, tagged, and data-extracted in under 10 minutes. What used to take hours now happens before your team logs in.

✅ Cleaner Data

Automation tools pull the correct fields with 95%+ accuracy. That includes tricky forms like 1040s, VOEs, and scanned W-2s.

✅ Fewer Defects

When the system validates data upfront, you catch problems earlier. That means fewer file reworks. Fewer suspended loans. Fewer last-minute scrambles.

✅ Lower Costs

By reducing manual tasks, lenders lower their cost-per-loan. They don’t need to hire more processors just to handle busy seasons.

✅ Better Compliance

Automation creates an audit trail as it works. Every action is recorded. That means easier responses to investor reviews, internal audits, or regulator questions.

How Lenders Use Mortgage Document Automation Today

Here are four ways lenders are already using mortgage document automation:

1. Pre-Close Checks

Before underwriting begins, the system checks that all required documents are present and complete. It flags anything missing so the team can act fast.

2. Loan Intake at Scale

When large batches of loans come in, automation splits and organizes the files instantly. The team can start reviewing loans instead of organizing them.

3. QC and Post-Close Audits

The system flags data mismatches and expired forms automatically. Auditors only need to review what’s actually flagged.

4. Re-Verification for Resubmissions

If a loan gets kicked back, automation can re-check documents quickly. No need to start from scratch.

Impact by the Numbers

Based on real adoption trends:

The numbers vary by lender, but the pattern is clear. Automation improves every major metric that matters to lending teams.

Who Benefits from Mortgage Document Automation?

Everyone. Everyone in the mortgage industry will see and experience the luxurious upgrade that automation brings.

➤ Processors

They don’t waste time clicking through PDFs. They work on problem-solving, not data entry.

➤ Auditors

They get cleaner files and a clear list of what needs review.

➤ Managers

They see more consistent output and better SLA performance.

➤ Executives

They reduce cost per loan, improve time to close, and stay ahead of competitors.

What About Borrowers?

Borrowers may not know what's happening behind the scenes but they feel the difference.

Loans close faster. Fewer document requests. Less confusion. A smoother journey.

That experience translates into higher satisfaction and stronger relationships.

How to Implement Mortgage Document Automation?

You Don’t Need to Change Everything to Change Everything

One of the biggest fears about automation is disruption. Lenders worry they’ll have to pause operations, retrain teams, or switch systems.

That’s not the case anymore.

Modern mortgage document automation tools work alongside your existing stack. They don’t replace your LOS. They complement it. That means no risky rip-and-replace rollout.

Instead, you start seeing results quickly with minimal effort.

Integration with Loan Origination Systems (LOS)

You already use a Loan Origination System to manage your mortgage pipeline. It might be Encompass, Byte, Blend, or something custom. Automation connects to it directly.

Here’s how it works:

- Document intake happens as usual

- Files are routed to the automation platform

- The platform classifies, extracts, and validates the data

- Clean results are pushed into your LOS or wherever you need them

No more toggling between tools. No more manual uploads. It’s seamless.

Whether your LOS is on the cloud or on-prem, automation tools can match your setup.

Cloud or On-Prem: You Choose

Not every lender wants to run on cloud infrastructure. Some need on-prem deployment to meet internal or regulatory needs.

Modern document automation platforms support both.

- Cloud: Fast setup, low maintenance, remote access

- On-Prem: Full control, internal compliance, secure internal data flow

Choose what fits your business. The benefits of automation don’t depend on the hosting model.

What Does Setup Actually Look Like?

You don’t need six months and an army of consultants.

Today’s automation tools are:

- Template-free: They don’t rely on rigid rules that break when a form changes

- Pre-trained: They already know how to handle mortgage documents

- Modular: You can start with one process (e.g., VOEs), then expand

That means setup is fast often in days, not months.

Here’s a typical onboarding timeline:

The biggest lift? Choosing which team starts first. Everything else moves quickly.

Choosing the Right Mortgage Automation Vendor: Key Questions

Not all platforms are equal. Some are built for banking. Some are generic. Others specialize in mortgage.

For those wondering how to pick the best IDP vendor, ask them these questions:

1. How many mortgage document types do you support?

Look for support for 1003s, VOEs, CDs, credit reports, tax forms, and bank statements at a minimum. The best platforms handle 600+ types.

2. Do you require templates or manual setup?

Avoid tools that need templates. They take time and break easily. Template-free systems adapt to form changes automatically.

3. Can we test with our own documents?

Always test the platform with your real loan files. Generic demos won’t reflect how it handles your formatting, noise, or layout quirks.

4. What’s your average field-level accuracy?

Top-tier platforms reach 95–99% accuracy on extracted fields. Ask for proof, not promises.

5. How do you handle exceptions?

Make sure the platform doesn’t just flag issues, but clearly shows what’s wrong and where to fix it.

6. Is the platform secure?

Look for SOC 2 Type II compliance and clear policies for data storage, retention, and access.

7. What’s the pricing model?

Some vendors charge per document. Others use per-page or volume tiers. Understand how scale affects cost before you commit.

Change Management: Making It Stick

Tech is only part of the equation. Teams need to feel the value.

The best rollouts start small. Choose one workflow like pre-close checks, and introduce automation there. Once teams see how much time they save, they’ll want it in other areas too.

Also helpful:

- Set clear goals (e.g., cut processing time by 40%)

- Share wins early (e.g., “we caught 12 missing VOEs this week”)

- Get feedback from processors and auditors

- Build internal champions across teams

When people trust the tool, adoption becomes natural.

The True Cost of Delaying Mortgage Automation

Every month, without automation, teams lose time to repetitive work. That’s not just frustrating, it’s expensive.

Let’s say your team processes 1,000 loans/month.

- Manual work adds 45 minutes per file

- That’s 750 hours per month of repetitive labor

- Even at $35/hour, that’s $26,250 burned on busywork

Now multiply that across your full operation. That’s money better spent on growth, borrower experience, or strategic hiring.

Use Automation to Handle Spikes in Volume

Market conditions change. Refinance booms. Policy shifts. Portfolio sales.

When volume spikes, staffing up isn’t always possible. Automation scales instantly. It runs 24/7. It doesn’t need breaks, PTO, or training.

Some lenders let AI take the first shift, and it works overnight, getting files ready by the time the team logs in. It’s like having an extra ops team that doesn’t sleep.

You Don’t Have to Do Everything at Once

Document automation doesn’t need to be all-or-nothing.

Start where it hurts the most:

- Are pre-close checks taking too long?

- Is your QC backlog growing?

- Are your processors buried in bank statements?

Automate one of those pain points first. See results. Then expand.

Real-World Use Cases of Mortgage Document Automation

Where Automation Fits into Your Daily Workflow

It’s one thing to talk about automation. It’s another to see where it actually helps.

Mortgage document automation isn’t just for one team or one task. It fits into multiple stages of the loan lifecycle like:

1. Pre-Close Document Review

Before a loan moves into underwriting, you need to confirm:

- All required documents are present

- None are expired or missing pages

- Income and employment data match across forms

This step can take hours. Processors scan each document, compare values, and log findings manually.

With automation, it’s the system:

- Classifies all incoming files

- Flags missing or invalid forms

- Highlights inconsistencies (e.g., VOE income doesn’t match W-2)

- Prepares a checklist of issues to resolve

Your team doesn’t have to dig. They log in and see exactly what needs fixing.

This alone can save hours per loan file.

2. Loan Intake and File Prep

A bulk upload of 500 loans used to mean:

- Dozens of hours just organizing PDFs

- Manually stacking pages by document type

- Bookmarking files for review

Now, automation does it all in minutes.

For example, the system can:

- Split a 1,200-page PDF into 75 complete loan files

- Classify each page by document type

- Stack and label each group correctly

- Bookmark key pages for faster review

That means your team can get straight to work without any prep time.

3. Quality Control (QC) Reviews

Post-close audits are crucial. But they’re also time-consuming.

Auditors often have to read through entire files to confirm:

- Dates and signatures are valid

- Required documents are present

- Key values are consistent across forms

Automation simplifies this by prechecking:

- Missing documents

- Mismatched data fields

- Unreadable scans

- Signature gaps

- Expired disclosures

It highlights only what needs review.

Auditors can move faster. They review issues, not every single page.

This improves productivity without sacrificing accuracy.

4. Resubmissions and Conditions Clearing

If an investor or underwriter requests changes, your team may need to reprocess a loan.

That means:

- Verifying document changes

- Re-checking income, assets, or ID fields

- Resending validated files

Automation speeds this up.

Rather than starting over, the system re-runs the updated documents. It flags only the changes or issues that remain.

This is especially helpful during investor feedback or funding delays.

5. Document Archival and Indexing

Post-close, documents are often archived for compliance or future reference. But unorganized archives cause issues later.

Automation helps by:

- Indexing files with correct document labels

- Embedding bookmarks and metadata

- Creating searchable records

Instead of digging through folders, teams find what they need in seconds.

6. High-Touch Loan Scenarios

Some loans are more complex than others self-employed borrowers, multi-property owners, foreign income, etc.

These loans generate more paperwork and require more checks.

While humans still handle judgment calls, automation:

- Extracts data from Schedule C or foreign tax forms

- Flags inconsistencies in asset declarations

- Organizes supporting documents for faster review

This keeps high-effort loans from slowing down your team.

7. Internal and External Audits

When regulators or investors request reviews, time is tight. You need:

- A full paper trail

- Verified data

- Document timestamps

- Exception logs

Automation provides that.

Every action is recorded:

- When the document was processed

- What data was extracted

- Which rules were flagged

- How issues were resolved

This makes it easier to defend decisions and pass audits with confidence.

8. Overflow Processing During Peak Volume

During busy seasons, teams often hit a wall. Hiring is slow. Training takes time.

Automation handles overflow instantly.

Let’s say your team can normally process 300 loans per month. Suddenly, you receive 500.

Rather than scramble, automation handles:

- Splitting and stacking files

- First-pass validation

- Flagging red flags

Your team focuses only on exceptions or edge cases. That’s how you handle spikes without stress.

9. Income Verification Support

Verifying borrower income can involve multiple forms—W-2s, VOEs, pay stubs, tax returns.

Automation reads these documents and pulls key values like:

- Gross monthly income

- Bonus and overtime

- Employment start/end dates

- Employer contact details

It matches income across forms and flags mismatches. This helps underwriters make faster, more confident decisions.

10. Early Risk Detection

Mistakes are costly when caught late.

Mortgage document automation helps you catch:

- Missing CD signatures

- Expired VOEs

- Unverified assets

- Identity mismatches

Before a file hits underwriting or investor delivery, the system flags issues. This early detection prevents rework and delays.

Real Results from Lenders Like You

Common Myths About Mortgage Document Automation

Let’s Address the Big Fears

Mortgage document automation has been around for years, yet some lenders still hesitate. The reasons vary, but they often boil down to fear of change, of cost, of complexity.

In reality, most of those fears aren’t true. Let’s walk through them.

Myth #1: “We’ll Lose Control”

Reality: You actually gain visibility.

Automation doesn’t remove people from the loop. It removes the boring tasks that don’t need a human in the first place. You still see every file. You still make the decisions.

The difference? Your team focuses only on exceptions, not everything. You know exactly what was extracted, what failed validation, and what got flagged.

That’s more control, not less.

Myth #2: “We Don’t Have Enough Volume to Justify It”

Reality: Even 50 loans a month can create thousands of document pages.

It’s not about loan count, it’s about document load. One loan might generate 100 pages. That’s 5,000 pages per month. Manually reviewing that takes dozens of hours.

Automation saves time at any scale. Even small teams benefit. And they free up staff for higher-value work.

Myth #3: “It’ll Be Too Hard to Set Up”

Reality: Modern platforms are fast to implement.

You don’t need a 6-month IT roadmap. You don’t need to change your LOS. Most tools run alongside your current setup. No templates. No coding.

You upload your documents. The system learns. You go live.

We’ve covered this in earlier sections, but it’s worth repeating: smart lenders roll out automation in under 30 days.

Myth #4: “Our Documents Are Too Messy”

Reality: That’s exactly what automation is built for.

Rotated pages? Scanned in grayscale? Text in strange fonts? Old fax formats?

Advanced systems handle all of it. These platforms are trained on thousands of document types from real lenders.

If your team can read it, the system likely can too and faster.

How to Roll Out Automation Without Pushback

Here’s a step-by-step approach that works:

- Pick one high-impact workflow

Look for a task that’s time-consuming, repetitive, and easy to measure (like pre-close document checks). - Upload your real documents

Not samples. Not templates. Real files from your daily operations. - Set a benchmark

Record current time per task, error rates, or file processing volume. - Run the automation tool side-by-side

Let a small group compare outputs. - Share the results internally

Like: “We cut processing time by 40% this week.” “We found 8 expired VOEs before submission.” - Expand from there

Once the value is clear, use it in audits, onboarding, or post-close reviews.

Signs Your Team Is Ready

If you hear any of these often, you’re ready for automation:

- “We’re falling behind on audits again.”

- “Too many resubmissions this month.”

- “We just hired another contractor for processing.”

- “It took us 3 hours to organize a single loan file.”

These pain points don’t solve themselves. But automation helps, fast.

Final Thoughts

Mortgage document automation isn’t new tech anymore. It’s the baseline.

Lenders who use it stay ahead. They process more. They fix defects earlier. They make teams happier. And they close loans faster.

The lenders still stuck in manual mode? They’re falling behind. Not because of poor teams, but because they’re running with yesterday’s tools.

Automation is ready. Teams are ready. The business case is clear.

Bhavika Bhatia is a Product Copywriter at Infrrd who blends curiosity with clarity to craft content that makes complex tech feel simple and human. With a background in philosophy and a knack for storytelling, she turns big ideas into meaningful narratives. Outside of work, you’ll find her chasing the perfect café corner, binge-watching a new series, or lost in a book that sparks more questions than answers