Mortgage lending is one of the most document-intensive processes in financial services. Borrowers, banks, employers, title companies, and insurers each contribute their own paperwork, and across thousands of loans, that volume accumulates rapidly, creating significant pressure on processing teams and timelines.

The average mortgage application file today contains more than 500 pages of documentation. Processing that volume manually creates significant delays.

Mortgage document classification addresses this challenge directly and is a foundational step in any mortgage document processing workflow. It organizes incoming files, identifies document types, and prepares them for underwriting, verification, and audit. Without a reliable classification system, lenders are left managing a disorganized digital archive with no structure or labeling.

This guide breaks down how mortgage document classification works, why it has become a competitive necessity, and what it takes to automate it well.

What is Mortgage Document Classification?

Mortgage document classification is the process of identifying the type of each document within a loan file. When incoming files arrive, the system reads them and assigns each one to a predefined category. Common document categories include bank statements, W-2 forms, pay stubs, tax returns, credit reports, and loan applications.

Classification occurs before data extraction begins. It functions similarly to sorting mail before opening envelopes, establishing order so that each item can be handled appropriately. In practical terms, mortgage document classification means automatically recognizing and labeling documents within a mortgage file so that downstream systems can process them correctly.

Once a document receives a category label, that label determines the next step in the workflow. The category tells the system what action to take, which data to extract, and which verification process to apply.

Types Of Mortgage Documents That Require Classification

Mortgage files contain many document types that span the entire loan lifecycle. These documents are collected and reviewed across multiple stages of the mortgage workflow, from initial application through final closing.

Common examples include:

- Uniform Residential Loan Application (1003)

- Pay stubs

- Bank statements

- Tax returns

- W-2 forms

- Credit reports

- Title reports

- Appraisal documents

- Insurance certificates

Each of these document types serves a distinct purpose within the mortgage process. Together, they provide lenders with the financial, legal, and property-related information needed to evaluate and approve a loan.

Examples Of Mortgage Document Classification

When a borrower uploads a single PDF containing multiple documents, a classification system does not treat it as one file. It splits the PDF at natural boundaries, analyzes each section, and assigns a category label to each segment. Those labels then drive every downstream action automatically.

The table below shows how a 21-page upload from a single borrower might be classified and routed through the loan workflow:

Without classification, a processor would open this file, manually identify each document, rename it, drag it into the correct folder, and repeat that process for every loan in the pipeline. With classification, that entire sequence happens automatically before a human ever touches the file.

Why Mortgage Document Classification Matters?

Mortgage processing depends on document accuracy at every stage. A single missing document can delay a loan closing, and a misclassified file can trigger compliance issues that affect the entire workflow. This is why mortgage document classification has become a foundational step in modern lending operations, ensuring that every file is organized and identifiable before it moves forward in the process.

Impact On Loan Processing Timelines

Underwriters cannot review documents they cannot locate. When a bank statement is filed under the wrong category, the underwriter must spend time searching for it rather than completing the review. Across thousands of loans, these individual delays accumulate into significant processing backlogs that slow down the entire lending operation.

Accuracy And Compliance Benefits

Mortgage lenders operate under strict regulatory requirements. Auditors routinely review loan files to confirm that documents are accurate, complete, and properly organized. Incorrect classification creates gaps in audit trails that can expose lenders to regulatory risk. Consistent and correct classification improves file quality and supports compliance across the loan portfolio.

Role In Underwriting And QC Workflows

Underwriters are responsible for reviewing income, asset, and credit documents before a loan can be approved. Quality control teams verify that each file meets institutional policy requirements. Accurate classification places every document in its correct category, allowing both underwriters and quality control teams to locate and review materials quickly and efficiently.

Classification Affects Audit Readiness

Auditors expect loan files to follow a structured and predictable order. Effective mortgage document classification improves file transparency and makes the audit process more straightforward by ensuring every document has a clearly assigned category before review begins. It allows reviewers to confirm that all required documents are present, that each document appears in the correct section of the file, and that document versions are consistent with borrower data.

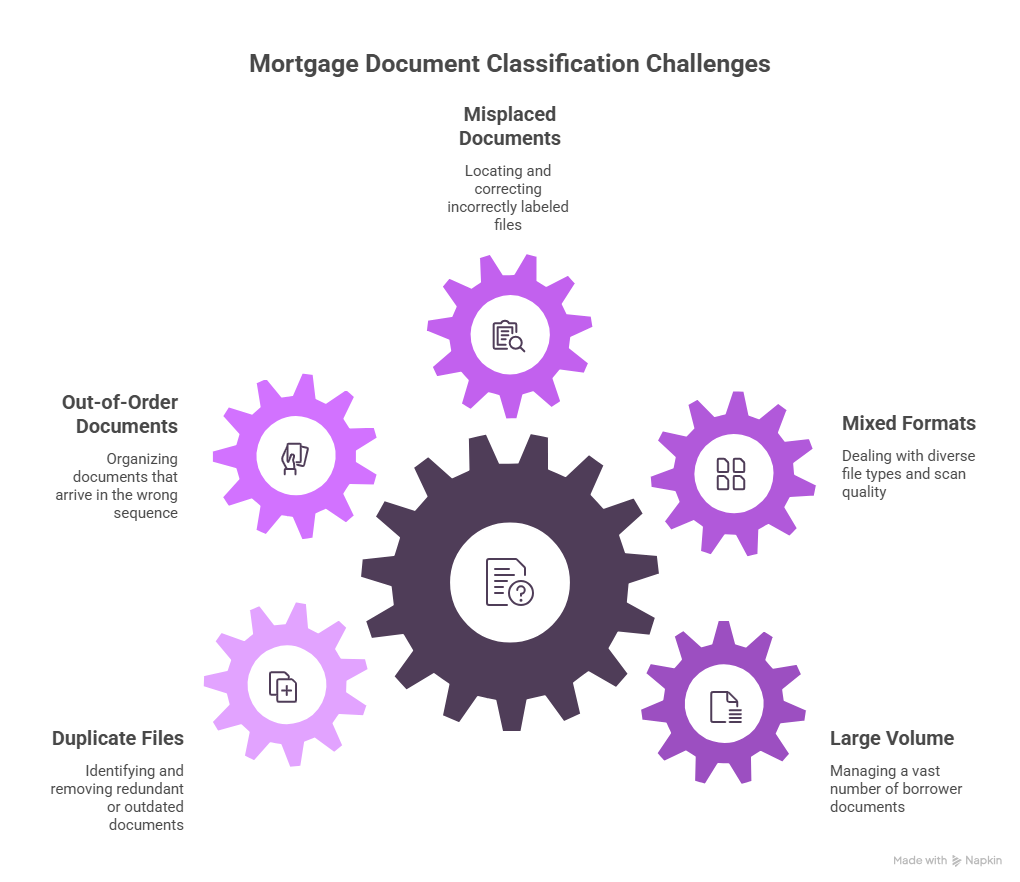

Challenges of Mortgage Document Classification

Mortgage documents rarely arrive in perfect condition. Borrowers upload photos taken on their phones, lenders receive scanned files of varying quality, and some documents contain handwritten information. These variations create significant challenges for any system attempting to classify documents accurately and consistently.

Large Volume Of Borrower Documents

Mortgage lenders process thousands of documents every day, and large lenders may review millions of files each year. The U.S. National Mortgage Database contains data on 11.9 million loans and 18.6 million borrowers, and each loan includes dozens of distinct document types.

Sorting that volume of incoming files manually is slow, error-prone, and difficult to scale, which is why mortgage document classification has become an operational necessity for lenders managing high loan volumes.

Mixed File Formats And Scanned Quality Issues

Mortgage files arrive in many different formats, including PDF, JPEG, TIFF, PNG, and scanned photocopies. Low-quality scans reduce the readability of document content, making it harder for systems to identify what each file contains.

Despite these quality limitations, classification systems must still determine the document type accurately in order to route files correctly through the workflow.

Misplaced Or Incorrectly Labeled Documents

Borrowers frequently upload files with generic names such as document.pdf, scan1.jpg, or statement.pdf. These filenames provide no meaningful context about the document's contents. As a result, manual processors must open each file individually to identify what it contains before any classification or routing can take place.

Documents Arriving Out Of Order

Mortgage files rarely arrive in a complete or sequential order. Borrowers submit documents across several days, and some upload missing pages or additional materials at a later stage. Classification systems must be capable of identifying and categorizing documents correctly, regardless of the order in which they are received.

Handling Duplicate Or Outdated Files

Borrowers sometimes upload the same document more than once, either accidentally or when replacing an earlier version. IDP must determine which version is current and which should be disregarded. Automated mortgage document classification can detect duplicate files quickly, reducing the time processors spend on manual version management and improving overall file accuracy.

Why Mortgage Companies Still Struggle with Document Classification?

Despite the availability of digital systems, many lenders continue to classify documents manually. Several operational and technical factors explain why this challenge persists across the industry.

Manual Sorting Of Borrower Documents

Loan processors often review documents one by one, manually renaming files and moving them into the appropriate folders. This approach is time-consuming and introduces the risk of human error, particularly when processors are handling large volumes of files under tight deadlines.

Traditional OCR Limitations

Optical Character Recognition technology is capable of reading the text within a document. However, OCR alone cannot reliably determine document type. A system may extract text from a file accurately but still assign it to the wrong category because it lacks the contextual understanding needed to distinguish between document types that share similar formatting or language.

Multiple Document Types In A Single File

Borrowers frequently upload combined PDF files that contain several distinct documents within a single submission. A single file might include a pay stub, a bank statement, and a tax return, all merged together. Classification systems must be able to split these combined files and assign the correct category to each section before processing can continue.

Lack Of Integration With Mortgage Systems

Modern mortgage operations rely on a range of interconnected platforms, including Loan Origination Systems (LOS), document management systems, and compliance tools. Without reliable mortgage document classification that connects directly with these systems, teams are still required to move documents manually between platforms, which reintroduces the delays and errors that automation is meant to eliminate.

How to Automate Mortgage Document Classification?

Modern automation platforms use AI to identify document types and organise loan files without manual intervention see how this classification step integrates into the full workflow in the complete mortgage automation guide for loan operations. These systems analyze patterns within each document, including text layout, formatting, and content structure, to determine what type of document they are processing.

AI-Based Document Recognition

AI models examine text layout, keywords, and formatting to distinguish between document types. Bank statements typically contain account numbers and transaction tables, pay stubs include income and employer fields, and W-2 forms carry employer identification information alongside earnings summaries. The model compares these patterns against known templates to assign each document to the correct category accurately and efficiently.

Machine Learning For Document Type Detection

Machine learning models are trained on large datasets of mortgage documents, allowing them to learn classification patterns across thousands of real-world examples. As the system processes more files over time, it refines its understanding of document variations and improves classification accuracy with each iteration.

Classification Models Trained On Mortgage Documents

Generic classification models often struggle with the specific formats found in mortgage files. Mortgage-specific models are designed to recognize document structures unique to the lending industry, including the many variations that appear across bank statements, pay stubs, and tax documents from different institutions and borrowers. This specialization makes mortgage document classification significantly more reliable than general-purpose alternatives.

Continuous Learning And Improvement

Modern classification systems continuously monitor their own accuracy. When a model mislabels a document and a reviewer makes a correction, that correction is fed back into the system as new training data. This feedback loop allows performance to improve steadily over time without requiring manual reprogramming.

Advantages of Automated Mortgage Document Classification

Automation delivers measurable improvements across the lending workflow. Manual document processing produces an error rate of approximately 10%, while automated systems reduce that figure to around 1-2%, representing a significant gain in accuracy and reliability.

Faster Loan Processing

Automated mortgage document classification identifies document types instantly as files enter the system. Loan processors receive organized, labeled files rather than unsorted submissions, and underwriters can begin their review sooner, reducing overall loan processing timelines.

Reduced Operational Costs

Manual document review requires large teams of processors performing repetitive, time-intensive tasks. Automation reduces the need for that level of staffing by handling routine classification work at scale. This allows staff to redirect their time toward higher-value activities that require human judgment.

Improved Document Accuracy

AI-powered classification systems apply consistent rules to every document they process. Unlike human reviewers, these systems do not experience fatigue or lapses in attention, which means accuracy remains stable even when processing large volumes of files over extended periods.

Better Borrower Experience

Borrowers expect fast decisions and transparent communication throughout the loan process. Automation reduces delays caused by slow document review, allowing lenders to move applications forward more quickly and deliver a smoother, more responsive experience to borrowers waiting for approval.

Easier Regulatory Compliance

Automated classification creates structured, consistent document records that are easy to navigate during audits. Compliance teams can locate specific documents quickly, and regulatory reporting becomes more straightforward when files are organized according to a reliable and repeatable classification system.

How Mortgage Document Classification Works?

Automated classification systems follow a structured workflow in which each stage prepares documents for the next step in the process. Understanding this workflow helps lenders evaluate how automation integrates with their existing operations.

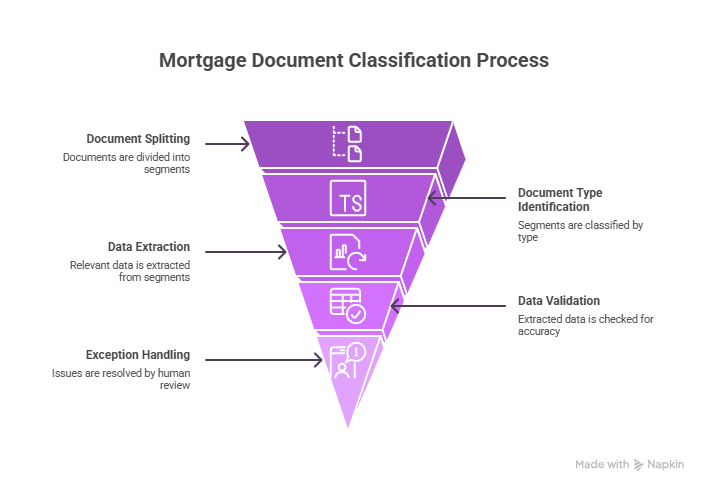

Document Intake And File Ingestion

Documents enter the classification system through multiple channels, including borrower portals, email attachments, and third-party integrations. As files arrive through these channels, the system ingests and stores them in preparation for processing.

Document Splitting And Segmentation

Borrowers frequently submit combined files that contain multiple documents within a single upload. Before classification can begin, the system identifies these multi-document files and separates them into individual sections so that each document can be categorized independently.

Document Type Identification

Once documents have been segmented, the classification model analyzes each file and assigns it to the appropriate category. Common categories include pay stubs, bank statements, tax returns, and other standard mortgage document types, each of which triggers a specific downstream processing workflow.

Data Extraction And Validation

After classification is complete, the system extracts relevant data fields from each document. These fields may include income amounts, account balances, and employer names, depending on the document type. Validation rules then compare extracted fields across documents to check for consistency and flag any discrepancies that require attention.

Exception Handling And Human Review

When the classification system detects uncertainty about a document's category, it routes that file to a human reviewer rather than assigning a potentially incorrect label. The reviewer confirms the correct classification, and that decision is fed back into the model as training data, reinforcing accuracy for similar documents in the future.

AI Mortgage Document Classification vs OCR

These two technologies are frequently confused, and the confusion leads to underinvestment in classification. OCR is a prerequisite for classification in many workflows, but it is not a substitute for it. They solve different problems.

A practical example: a scanned W-2 is uploaded to a mortgage portal. OCR reads the characters on the page and produces a text string. That text still needs to be interpreted; which field is the employer name, which is the annual wages figure, and what kind of document is this in the first place? Classification answers that last question and structures the extraction that follows.

Best Practices for Mortgage Document Classification

Mortgage lenders can improve classification accuracy and operational consistency by following a set of established best practices. These practices help ensure that automated systems perform reliably across high document volumes and varied file conditions.

Set Document Confidence Thresholds

Most automation platforms generate a confidence score for each document they classify. Lenders should establish minimum confidence thresholds so that any document falling below that threshold is automatically routed to a human reviewer rather than processed with an uncertain label. This safeguard reduces the risk of misclassification moving through the workflow undetected.

Handle Missing Pages And Incomplete Files

Classification systems should be configured to detect incomplete document submissions. For example, if a two-page bank statement arrives with only one page, the system should flag the file as incomplete rather than attempting to classify a partial document. Catching these gaps early prevents errors from compounding later in the underwriting process.

Use Standardized Document Taxonomies

Consistent document categories simplify processing and reduce ambiguity across teams. A well-structured taxonomy groups documents into logical categories such as income documents, asset documents, identity verification materials, and property documentation.

Standardizing these categories ensures that every team member and every system interprets document labels in the same way.

Integrate With Los And Document Management Systems

Effective mortgage document classification delivers its full value only when it connects directly with the platforms lenders already use. Integration with loan origination systems and document management tools allows classified documents to flow automatically into the appropriate loan workflows, eliminating the need for processors to transfer files manually between systems.

Monitor Model Performance Regularly

Lenders should track classification accuracy on an ongoing basis rather than assuming the system will maintain performance without oversight. Regular monitoring helps identify patterns in misclassification, reveals gaps in training data, and supports continuous improvement of the model over time.

How to Evaluate a Mortgage Document Classification Solution?

Selecting the right classification platform requires lenders to assess several critical factors. A thorough evaluation helps ensure that the solution performs reliably in real-world lending environments and integrates smoothly with existing operations.

Accuracy And Document Recognition Rate

The system should identify documents correctly across large datasets. If documents are labeled incorrectly, processors must fix them manually, which slows the workflow.

A reliable platform should recognize different versions of common mortgage documents such as pay stubs, bank statements, and tax forms. Lenders should also review the system’s confidence scoring. Documents with low confidence should automatically move to human review. Testing with real loan files helps reveal how the system performs with varied document layouts and scan quality.

Ability To Handle Multi-Document Files

Borrowers frequently submit combined PDF files containing multiple distinct documents within a single upload.

A strong mortgage document classification platform should automatically detect where each document begins and ends through a process called document segmentation. The system analyzes layout changes, headers, and keyword patterns to separate documents accurately before assigning category labels. Automated segmentation saves processing time and prevents the errors that occur when processors are required to divide large files manually.

Integration With LOS, POS, And QC Systems

Mortgage processing relies on several platforms, including loan origination systems (LOS), borrower portals (POS), document management tools, and quality control systems. A classification solution should connect directly with each of these platforms so that classified documents flow automatically into the correct loan files.

Without integration, teams must manually move documents between systems, which creates delays and increases error risk. Integrated systems allow classified documents to flow automatically into loan files. While integration is in place, underwriters and processors can access organized documents immediately, which speeds up the loan review process.

Scalability For High Loan Volumes

A classification platform must be capable of handling high document volumes without degrading in speed or accuracy. Scalability depends on processing speed, infrastructure capacity, and the system's ability to handle multiple documents in parallel. Lenders should test the platform with large document batches to confirm that performance remains stable and consistent during peak processing periods.

Security And Compliance Readiness

Any mortgage document classification platform must adhere to strict security standards to protect sensitive borrower information. Data encryption should protect documents during storage and transmission.

Access controls should restrict who can view or modify files, and audit logs should record document activity for compliance tracking. Lenders should also review whether the platform supports industry security frameworks such as SOC 2 or ISO 27001 before deployment.

How Infrrd Automates Mortgage Document Classification?

Infrrd uses AI-driven document processing designed for high-volume workflows. The IDP auto-classifies documents after retrieving them from the origin, and segregates them for easy accessibility for LOS/POS systems to generate comprehensive results.

AI-Driven Document Recognition Models

The platform analyzes document layout, text patterns, and formatting. These signals help identify document type quickly

Mortgage Document Classification & Data Extraction

Automation handles most document classification before human review begins and auto extracts the mortgage file data. Loan teams start work with organized files.

Cross-Document Validation And Verification

The system compares data across documents. Example: Income values in pay stubs match tax returns. It makes sure all the information is consistent across all documents. Human reviewers verify flagged documents through structured review screens. Corrections feed back into the learning model.

Integration With Mortgage Systems

The platform integrates with mortgage platforms and document repositories. Documents move directly into processing pipelines.

Conclusion

Mortgage document classification is no longer optional for lenders operating at scale. As loan volumes grow and regulatory requirements tighten, the ability to accurately identify, organize, and route documents determines how efficiently a lender can close loans and serve borrowers. Manual classification cannot keep pace with that demand. AI-powered systems that classify documents automatically, integrate with existing platforms, and improve through continuous learning give lenders a measurable operational advantage. Investing in the right classification solution today directly translates into faster processing, fewer errors, and stronger compliance outcomes tomorrow.

FAQs About Mortgage Document Classification

What Is Mortgage Document Classification?

It is the process of identifying and labeling documents in a mortgage file so systems can process them correctly.

Why Is Document Classification Important In Mortgage Lending?

It organizes documents and speeds up underwriting, verification, and audit processes.

What Types Of Mortgage Documents Need Classification?

Examples include pay stubs, tax returns, bank statements, loan applications, credit reports, and appraisal documents.

How Does AI Classify Mortgage Documents?

AI analyzes text patterns, document layout, and keywords to identify document types.

What Is The Difference Between OCR And Document Classification?

OCR reads text from documents. Classification identifies the type of document.

Can Document Classification Reduce Mortgage Processing Time?

Yes. Automation organizes files quickly and reduces manual sorting work.

How Accurate Are Automated Mortgage Classification Systems?

Modern systems can achieve accuracy above 95% depending on document quality and training data.

What Challenges Occur When Classifying Mortgage Documents?

Challenges include poor scan quality, mixed document files, and inconsistent borrower uploads.

How Does Document Classification Integrate With Los Systems?

Automation platforms send classified documents directly into loan origination workflows.

Is Human Review Still Needed After Automated Classification?

Yes. Reviewers handle exceptions and confirm documents with low confidence scores.