If you work in insurance, you’ve encountered an ACORD form. And if your work touches business-auto policies, you’ve almost certainly handled ACORD 127, the dense yet indispensable sheet that every broker, agent, and underwriter depends on.

In 2026, these forms are more than paperwork; they’re the data backbone of the commercial-auto ecosystem. Let’s explore what ACORD 127 is, why it matters, and how automation is changing the game for insurance teams.

What Is ACORD 127

ACORD 127 is the Business Auto Section form used to document a commercial policyholder’s vehicle-related exposures, company-owned or leased vehicles, employed drivers, and coverage selections.

It captures every detail an insurer needs to understand an insured business’s auto risk, who drives, what’s being driven, and how it’s used. In the U.S., about 90 percent of agencies rely on ACORD forms to share policy and claims data across systems (nasasoft.com & acords.com).

This single standard keeps communication clean between carriers, agents, and risk teams, one language, one layout, fewer misunderstandings.

Relation Between ACORD 125, 127, 129, and 137 Forms

ACORD 127 rarely travels alone, which highlights the need to automate ACORD 126 workflows alongside related forms for complete underwriting readiness. It’s part of a family that keeps commercial auto underwriting organized:

- ACORD 125 – the master application covering the insured business’s general info (legal name, address, operations).

- ACORD 127 – the auto-specific section (vehicles, drivers, usage).

- ACORD 129 – the driver supplement with detailed individual records.

- ACORD 137 – the state-specific add-on with required endorsements.

Together, they form a complete picture. Miss one, and the entire submission stalls.

Importance of ACORD 127 in Commercial Auto Insurance

ACORD 127 plays a central role in commercial auto insurance because it standardizes how exposure information is captured and shared. Its consistent structure removes guesswork and helps every team, from brokers to underwriters and auditors, work from the same reliable foundation. Here’s how each group benefits from it:

Why ACORD 127 Is Universally Recognized and Valuable

For Brokers

- Standardized format used industry-wide, allowing brokers to send the same application to multiple carriers.

- Eliminates the need to re-key data, reducing manual work and preventing errors.

- Speeds up submissions, improving quoting efficiency and turnaround time.

For Underwriters

- Highly predictable structure, with every question clearly defined.

- Enables precise risk evaluation, thanks to clean, organized data.

- Suitable for all fleet sizes, from a couple of vehicles to large commercial fleets.

- Provides structured insight, helping underwriters price risk accurately and consistently.

For Auditors and Claims Teams

- Acts as the source-of-truth document, capturing original exposure details.

- Useful for audits, reviews, and claim investigations, when verifying earlier information.

- Strengthens traceability, helping teams confirm what was submitted and when.

How Acord 127 Streamlines Submission and Underwriting

Without ACORD 127, submissions would look like digital chaos, with different layouts, random spreadsheets, and endless clarifying emails.

With it, everything aligns: driver lists, VINs, garaging ZIPs, and liability limits flow in a uniform format. This structure allows carriers to auto-ingest data into their rating or policy-admin systems. Agents spend less time reformatting and more time advising clients. In short, ACORD 127 converts potential confusion into clean, structured intelligence.

How to Complete the ACORD 127 Form (Step-by-Step)

Filling out ACORD 127 isn’t rocket science, just a matter of accuracy and attention. Here’s a simple walkthrough.

Driver Information Section

List each driver’s full name, license number, issuing state, and driving experience. This section forms the basis for driver eligibility. Always make sure the names here match those in ACORD 129; any mismatch delays processing.

General Information (17 Standard Questions)

These questions reveal how the vehicles are used — leased, owned, or non-owned. They also cover the radius of operation, contract requirements, and driver supervision.

Underwriters rely heavily on these answers. For example, “radius of operation” separates local delivery risks from long-haul transport risks, directly influencing premiums.

Additional Interest and Certificate Holders

Here, you record lienholders, lessors, and other interested parties needing proof of coverage. Type names exactly as they appear in official agreements. A single typo can delay certificates or trigger compliance flags.

Vehicle Description and Usage

VIN, year, make, model, cost new, and territory codes; every data point matters. Underwriters use this to evaluate exposure. Missing or transposed digits can cause quoting delays or even policy rejections.

Hired & Non-Owned Auto Coverage

This section applies when employees use personal or rented vehicles for business purposes. It’s often skipped by smaller companies, but that’s risky. If an employee crashes their own car while making a delivery, this coverage decides who pays.

Signatures and Final Review

Always confirm effective dates, signatures, and correct form versions before submission. Electronic portals may flag missing details automatically, but paper submissions still depend on human diligence.

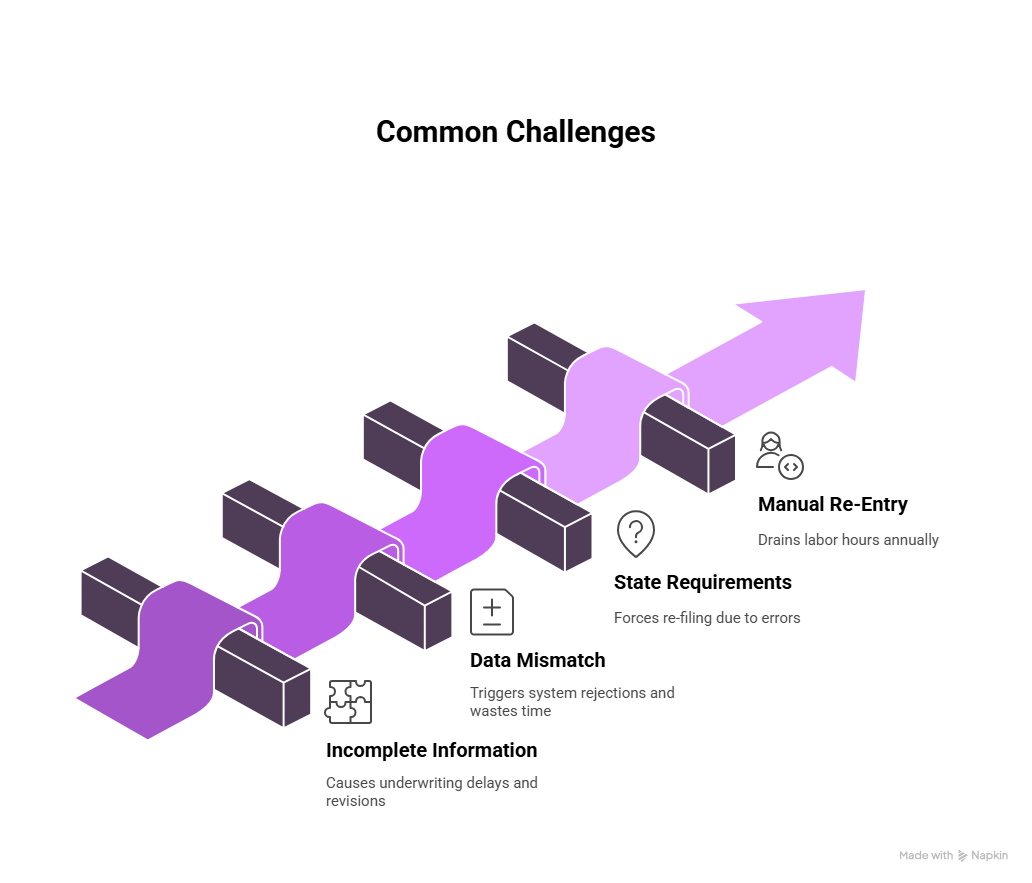

Common Challenges When Filling Out ACORD 127

Even with clear instructions, ACORD 127 can still trip up experienced professionals. The form’s structured layout hides plenty of small traps, from mismatched vehicle counts to overlooked state requirements. Because each field connects to another, a single missing entry can snowball into delays, resubmissions, or even compliance issues. Let’s look at the most common challenges insurance teams face when completing this form and how to avoid them.

Incomplete Driver or Vehicle Information

Leaving out driver license numbers, garaging addresses, or VINs leads to instant underwriting delays. What feels like “minor cleanup later” usually turns into a frustrating chain of revision requests.

Data Mismatch Across Multiple Forms

ACORD 125 lists ten vehicles; ACORD 127 lists nine, which is an automatic red flag. Such inconsistencies cause system rejections and waste underwriting time.

State-Specific Requirements and Filing Errors

Each state requires its own ACORD 137. Forgetting one or misaligning codes between forms forces re-filing. Most agencies now maintain internal validation checklists or use automation that pre-checks mandatory state fields.

Manual Re-Entry and Processing Delays

Brokers still manually copy data from PDFs into AMS or CRM systems. Every re-entry adds seconds that turn into hours by week’s end.

Industry studies show that manual ACORD processing drains thousands of labor hours annually, hours better spent on clients, not keyboards.

Why Manual ACORD 127 Processing Slows Teams Down

Manual processing of ACORD 127 forms might feel routine, but it’s one of the biggest silent productivity drains in commercial insurance. Each form demands repetitive data entry, double-checking, and cross-referencing across multiple systems. What looks like “simple paperwork” often balloons into hours of clerical work, eating into valuable time brokers and underwriters could spend on client relationships or revenue-generating tasks. Here’s why relying on manual processes slows entire teams down.

Error Rates and Rework Costs

Manual entry error rates are high in insurance workflows. Each correction consumes time, and a single error in VIN or driver data can ripple into billing and claims mismatches.

Multiply that across hundreds of policies, and rework costs become eye-watering.

Lost Time in Manual Verification

Underwriters often spend hours verifying submissions. A wrong policy effective date or a missing signature might pause a quote for days.

Manual reviews slow down quote-to-bind cycles, leaving revenue on the table. That’s exactly why 2026 is the year automation takes the wheel.

Automating ACORD 127 Processing in 2026

Modern AI-powered Intelligent Document Processing (IDP) platforms can read ACORD 127 forms like seasoned underwriters. They detect fields, extract text, and even interpret handwritten notes or checkboxes.

The best systems combine OCR for character reading, NLP for context, and validation rules aligned with ACORD standards. Result: faster, cleaner, and fully auditable data capture.

Step-by-Step Workflow for Acord 127 Automation

- Ingest Forms: Scan or upload ACORD 127 PDFs to the automation portal.

- Extract Fields: AI models identify and capture each data point (driver, VIN, limit).

- Validate Data: Cross-check against ACORD 125 and 129 to spot mismatches.

- Route for Review: Low-confidence items go to a review queue (usually less than 5 percent of fields).

- Sync Systems: Approved data flows into AMS, CRM, and policy-admin platforms in real time.

- Archive and Audit: Every action is timestamped for regulatory transparency.

Integration with AMS, CRM, and Policy Systems

Modern IDP tools connect directly with Agency Management Systems (AMS), Customer Relationship Management (CRM) tools, and Policy Administration Systems (PAS). This means no more copy-paste between platforms — data flows instantly, reducing turnaround from days to minutes.

Advantages of Automated ACORD 127 Processing

Automating ACORD 127 processing isn’t just about speed; it’s about reclaiming control over accuracy, compliance, and operational costs. By letting AI handle repetitive data capture, insurers and brokers can focus on underwriting decisions instead of field validation. The result? Faster submissions, fewer reworks, and a smoother experience for both carriers and policyholders.

Speed and Accuracy Improvements

Automation doesn’t just shave seconds; it transforms the entire workflow. When ACORD 127 data is captured through AI-driven extraction, every field is read, validated, and uploaded in seconds instead of minutes. That means a submission that once took an hour to prepare can now move from inbox to underwriting in under five minutes.

Accuracy improves, too. Automated extraction tools apply built-in validation rules, checking VIN formats, matching driver details with ACORD 129, and flagging missing fields before submission. This prevents costly back-and-forth emails and form rejections.

The outcome is measurable: insurers see faster quoting cycles, brokers spend less time cleaning data, and clients (the insured businesses) experience quicker policy issuance. The result? More quotes issued per day, fewer errors to fix, and a lot less frustration for everyone involved.

Compliance and Audit Readiness

Automation automatically records every extracted, verified, or corrected field. Each action is timestamped, creating a ready-to-share audit log. This traceability eliminates guesswork during reviews and makes compliance reporting effortless. Auditors get clear visibility into every data change without manual digging.

Lower Operational Costs

Manual ACORD processing consumes time and labor. Automation reduces both. Analyst data shows that digitizing ACORD workflows with AI can lower U.S. P&C insurer costs by roughly 14.6 percent—about $480 billion a year. The savings come from shorter processing cycles and fewer human touchpoints. Agencies benefit too: with automated entry, one account manager can handle more quotes in the same time, more output per employee, and less overhead per policy.

Implementation Checklist for Automation

Implementing ACORD 127 automation takes planning. The goal isn’t just to add new software, it’s to redesign how data moves through your organization. A clear checklist helps teams identify gaps, measure results, and scale efficiently. Here’s a quick roadmap to get started.

Readiness Assessment

Start by identifying where your team still touches data manually. Is it at intake, validation, or export? Knowing the friction points guides your automation roadmap.

Pilot Plan and Metrics

Begin small, automate one form type (say, ACORD 127 for renewals). Track metrics like average handling time, accuracy rate, and staff hours saved. If the results cut cycle time in half, expand.

Scaling Automation Across Teams

Once workflows prove stable, extend automation to ACORD 125, 129, and 137. Create internal champions, tech-savvy underwriters who help others adapt. Automation succeeds fastest when teams feel ownership of the new process.

ROI and Business Impact of Automating ACORD 127

The impact of automating ACORD 127 goes beyond convenience; it directly affects profitability and turnaround time. Faster submissions, cleaner data, and reduced manual effort create measurable returns within months. Here’s how automation translates into real business value for insurers, brokers, and risk teams.

Reduction in Turnaround Time

Automated extraction means submissions reach underwriting faster. What once took days now lands in a carrier’s system in minutes. That speed lets agents deliver quotes ahead of competitors.

Improved Data Quality and Customer Experience

Accurate data reduces back-and-forth with insured businesses. Clients (the policyholders) notice when coverage gets bound quickly and cleanly. Fewer errors also mean fewer billing corrections later, a quiet win for everyone.

How Infrrd Processes ACORD Forms

Infrrd simplifies how insurance teams handle ACORD forms, whether it’s ACORD 125, 126, 127, or 137, by automating document-heavy insurance workflows. Instead of manually re-keying driver, vehicle, or coverage data, Infrrd’s AI engine reads, understands, and validates every field automatically.

1. Multi-Format Data Extraction

Infrrd’s platform can extract data from both typed and handwritten ACORD forms. Whether the submission comes in as a clean digital PDF or a scanned image, the system detects all standard ACORD fields, names, VINs, policy numbers, driver details, and converts them into usable structured data within seconds.

2. Pre-Trained AI Models for Insurance

The engine is trained on millions of insurance documents, which means it already understands how ACORD layouts are structured. That allows Infrrd to recognize variations across versions and carriers without needing manual templates. It’s especially useful for ACORD 127, where vehicle and driver sections can differ depending on policy type.

3. Validation and SLA Prioritization

Infrrd doesn’t stop at extraction. It checks for accuracy using predefined business rules—matching driver names to ACORD 129, validating VIN formats, and ensuring state codes align with ACORD 137. Its SLA-based prioritization pushes time-sensitive submissions, like renewals or high-value accounts, to the front of the queue.

4. Seamless Integration with Core Systems

Once verified, extracted data flows directly into agency management systems (AMS), CRMs, or policy administration platforms. That eliminates manual re-entry, reduces turnaround time, and allows underwriters to start evaluation immediately.

5. Built-In Audit and Compliance Tracking

Every data action—extraction, correction, or approval- is logged automatically. This creates a ready-to-share audit trail that satisfies compliance checks and regulatory reviews without extra effort.

6. Real Business Outcomes

Infrrd’s automation cuts manual review work by up to 70 percent and helps teams process more policies with the same headcount. Agencies see measurable productivity gains, more quotes per employee, fewer data errors, and faster submissions.

In a Nutshell

ACORD 127 may look like just another form, but it’s the backbone of commercial-auto underwriting. With automation steering the wheel, insurers and agencies are finally shifting from paperwork to pure decision-making, and that’s a ride worth taking.

FAQs About ACORD 127

Q1. What is the purpose of ACORD 127?

ACORD 127 is designed to capture a commercial policyholder’s complete auto exposure, including vehicle types, usage, values, radius of operation, and other rating factors. Carriers rely on this form to understand the risk profile of each vehicle listed on a policy. By standardizing how data is collected, ACORD 127 helps insurers evaluate risk consistently, compare submissions across brokers, and price coverage with greater accuracy.

Q2. Who fills out the ACORD 127 form?

The form is typically completed by the insurance agent or broker, who gathers the necessary details from the insured business. After collecting all information—such as vehicle specs, business use, and operational details—brokers submit the completed ACORD 127 to one or more carriers for quoting. This helps ensure the submission is complete, accurate, and structured in a format carriers can easily process.

Q3. What is the difference between ACORD 127 and ACORD 129?

ACORD 127 focuses on the vehicles, capturing specifics like make, model, VIN, usage, and other exposures tied to the fleet.

ACORD 129, on the other hand, focuses on the drivers, listing who operates the vehicles and detailing their licenses, experience, and driving history.

Both forms work together—carriers need exposure on both the vehicles and the people driving them for a full commercial auto submission.

Q4. Can ACORD 127 be automated using AI?

Yes. Modern Intelligent Document Processing (IDP) systems can read scanned or digital ACORD 127 forms, extract every field, and validate it against business rules or third-party data. AI can detect inconsistencies, flag missing fields, normalize formats (like VIN or mileage), and send structured data directly into underwriting or policy administration systems. This reduces the dependency on manual entry and speeds up processing significantly.

Q5. How does automation help underwriters and brokers?

Automation removes the need for brokers to manually type data into carrier portals or spreadsheets, cutting hours of administrative work per submission. It also reduces the risk of errors caused by re-keying information from forms. Underwriters receive cleaner, standardized data faster, allowing them to focus on evaluating risk instead of hunting for missing information. The result is quicker quoting, higher submission quality, and more time for brokers to manage client relationships rather than paperwork.

Priyanka Joy is a product writer at Infrrd who approaches automation tech like a curious detective. With a love for research and storytelling, she turns technical depth into clarity. When not writing, she’s immersed in dance, theatre, or crafting her next narrative.