Every contractor, vendor, or service provider who has ever dealt with a certificate request knows the drill. The client needs proof of insurance before work begins, and they need it fast. The document they are requesting, almost without exception, is ACORD 25.

Despite being universal, the ACORD 25 remains a source of confusion for insurance professionals and operations teams alike which is why intelligent document processing for insurance certificate workflows removes the manual bottlenecks and human errors that slow down certificate issuance at scale. Questions about what it covers, how to complete it correctly, and why errors cause so many downstream delays come up constantly.

This guide walks through everything your team needs to know, from the form structure to the most effective ways to process it at scale.

What Is the ACORD 25?

The ACORD 25 is the standardized Certificate of Liability Insurance form developed and maintained by ACORD (Association for Cooperative Operations Research and Development). It serves as official proof that a named insured holds an active liability insurance policy with specified coverage types and limits.

The ACORD 25 provides certificate holders with verified proof of liability coverage — and for commercial risks that also include company vehicles, the ACORD 127 commercial auto section guide for insurance teams covers the vehicle and driver data that completes the full submission. This document allows a third party to confirm the existence of liability insurance without performing a comprehensive policy review. It provides exactly that a universally recognized format that carriers, brokers, and certificate holders can all read and verify at a glance.

The form does not create, modify, or extend coverage. It simply documents what already exists in the underlying policy. That distinction is critical and a frequent source of misunderstanding.

ACORD 25 and Its Relationship to Related Forms

The ACORD 25 does not exist in isolation. It sits within a broader ecosystem of ACORD certificates and evidence forms, and knowing how they relate prevents costly mix-ups.

The key rule: if a contract requires proof of liability coverage, the ACORD 25 is the correct form and for teams managing the full portfolio of certificates issued against those policies, the ACORD 26 Policy Certification Log automation guide explains how to keep that record accurate and up to date.

Why the ACORD 25 Matters to Insurance and Operations Teams?

The ACORD 25 is one of the most frequently issued documents in commercial insurance. Millions of certificates are generated every year across industries; construction, healthcare, logistics, real estate, and professional services all depend on them.

Here is why the form carries significant operational weight:

Contract Compliance

Most commercial contracts require certificate issuance before work begins. A delayed or inaccurate ACORD 25 can hold up projects, trigger contractual penalties, or disqualify a vendor from an engagement entirely.

Risk Transfer Verification

Certificate holders, the businesses requesting proof of insurance, use the ACORD 25 to confirm that their vendors and contractors carry adequate limits. It is a front-line tool for managing third-party risk exposure.

Regulatory And Lender Requirements

Lenders, municipalities, and government agencies frequently require ACORD 25 certificates as a condition of financing, permitting, or contract award. Errors here carry real financial consequences.

According to ACORD's own data, certificate of insurance processing is one of the top administrative burdens in commercial lines operations. The volume is relentless, and the margin for error is narrow.

Who Uses the ACORD 25?

Understanding who touches this document helps teams design better workflows around it.

Insurance agents and brokers generate ACORD 25 certificates on behalf of their policyholders whenever a certificate holder requests proof. This is typically a high-volume, time-sensitive task.

Policyholders (named insureds) submit the certificate as evidence of their coverage when entering into contracts or leases.

Certificate holders receive and review the form to verify that the insured's coverage types, limits, and effective dates meet the requirements specified in their contracts.

Underwriters and risk managers use the data captured on ACORD 25 certificates to assess third-party risk, especially when managing large vendor or subcontractor pools.

How to Complete the ACORD 25: A Section-by-Section Breakdown?

The ACORD 25 is organized into clearly defined sections. Completing each one accurately is non-negotiable; errors in any field can invalidate the certificate for the recipient's purposes.

Section 1: Producer Information

This section identifies the insurance agency or brokerage issuing the certificate. It includes the producer's name, address, phone number, and email. Accuracy here ensures the certificate holder can contact the right party if they need to verify coverage or request an endorsement.

Section 2: Insured Information

This block contains the name and address of the policyholder, the entity whose coverage is being documented. The legal name must match exactly what appears on the underlying policy. Mismatches, even minor ones, create verification problems and may lead to certificate rejection.

Section 3: Insurer Information

Up to five insurers can be listed on the form, each labelled from A through E. For every insurer, the full legal name and NAIC code must be provided. The NAIC code enables certificate holders to verify the insurer’s licensing status and financial strength independently.

Section 4: Coverages

This is the heart of the form. It documents the specific coverage types in force and their corresponding limits. The standard sections include:

- Commercial General Liability (CGL): Includes occurrence vs. claims-made designation, limits for bodily injury, property damage, personal and advertising injury, and general aggregate.

- Automobile Liability: Covers owned, hired, and non-owned autos. Includes combined single limit or split limits.

- Umbrella/Excess Liability: Documents umbrella or excess limits sitting above the primary policies.

- Workers' Compensation and Employers' Liability: Covers statutory WC limits and EL limits by accident, disease per employee, and disease policy limit.

- Other: A flexible section for professional liability, cyber liability, or any coverage not captured above.

Policy numbers, effective dates, and expiration dates are required for each coverage line. An expired policy date is one of the most common and most consequential certificate errors.

Section 5: Certificate Holder

This section identifies who is receiving the certificate. The legal name and address of the certificate holder must be exact. If an additional insured endorsement is required, it must be reflected here and in the coverages section. The certificate itself cannot grant additional insured status, but it can indicate that an endorsement exists.

Section 6: Description of Operations

This free-text field is used to note the specific project, contract, or relationship prompting the certificate request. It is also used to document additional insured status, primary and non-contributory wording, waiver of subrogation, and notice of cancellation provisions.

This section requires careful attention. Agents sometimes skip key endorsement language here, creating disputes when claims arise.

Section 7: Cancellation Notice

This section documents the number of days of advance written notice the certificate holder will receive if the policy is cancelled. Standard language specifies 30 days for cancellation and 10 days for non-payment.

Signatures and Authorized Representation

The certificate must be signed by an authorized representative of the issuing agency. An unsigned ACORD 25 is not a valid certificate.

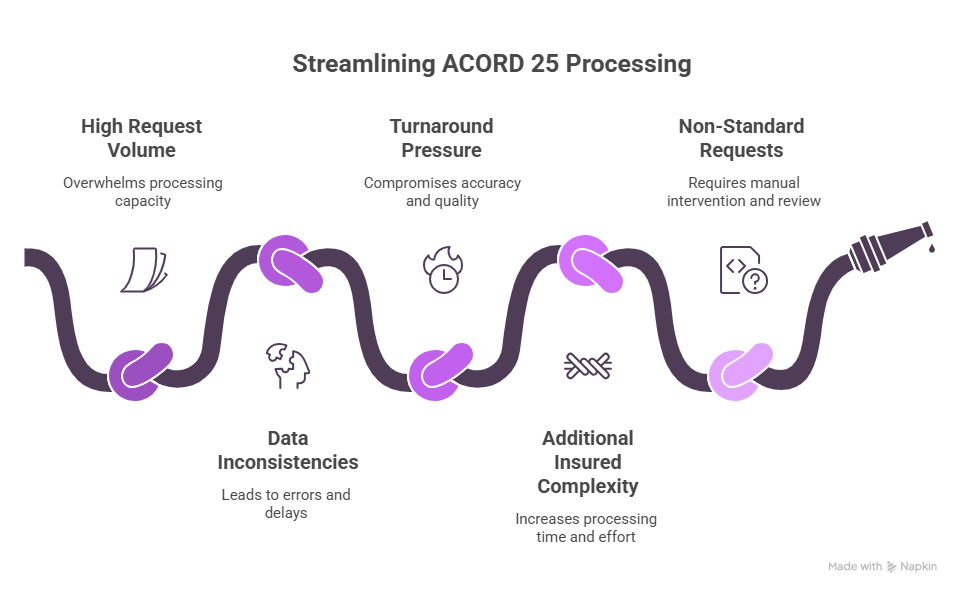

Common Challenges Teams Face With ACORD 25 Processing

The form is standardized. The problems are not.

High Request Volume

Large brokerages and carriers handle hundreds of certificate requests daily. Processing each one manually consumes significant agent time that would be better spent on coverage work.

Data Inconsistencies

Coverage information on the certificate must match the underlying policy precisely. When agents pull data manually from policy management systems, transposition errors and outdated information creep in.

Turnaround Pressure

Certificate holders often request same-day issuance. The combination of urgency and manual processes is a reliable formula for mistakes.

Additional Insured Complexity

When a certificate involves multiple additional insured endorsements with different terms, the Description of Operations section becomes crowded and error-prone.

Non-Standard Requests

Some certificate holders request custom language or non-standard limits. Agents must verify whether the underlying policy supports these requests before issuing a step that is easy to skip under pressure.

Studies from industry associations suggest that manual insurance data processing carries error rates of 15–20%. For a document as consequential as the ACORD 25, that is an unacceptable baseline.

Why Manual Processing of ACORD 25 Slows Teams Down?

An experienced agent can generate an ACORD 25 certificate in a few minutes under ideal conditions. In practice, conditions are rarely ideal.

The agent must locate the correct policy record. Verify that all coverage information is current. Cross-reference the certificate holder's requirements. Fill the form fields without errors. Get the certificate reviewed if additional insured language is involved. Then issue and deliver it.

Multiply that by two hundred requests a week, add in requests that come in outside business hours, and it is easy to see why certificate processing is a persistent operational bottleneck. It is like having a fast machine running on slow fuel. The potential is there, but the process keeps throttling it.

Automating ACORD 25 With IDP

Intelligent Document Processing (IDP) applies AI, machine learning, and OCR to extract, validate, and route data from insurance documents, including both inbound certificate requests and the source policy documents used to populate them.

Here is how automation changes the ACORD 25 workflow:

Step 1: Intake and Classification

When a certificate request arrives via email, portal, or fax, an IDP system classifies it automatically. The system identifies it as an ACORD 25 request, extracts the certificate holder's requirements, and routes it to the appropriate workflow without manual triage.

Step 2: Policy Data Extraction

The IDP engine pulls relevant coverage data directly from the underlying policy documents stored in the agency management system. Coverage types, limits, policy numbers, and dates are extracted with high accuracy with no manual lookup required.

Step 3: Field Population and Validation

Extracted data is mapped to the corresponding ACORD 25 fields. The system validates that all required fields are populated, that dates are current, and that coverage limits match the certificate holder's stated requirements. Mismatches trigger an automated alert for agent review.

Step 4: Additional Insured and Endorsement Checks

For certificates requiring additional insured status or special endorsement language, the system cross-references endorsement records and auto-populates the Description of Operations section with the correct language. This is one of the highest-error steps in manual processing; automation eliminates most of those risks.

Step 5: Issuance and Delivery

Once validated, the certificate is generated and delivered to the certificate holder through the preferred channel. The entire process from request intake to delivery can be completed in minutes rather than hours.

Advantages of Automating ACORD 25 Processing

Beyond speed and accuracy, automation frees agents to focus on coverage advice, renewals, and complex client work, tasks that require human judgment and cannot be automated away.

How Infrrd Automates ACORD 25 Processing?

Infrrd's Intelligent Document Processing platform is purpose-built for high-volume, accuracy-critical insurance document workflows. For ACORD 25 specifically, Infrrd addresses the full processing chain, not just data extraction.

Trained Document Models for ACORD Forms

Infrrd's models are pre-trained on ACORD form structures, including the ACORD 25. This means out-of-the-box recognition of every field, section, and layout variation across carriers and policy types without custom configuration for each client.

Policy Document Cross-Referencing

IDP extracts coverage data directly from underlying policy documents and maps it to ACORD 25 fields. The platform handles structured and semi-structured policy documents, including declarations pages, endorsements, and endorsement summaries.

Validation and Exception Management

When extracted data does not match certificate holder requirements or when a required field is missing, Infrrd’s IDP flags the exception for human review. Agents see exactly what needs attention, not a queue of undifferentiated documents.

Integration With Agency Management Systems

IDP connects with standard agency management platforms, pulling policy data and pushing completed certificates without requiring agents to toggle between systems. The result is a tighter, faster, and more accurate certificate operation.

Summary

The ACORD 25 is the foundational document for liability insurance verification in commercial lines. Its standardized structure makes it universally readable but that standardization does not make it simple to produce at volume, under time pressure, with zero errors.

Teams that continue to rely on manual ACORD 25 processing will find that the bottleneck only grows as certificate volumes increase. Automation, built on purpose-trained IDP models, gives operations teams the throughput and accuracy that manual processes simply cannot deliver.

FAQs About ACORD 25

Q. What is the ACORD 25 form used for?

The ACORD 25 is the Certificate of Liability Insurance. It documents that a named insured holds active liability coverage, specifying coverage types, policy limits, and effective dates. It is typically required by clients, lenders, and contract counterparties as a condition of doing business.

Q. Does the ACORD 25 provide coverage or modify a policy?

No. The ACORD 25 documents existing coverage — it does not create, extend, or modify any policy. Coverage is determined entirely by the underlying insurance contract.

Q. Who issues an ACORD 25 certificate?

The certificate is issued by the insured's insurance agent or broker on behalf of the carrier. The issuing agent must be an authorized representative of the insurance agency.

Q. What is the difference between ACORD 25 and ACORD 27?

The ACORD 25 is the Certificate of Liability Insurance, used to document general and professional liability coverage. The ACORD 27 is the Evidence of Property Insurance, used to document commercial property coverage.

Q. Can the ACORD 25 grant additional insured status?

No. Additional insured status can only be granted through an endorsement to the underlying policy. The ACORD 25 can confirm that such an endorsement exists, but the certificate itself does not confer additional insured rights.

Q. What does the Description of Operations section on the ACORD 25 contain?

This free-text field documents the specific project or contract prompting the certificate, and is used to note special conditions such as additional insured status, primary and non-contributory wording, waivers of subrogation, and cancellation notice provisions.

Q. How long is an ACORD 25 certificate valid?

The certificate is valid for the period of the underlying policy. Once a policy expires or is cancelled, the certificate is no longer valid. Certificate holders should request updated certificates whenever coverage renews.

Q. What happens if there is an error on an ACORD 25?

If a certificate holder identifies an error, the issuing agent must reissue a corrected certificate. Errors in coverage limits, insurer names, or policy dates can cause contract delays or disputes, which is why accuracy at the point of issuance is critical.

Q. Can the ACORD 25 be issued electronically?

Yes. Electronic issuance and delivery of ACORD 25 certificates is standard practice. The form must still bear an authorized representative's signature, which can be electronic in most jurisdictions.

Q. What causes the most delays in ACORD 25 processing?

The most common causes of delay are manual data entry errors, missing endorsement information, high request volume during renewal periods, and non-standard certificate holder requirements that require underwriter review before issuance.