Wenn Sie in der Versicherung arbeiten, sind Sie auf ein ACORD-Formular gestoßen. Und wenn es bei Ihrer Arbeit um Versicherungspolicen für Unternehmen geht, haben Sie das mit ziemlicher Sicherheit erledigt AKKORD 127, das dichte und doch unverzichtbare Blatt, auf das jeder Makler, Agent und Underwriter angewiesen ist.

Im Jahr 2026 sind diese Formulare mehr als nur Papierkram; sie sind das Datenrückgrat des Nutzfahrzeug-Ökosystems. Lassen Sie uns untersuchen, was ACORD 127 ist, warum es wichtig ist und wie die Automatisierung die Spielregeln für Versicherungsteams verändert.

Was ist ACORD 127

AKKORD 127 ist der Bereich Business Auto Formular, das verwendet wurde, um eine zu dokumentieren gewerblicher Versicherungsnehmer fahrzeugseitige Risiken, firmeneigene oder geleaste Fahrzeuge, angestellte Fahrer und Deckungsoptionen.

Es erfasst jedes Detail, das ein Versicherer benötigt, um das Autorisiko eines versicherten Unternehmens zu verstehen, wer fährt, was gesteuert wird und wie es genutzt wird. In den USA etwa 90 Prozent der Agenturen verlassen sich auf ACORD-Formulare, um Policen- und Schadensdaten systemübergreifend auszutauschen (nasasoft.com & acords.com).

Dieser einheitliche Standard sorgt für eine saubere Kommunikation zwischen Spediteuren, Agenten und Risikoteams, eine Sprache, ein Layout, weniger Missverständnisse.

Beziehung zwischen den Formularen ACORD 125, 127, 129 und 137

ACORD 127 reist selten alleine. Er gehört zu einer Familie, die die gewerbliche Kfz-Versicherungspolice organisiert:

- AKKORD 125 — den Hauptantrag mit den allgemeinen Informationen des versicherten Unternehmens (Firmenname, Adresse, Geschäftstätigkeit).

- AKKORD 127 — der autospezifische Bereich (Fahrzeuge, Fahrer, Nutzung).

- AKKORD 129 — die Fahrerbeilage mit detaillierten Einzelaufzeichnungen.

- AKKORD 137 — das landesspezifische Add-on mit den erforderlichen Vermerken.

Zusammen bilden sie ein vollständiges Bild. Fehlt eine, gerät die gesamte Einreichung ins Stocken.

Bedeutung von ACORD 127 in der gewerblichen Autoversicherung

ACORD 127 spielt eine zentrale Rolle in der gewerblichen Autoversicherung, da es standardisiert, wie Risikoinformationen erfasst und weitergegeben werden. Die einheitliche Struktur macht Rätselraten überflüssig und hilft allen Teams, von Maklern über Versicherer bis hin zu Wirtschaftsprüfern, auf derselben zuverlässigen Grundlage zu arbeiten. So profitiert jede Gruppe davon:

Warum ACORD 127 allgemein anerkannt und wertvoll ist

Für Makler

- Branchenweit verwendetes standardisiertes Format, sodass Makler denselben Antrag an mehrere Spediteure senden können.

- Macht das erneute Eingeben von Daten überflüssig, reduziert die manuelle Arbeit und verhindert Fehler.

- Beschleunigt Einreichungen, wodurch die Effizienz der Angebotserstellung und die Bearbeitungszeit verbessert werden.

Für Underwriter

- Hochgradig vorhersehbare Struktur, wobei jede Frage klar definiert ist.

- Ermöglicht eine präzise Risikobewertung, dank sauberer, organisierter Daten.

- Geeignet für alle Flottengrößen, von ein paar Fahrzeugen bis hin zu großen kommerziellen Flotten.

- Bietet strukturierte Einblickeund hilft Versicherern dabei, Risiken genau und konsistent zu bewerten.

Für Wirtschaftsprüfer und Schadenteams

- Fungiert als Dokument zur Informationsquelle, um die ursprünglichen Belichtungsdetails zu erfassen.

- Nützlich für Audits, Überprüfungen und Schadensuntersuchungen, bei der Überprüfung früherer Informationen.

- Verstärkt die Rückverfolgbarkeitund hilft den Teams dabei, zu bestätigen, was wann eingereicht wurde.

Wie Acord 127 Einreichung und Underwriting optimiert

Ohne ACORD 127 würden Einreichungen wie ein digitales Chaos aussehen, mit unterschiedlichen Layouts, zufälligen Tabellen und endlosen klärenden E-Mails.

Damit stimmt alles überein: Fahrerlisten, VINs, Garaging-ZIPs und Haftungslimits fließen in einem einheitlichen Format zusammen. Diese Struktur ermöglicht es den Spediteuren automatische Aufnahme Daten in ihre Bewertungs- oder Policy-Admin-Systeme. Agenten verbringen weniger Zeit mit der Neuformatierung und mehr Zeit mit der Beratung von Kunden. Kurz gesagt, ACORD 127 wandelt potenzielle Verwirrung in saubere, strukturierte Informationen um.

So füllen Sie das ACORD 127-Formular aus (Schritt für Schritt)

Das Ausfüllen von ACORD 127 ist kein Hexenwerk, sondern nur eine Frage der Genauigkeit und Aufmerksamkeit. Hier ist eine einfache Anleitung.

Abschnitt mit Fahrerinformationen

Geben Sie für jeden Fahrer den vollständigen Namen, die Lizenznummer, den Ausstellungsstaat und die Fahrerfahrung an. Dieser Abschnitt bildet die Grundlage für die Eignung eines Fahrers. Stellen Sie immer sicher, dass die Namen hier mit denen in ACORD 129 übereinstimmen. Jede Nichtübereinstimmung verzögert die Bearbeitung.

Allgemeine Informationen (17 Standardfragen)

Diese Fragen geben Aufschluss darüber, wie die Fahrzeuge genutzt werden — geleast, im eigenen Besitz oder als Fremdfahrzeug. Sie decken auch den Einsatzradius, die vertraglichen Anforderungen und die Fahreraufsicht ab.

Versicherer verlassen sich stark auf diese Antworten. So trennt beispielsweise der „Einsatzradius“ lokale Lieferrisiken von Ferntransportrisiken und wirkt sich direkt auf die Prämien aus.

Weitere Interessenten und Zertifikatsinhaber

Hier erfassen Sie Pfandinhaber, Vermieter und andere Interessenten, die einen Versicherungsnachweis benötigen. Geben Sie die Namen genau so ein, wie sie in offiziellen Vereinbarungen stehen. Ein einziger Tippfehler kann Zertifikate verzögern oder Konformitätskennzeichen auslösen.

Fahrzeugbeschreibung und Verwendung

VIN, Jahr, Marke, Modell, Neupreis und Gebietscode; jeder Datenpunkt ist wichtig. Versicherer nutzen dies, um das Risiko zu bewerten. Fehlende oder vertauschte Ziffern können zu Verzögerungen bei der Angebotserstellung oder sogar zur Ablehnung von Versicherungsverträgen führen.

Versicherungsschutz für gemietete und nicht eigene Autos

Dieser Abschnitt gilt, wenn Mitarbeiter private oder gemietete Fahrzeuge für geschäftliche Zwecke nutzen. Es wird oft von kleineren Unternehmen übersprungen, aber das ist riskant. Wenn ein Mitarbeiter bei der Lieferung mit seinem eigenen Auto einen Unfall hat, entscheidet dieser Versicherungsschutz darüber, wer bezahlt.

Unterschriften und abschließende Überprüfung

Bestätigen Sie vor dem Absenden immer das Datum des Inkrafttretens, die Unterschriften und die korrekten Formularversionen. Elektronische Portale können fehlende Angaben automatisch kennzeichnen, aber das Einreichen von Unterlagen hängt immer noch von menschlicher Sorgfalt ab.

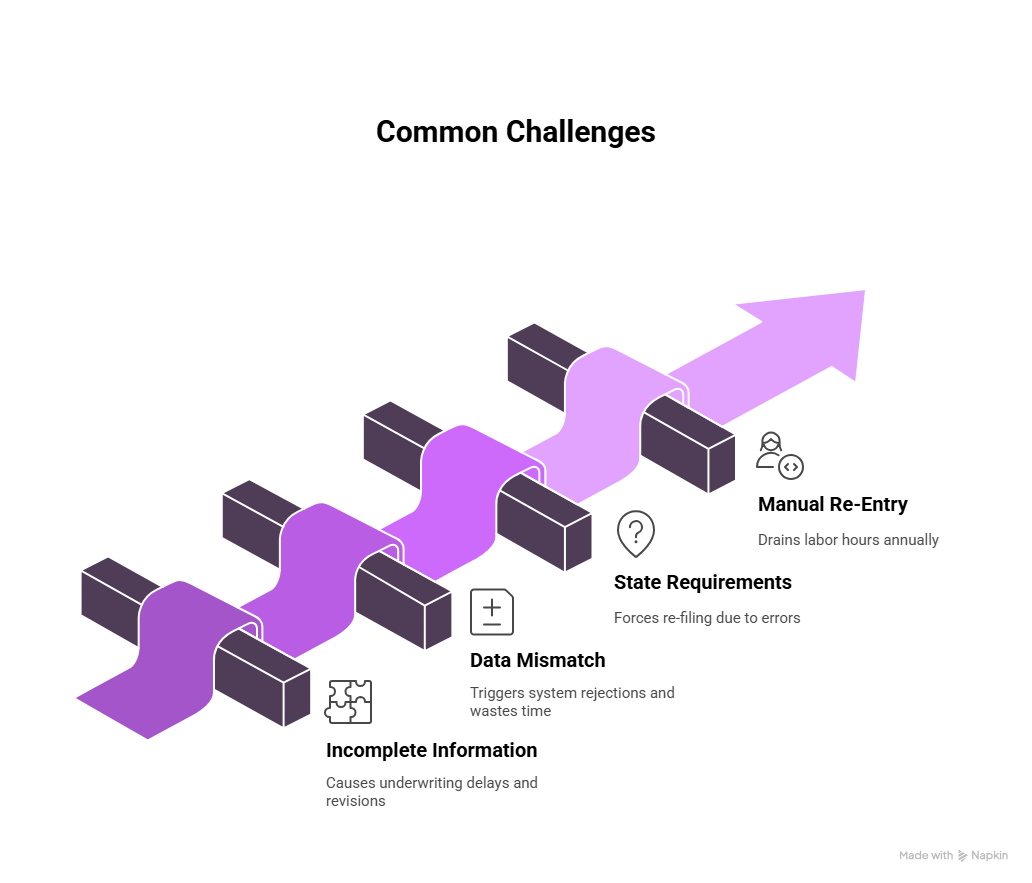

Häufige Herausforderungen beim Ausfüllen von ACORD 127

Selbst mit klaren Anweisungen kann ACORD 127 erfahrene Profis immer noch überfordern. Das strukturierte Layout des Formulars verbirgt viele kleine Fallen, von nicht übereinstimmenden Fahrzeugangaben bis hin zu übersehenen staatlichen Anforderungen. Da jedes Feld mit einem anderen verknüpft ist, kann ein einziger fehlender Eintrag zu Verzögerungen, erneuten Eingaben oder sogar zu Problemen mit der Einhaltung der Vorschriften führen. Schauen wir uns die häufigsten Herausforderungen an, mit denen Versicherungsteams beim Ausfüllen dieses Formulars konfrontiert sind, und wie sie vermieden werden können.

Unvollständige Fahrer- oder Fahrzeuginformationen

Das Auslassen von Führerscheinnummern, Garagenadressen oder VINs führt zu sofortigen Verzögerungen bei der Versicherungsprüfung. Was sich wie eine „kleine Säuberung später“ anfühlt, wird in der Regel zu einer frustrierenden Kette von Revisionsanfragen.

Daten stimmen in mehreren Formularen nicht überein

ACORD 125 listet zehn Fahrzeuge auf; ACORD 127 listet neun auf, was eine automatische rote Flagge ist. Solche Inkonsistenzen führen zu Systemablehnungen und vergeuden Versicherungszeit.

Landesspezifische Anforderungen und Anmeldefehler

Jeder Staat benötigt seinen eigenen ACORD 137. Wenn Sie eines vergessen oder die Codes zwischen den Formularen falsch ausgerichtet sind, müssen Sie es erneut einreichen. Die meisten Behörden führen jetzt interne Validierungs-Checklisten oder verwenden eine Automatisierung, die die Pflichtfelder des Bundesstaats vorab überprüft.

Manuelle Wiedereingabe und Verzögerungen bei der Bearbeitung

Makler kopieren Daten immer noch manuell aus PDFs in AMS- oder CRM-Systeme. Bei jeder erneuten Eingabe werden Sekunden hinzugefügt, aus denen am Wochenende Stunden werden.

Branchenstudien zeigen, dass die manuelle ACORD-Verarbeitung jährlich Tausende von Arbeitsstunden kostet — Stunden, die besser für Kunden als für Tastaturen verwendet werden sollten.

Warum die manuelle ACORD 127-Verarbeitung Teams verlangsamt

Die manuelle Bearbeitung von ACORD 127-Formularen mag sich routinemäßig anfühlen, ist aber einer der größten stillen Produktivitätseinbußen in der gewerblichen Versicherung. Jedes Formular erfordert eine wiederholte Dateneingabe, doppelte Überprüfung und Querverweise in mehreren Systemen. Was wie „einfacher Papierkram“ aussieht, mündet oft in stundenlange Büroarbeit, was wertvolle Zeit in Anspruch nimmt, die Makler und Versicherer für Kundenbeziehungen oder umsatzgenerierende Aufgaben aufwenden könnten. Aus diesem Grund verlangsamt es ganze Teams, sich auf manuelle Prozesse zu verlassen.

Fehlerraten und Nacharbeitskosten

Die Fehlerquote bei manueller Eingabe ist in Versicherungsabläufen hoch. Jede Korrektur nimmt Zeit in Anspruch, und ein einziger Fehler in der Fahrgestellnummer oder in den Fahrerdaten kann dazu führen, dass Rechnungen und Ansprüche nicht übereinstimmen.

Multiplizieren Sie das mit Hunderten von Policen, und die Kosten für Nacharbeiten laufen einem ins Auge.

Verlorene Zeit bei manueller Überprüfung

Versicherer verbringen oft Stunden damit, Einreichungen zu überprüfen. Ein falsches Datum des Inkrafttretens der Richtlinie oder eine fehlende Unterschrift kann dazu führen, dass ein Angebot tagelang unterbrochen wird.

Manuelle Überprüfungen verlangsamen die Zyklen von Angebot zu Angebot, sodass der Umsatz auf dem Tisch bleibt. Genau aus diesem Grund ist 2026 das Jahr, in dem die Automatisierung das Steuer übernimmt.

Automatisierung der ACORD 127-Verarbeitung im Jahr 2026

modern KI-gestützte intelligente Dokumentenverarbeitung (IDP) Plattformen können ACORD 127-Formulare wie erfahrene Versicherer lesen. Sie erkennen Felder, extrahieren Text und interpretieren sogar handschriftliche Notizen oder Kontrollkästchen.

Die besten Systeme kombinieren OCR für das Lesen von Zeichen, NLP für den Kontext und Validierungsregeln, die den ACORD-Standards entsprechen. Ergebnis: schnellere, sauberere und vollständig überprüfbare Datenerfassung.

Schrittweiser Arbeitsablauf für Acord 127 Automation

- Formulare aufnehmen: Scannen Sie ACORD 127-PDFs oder laden Sie sie in das Automatisierungsportal hoch.

- Felder extrahieren: KI-Modelle identifizieren und erfassen jeden Datenpunkt (Treiber, VIN, Limit).

- Daten validieren: Vergleichen Sie mit ACORD 125 und 129, um Unstimmigkeiten zu erkennen.

- Route zur Überprüfung: Artikel mit geringer Vertrauenswürdigkeit werden in eine Bewertungswarteschlange aufgenommen (normalerweise weniger als 5 Prozent der Felder).

- Systeme synchronisieren: Genehmigte Daten fließen in Echtzeit in AMS-, CRM- und Policy-Admin-Plattformen.

- Archivieren und Audit: Jede Maßnahme ist aus Gründen der regulatorischen Transparenz mit einem Zeitstempel versehen.

Integration mit AMS-, CRM- und Richtliniensystemen

Moderne IDP-Tools sind direkt mit Agency Management Systems (AMS), Customer Relationship Management (CRM) -Tools und Policy Administration Systems (PAS) verbunden. Das bedeutet, dass kein Kopieren und Einfügen zwischen Plattformen mehr erforderlich ist — die Daten fließen sofort, wodurch die Bearbeitungszeit von Tagen auf Minuten reduziert wird.

Vorteile der automatisierten ACORD 127-Verarbeitung

Automatisierung der ACORD 127-Verarbeitung geht es nicht nur um Geschwindigkeit, sondern auch darum, die Kontrolle über Genauigkeit, Konformität und Betriebskosten zurückzugewinnen. Da die KI die sich wiederholende Datenerfassung übernimmt, können sich Versicherer und Makler auf versicherungstechnische Entscheidungen konzentrieren, anstatt sie vor Ort zu validieren. Das Ergebnis? Schnellere Einreichungen, weniger Nacharbeiten und ein reibungsloseres Erlebnis für Fluggesellschaften und Versicherungsnehmer.

Verbesserungen bei Geschwindigkeit und Genauigkeit

Automatisierung spart nicht nur Sekunden, sie transformiert den gesamten Arbeitsablauf. Wenn ACORD 127-Daten durch KI-gestützte Extraktion erfasst werden, wird jedes Feld in Sekunden statt in Minuten gelesen, validiert und hochgeladen. Das bedeutet, dass eine Einreichung, deren Vorbereitung früher eine Stunde gedauert hat, jetzt in weniger als fünf Minuten vom Posteingang zum Underwriting übertragen werden kann.

Die Genauigkeit verbessert sich ebenfalls. Automatisierte Extraktionstools wenden integrierte Validierungsregeln an, überprüfen VIN-Formate, gleichen Treiberdetails mit ACORD 129 ab und kennzeichnen fehlende Felder vor dem Absenden. Dies verhindert kostspieliges Hin und Her von E-Mails und das Ablehnen von Formularen.

Das Ergebnis ist messbar: Versicherer erleben schnellere Angebotszyklen, Makler verbringen weniger Zeit mit der Bereinigung von Daten und Kunden (die versicherten Unternehmen) können Policen schneller ausstellen. Das Ergebnis? Mehr Angebote pro Tag, weniger Fehler, die behoben werden müssen, und viel weniger Frust für alle Beteiligten.

Einhaltung von Vorschriften und Auditbereitschaft

Die Automatisierung zeichnet automatisch jedes extrahierte, verifizierte oder korrigierte Feld auf. Jede Aktion wird mit einem Zeitstempel versehen, wodurch ein Audit-Protokoll erstellt wird, das sofort geteilt werden kann. Diese Rückverfolgbarkeit macht Rätselraten bei Überprüfungen überflüssig und macht die Erstellung von Compliance-Berichten zum Kinderspiel. Auditoren erhalten einen klaren Überblick über jede Datenänderung, ohne dass sie manuell nachforschen müssen.

Niedrigere Betriebskosten

Die manuelle ACORD-Verarbeitung erfordert Zeit und Arbeit. Die Automatisierung reduziert beides. Analystendaten zeigen, dass die Digitalisierung von ACORD-Workflows mit KI die Kosten von US-P&C-Versicherern um ungefähr senken kann 14,6 Prozent — etwa 480 Milliarden US-Dollar ein Jahr. Die Einsparungen sind auf kürzere Verarbeitungszyklen und weniger menschliche Kontaktpunkte zurückzuführen. Auch Agenturen profitieren: Durch die automatische Erfassung kann ein Kundenbetreuer mehrere Angebote gleichzeitig bearbeiten. mehr Leistung pro Mitarbeiter und weniger Gemeinkosten pro Police.

Implementierungscheckliste für die Automatisierung

Die Implementierung der ACORD 127-Automatisierung erfordert Planung. Das Ziel besteht nicht nur darin, neue Software hinzuzufügen, sondern auch die Art und Weise, wie Daten in Ihrem Unternehmen übertragen werden, neu zu gestalten. Eine klare Checkliste hilft Teams, Lücken zu identifizieren, Ergebnisse zu messen und effizient zu skalieren. Hier ist eine kurze Roadmap für den Einstieg.

Bewertung der Eignung

Identifizieren Sie zunächst, wo Ihr Team noch manuell mit Daten umgeht. Befinden sie sich bei der Aufnahme, Validierung oder beim Export? Wenn Sie die Reibungspunkte kennen, leiten Sie Ihren Automatisierungsfahrplan ab.

Pilotplan und Kennzahlen

Fangen Sie klein an und automatisieren Sie einen Formulartyp (z. B. ACORD 127 für Verlängerungen). Verfolgen Sie Kennzahlen wie die durchschnittliche Bearbeitungszeit, die Genauigkeitsrate und die eingesparten Personalstunden. Wenn die Ergebnisse die Zykluszeit um die Hälfte reduzieren, erweitern Sie.

Teamübergreifende Skalierung der Automatisierung

Sobald sich die Workflows als stabil erweisen, erweitern Sie die Automatisierung auf ACORD 125, 129 und 137. Schaffen Sie interne Champions, technisch versierte Versicherer, die anderen helfen, sich anzupassen. Automatisierung gelingt am schnellsten, wenn die Teams das Gefühl haben, für den neuen Prozess verantwortlich zu sein.

ROI und geschäftliche Auswirkungen der Automatisierung von ACORD 127

Die Auswirkungen der Automatisierung von ACORD 127 gehen über den Komfort hinaus; sie wirken sich direkt auf die Rentabilität und die Bearbeitungszeit aus. Schnellere Einreichungen, sauberere Daten und weniger manueller Aufwand sorgen für messbare Renditen innerhalb weniger Monate. So führt Automatisierung zu einem echten Geschäftswert für Versicherer, Makler und Risikoteams.

Verkürzung der Bearbeitungszeit

Automatisierte Extraktion bedeutet, dass Einreichungen schneller beim Underwriting ankommen. Was früher Tage gedauert hat, landet jetzt innerhalb von Minuten im System eines Spediteurs. Diese Geschwindigkeit ermöglicht es den Agenten, Angebote vor der Konkurrenz abzugeben.

Verbesserte Datenqualität und Kundenerlebnis

Präzise Daten reduzieren das Hin und Her mit versicherten Unternehmen. Kunden (die Versicherungsnehmer) merken, wenn der Versicherungsschutz schnell und sauber abgeschlossen wird. Weniger Fehler bedeuten auch später weniger Abrechnungskorrekturen, ein stiller Gewinn für alle.

Wie Infrarot ACORD-Formulare verarbeitet

Infrarot vereinfacht den Umgang von Versicherungsteams mit ACORD-Formularen, unabhängig davon, ob es sich um ACORD 125, 126, 127 oder 137 handelt, durch Automatisierung dokumentenintensive Versicherungsabläufe. Anstatt Fahrer-, Fahrzeug- oder Empfangsdaten manuell erneut einzugeben, liest, versteht und validiert die KI-Engine von Infrrd jedes Feld automatisch.

1. Datenextraktion in mehreren Formaten

Die Plattform von Infrrd kann Daten extrahieren sowohl aus getippten als auch aus handgeschriebenen ACORD-Formularen. Unabhängig davon, ob die Einreichung als sauberes digitales PDF oder als gescanntes Bild erfolgt, erkennt das System alle ACORD-Standardfelder, Namen, VINs, Policennummern und Fahrerdetails und wandelt sie innerhalb von Sekunden in nutzbare strukturierte Daten um.

2. Vortrainierte KI-Modelle für Versicherungen

Die Engine ist mit Millionen von Versicherungsdokumenten trainiert, was bedeutet, dass sie bereits versteht, wie ACORD-Layouts strukturiert sind. Auf diese Weise kann Infrrd Variationen zwischen Versionen und Anbietern erkennen, ohne dass manuelle Vorlagen erforderlich sind. Dies ist besonders nützlich für ACORD 127, wo sich Fahrzeug- und Fahrerbereiche je nach Versicherungstyp unterscheiden können.

3. Validierung und SLA-Priorisierung

Infrarot hört nicht bei der Extraktion auf. Es überprüft die Richtigkeit anhand vordefinierter Geschäftsregeln. Dabei werden Treibernamen mit ACORD 129 abgeglichen, VIN-Formate validiert und sichergestellt, dass die Statuscodes mit ACORD 137 übereinstimmen. Durch die SLA-basierte Priorisierung werden zeitkritische Einreichungen, wie Verlängerungen oder Konten mit hohem Wert, in der Warteschlange an den Anfang der Warteschlange gestellt.

4. Nahtlose Integration mit Kernsystemen

Nach der Überprüfung fließen die extrahierten Daten direkt in Behördenverwaltungssysteme (AMS), CRMs oder Plattformen für die Richtlinienverwaltung. Dadurch entfällt die manuelle Neueingabe, die Bearbeitungszeit wird reduziert und die Versicherer können sofort mit der Bewertung beginnen.

5. Integrierte Audit- und Compliance-Nachverfolgung

Jede Datenaktion — Extraktion, Korrektur oder Genehmigung — wird automatisch protokolliert. Dadurch entsteht ein Audit-Trail, der sofort mit anderen geteilt werden kann und der Konformitätsprüfungen und behördlichen Prüfungen ohne zusätzlichen Aufwand genügt.

6. Echte Geschäftsergebnisse

Die Automatisierung von Infrrd reduziert den manuellen Überprüfungsaufwand um bis zu 70 Prozent und hilft Teams, mehr Richtlinien mit derselben Mitarbeiterzahl zu bearbeiten. Agenturen verzeichnen messbare Produktivitätssteigerungen, mehr Angebote pro Mitarbeiter, weniger Datenfehler und schnellere Einreichungen.

Auf den Punkt gebracht

ACORD 127 sieht zwar wie eine weitere Form aus, ist aber das Rückgrat der gewerblichen Autoversicherung. Da die Automatisierung das Steuer lenkt, wechseln Versicherer und Agenturen endlich vom Papierkram zur reinen Entscheidungsfindung, und das ist eine Fahrt, die sich lohnt.

Häufig gestellte Fragen zu ACORD 127

Q1. Was ist der Zweck von ACORD 127?

ACORD 127 ist so konzipiert, dass es das komplette Autorisiko eines gewerblichen Versicherungsnehmers erfasst, einschließlich Fahrzeugtypen, Nutzung, Werte, Betriebsradius und anderer Bewertungsfaktoren. Fluggesellschaften verlassen sich auf dieses Formular, um das Risikoprofil jedes in einer Police aufgeführten Fahrzeugs zu verstehen. ACORD 127 standardisiert die Art und Weise, wie Daten erfasst werden, und hilft Versicherern, Risiken einheitlich zu bewerten, die Angaben der Makler zu vergleichen und die Versicherungsdeckung mit größerer Genauigkeit abzudecken.

Q2. Wer füllt das ACORD 127-Formular aus?

Das Formular wird in der Regel vom Versicherungsvertreter oder Makler ausgefüllt, der die erforderlichen Informationen vom versicherten Unternehmen einholt. Nach Erfassung aller Informationen — wie Fahrzeugspezifikationen, betrieblicher Nutzung und Betriebsdetails — reichen die Makler das ausgefüllte ACORD 127 an eine oder mehrere Spediteure zur Angebotsabgabe ein. Dadurch wird sichergestellt, dass die Einreichung vollständig, korrekt und in einem Format strukturiert ist, das die Spediteure problemlos verarbeiten können.

Q3. Was ist der Unterschied zwischen ACORD 127 und ACORD 129?

ACORD 127 konzentriert sich auf Fahrzeuge, wobei Angaben wie Marke, Modell, Fahrgestellnummer, Nutzung und andere mit der Flotte verbundene Risiken erfasst werden.

ACORD 129 konzentriert sich dagegen auf die Fahrer, in dem aufgeführt ist, wer die Fahrzeuge bedient, sowie deren Führerscheine, Erfahrung und Fahrhistorie detailliert beschrieben werden.

Beide Formen funktionieren zusammen — die Spediteure müssen sowohl über die Fahrzeuge als auch über die Personen, die sie fahren, informiert sein, um ein vollwertiges Fahrzeug einreichen zu können.

Q4. Kann ACORD 127 mithilfe von KI automatisiert werden?

Ja. Moderne Systeme zur intelligenten Dokumentenverarbeitung (IDP) können gescannte oder digitale ACORD 127-Formulare lesen, jedes Feld extrahieren und es anhand von Geschäftsregeln oder Daten von Drittanbietern validieren. KI kann Inkonsistenzen erkennen, fehlende Felder kennzeichnen, Formate (wie Fahrgestellnummer oder Kilometerstand) normalisieren und strukturierte Daten direkt an Versicherungs- oder Policenverwaltungssysteme senden. Dies reduziert die Abhängigkeit von manueller Eingabe und beschleunigt die Verarbeitung erheblich.

Q5. Wie hilft Automatisierung Versicherern und Maklern?

Durch die Automatisierung müssen Makler Daten nicht mehr manuell in Portale oder Tabellenkalkulationen eingeben, wodurch der Verwaltungsaufwand pro Einreichung um Stunden reduziert wird. Es reduziert auch das Risiko von Fehlern, die durch die erneute Eingabe von Informationen aus Formularen verursacht werden. Versicherer erhalten schneller sauberere, standardisierte Daten, sodass sie sich auf die Risikobewertung konzentrieren können, anstatt nach fehlenden Informationen zu suchen. Das Ergebnis ist eine schnellere Angebotserstellung, eine höhere Qualität der Einreichung und mehr Zeit für Makler, um die Kundenbeziehungen zu verwalten, anstatt den Papierkram zu erledigen.

Priyanka Joy ist Produktautorin bei Infrrd und nähert sich Automatisierungstechnik wie eine neugierige Detektivin. Mit ihrer Liebe zur Recherche und zum Geschichtenerzählen verwandelt sie technische Tiefe in Klarheit. Wenn sie nicht schreibt, vertieft sie sich in Tanz, Theater oder schreibt an ihrer nächsten Erzählung.

Häufig gestellte Fragen

Software zur Überprüfung und Prüfung von Hypotheken ist ein Sammelbegriff für Tools zur Automatisierung und Rationalisierung des Prozesses der Kreditbewertung. Es hilft Finanzinstituten dabei, die Qualität, die Einhaltung der Vorschriften und das Risiko von Krediten zu beurteilen, indem sie Kreditdaten, Dokumente und Kreditnehmerinformationen analysiert. Diese Software stellt sicher, dass Kredite den regulatorischen Standards entsprechen, reduziert das Fehlerrisiko und beschleunigt den Überprüfungsprozess, wodurch er effizienter und genauer wird.

Eine QC-Checkliste vor der Finanzierung besteht aus einer Reihe von Richtlinien und Kriterien, anhand derer die Richtigkeit, Einhaltung und Vollständigkeit eines Hypothekendarlehens überprüft und verifiziert werden, bevor Mittel ausgezahlt werden. Sie stellt sicher, dass das Darlehen den regulatorischen Anforderungen und internen Standards entspricht, wodurch das Risiko von Fehlern und Betrug verringert wird.

KI verwendet Mustererkennung und Natural Language Processing (NLP), um Dokumente genauer zu klassifizieren, selbst bei unstrukturierten oder halbstrukturierten Daten.

Ja, IDP kann Dokumenten-Workflows vollständig automatisieren, vom Scannen über die Datenextraktion und Validierung bis hin zur Integration mit anderen Geschäftssystemen.

Eine QC-Checkliste vor der Finanzierung ist hilfreich, da sie sicherstellt, dass ein Hypothekendarlehen vor der Finanzierung alle regulatorischen und internen Anforderungen erfüllt. Das frühzeitige Erkennen von Fehlern, Inkonsistenzen oder Compliance-Problemen reduziert das Risiko von Kreditmängeln, Betrug und potenziellen rechtlichen Problemen. Dieser proaktive Ansatz verbessert die Kreditqualität, minimiert kostspielige Verzögerungen und stärkt das Vertrauen der Anleger.

Wählen Sie eine Software, die fortschrittliche Automatisierungstechnologie für effiziente Audits, leistungsstarke Compliance-Funktionen, anpassbare Audit-Trails und Berichte in Echtzeit bietet. Stellen Sie sicher, dass sie sich gut in Ihre vorhandenen Systeme integrieren lässt und Skalierbarkeit, zuverlässigen Kundensupport und positive Nutzerbewertungen bietet.