AI is no longer a general idea in the mortgage industry. It is already showing up in document review, borrower communication, underwriting support, fraud checks, servicing, quality control, and audit preparation.

Still, many mortgage teams are asking the same question.

Is AI actually delivering?

The answer is yes, but not in the way many people first imagined.

AI is not walking into a lending office and replacing every loan officer, broker, underwriter, processor, and auditor. It is doing something more practical. It is taking over repetitive work, finding patterns in large loan files, flagging issues, and helping mortgage professionals make faster and better decisions.

That matters because mortgage work is still document-heavy. A single loan file can include income records, bank statements, tax documents, disclosures, credit reports, insurance documents, appraisal data, and compliance checks. Humans can review these files, but the work takes time. It also becomes harder when teams face volume spikes, missing documents, inconsistent formats, and tight closing timelines.

AI helps by turning loan data into usable information earlier in the process. It can classify documents, extract fields, compare information across files, and raise exceptions for review. It can also support decisioning, audit, servicing, and borrower communication.

This does not make the mortgage industry a fully machine-led process. Mortgage is still a trust-based business. Borrowers need guidance. Lenders need judgment. Underwriters need context. Auditors need evidence.

AI works best when it supports the human layer rather than trying to remove it.

Fannie Mae’s survey found that 30% of lenders had deployed or were trialing AI or machine learning, while 55% expected to start trials or expand use more broadly. The same report also found that operational efficiency had become the main reason lenders were adopting AI.

That tells us something important. AI in mortgage is not just hype. It is becoming a practical tool for teams that need speed, consistency, and better control over loan data.

The Evolution of the Mortgage Industry

The mortgage industry has always moved at the speed of trust, risk, and paperwork.

A borrower may think of a mortgage as one application. A lender sees a long chain of steps. Each step needs data, checks, rules, decisions, and proof. That is why mortgages have often been slower than other financial services.

Before AI, many digital mortgage efforts focused on moving forms online. Borrowers could upload documents through portals. Loan teams could use workflow tools. Some systems could pre-fill fields or route tasks.

That helped, but it did not solve the deeper issue.

The data inside mortgage documents still needed to be read, checked, compared, and validated. Digital did not always mean intelligent.

But AI started changing that by helping systems understand the document's context, not just store it.

Before AI Came Into Play in the Mortgage Industry

Before AI gained serious attention, mortgage teams relied heavily on manual review and rules-based systems.

- A processor would open documents, check fields, rename files, update systems, and send requests for missing items.

- Underwriters would review borrower information, compare documents, assess risk, and decide whether the file met guidelines.

- Quality control and audit teams would check completed loans for errors, missing data, or compliance issues.

This process worked, but it had clear limits. It was slow during high-volume periods. It depended heavily on team experience. It could produce inconsistent results when different people reviewed the same type of issue. It also made scaling harder because adding more volume often meant adding more people.

Traditional OCR helped in some areas. OCR could read text from a template document, but it could not always understand what the text meant. A mortgage document includes tables, stamps, handwritten notes, signatures, conditional fields, and data points spread across many pages. Reading characters is not the same as understanding the loan file.

That is why many mortgage teams ended up with partial automation.

They could move documents faster, but humans still had to fix the hard parts.

When AI Came Into Play in the Mortgage Industry?

AI entered the mortgage industry in stages.

At first, many systems used rules, decision trees, and basic automation. These tools helped with simple borrower journeys, eligibility checks, and task routing. They were helpful, but they were limited by fixed logic.

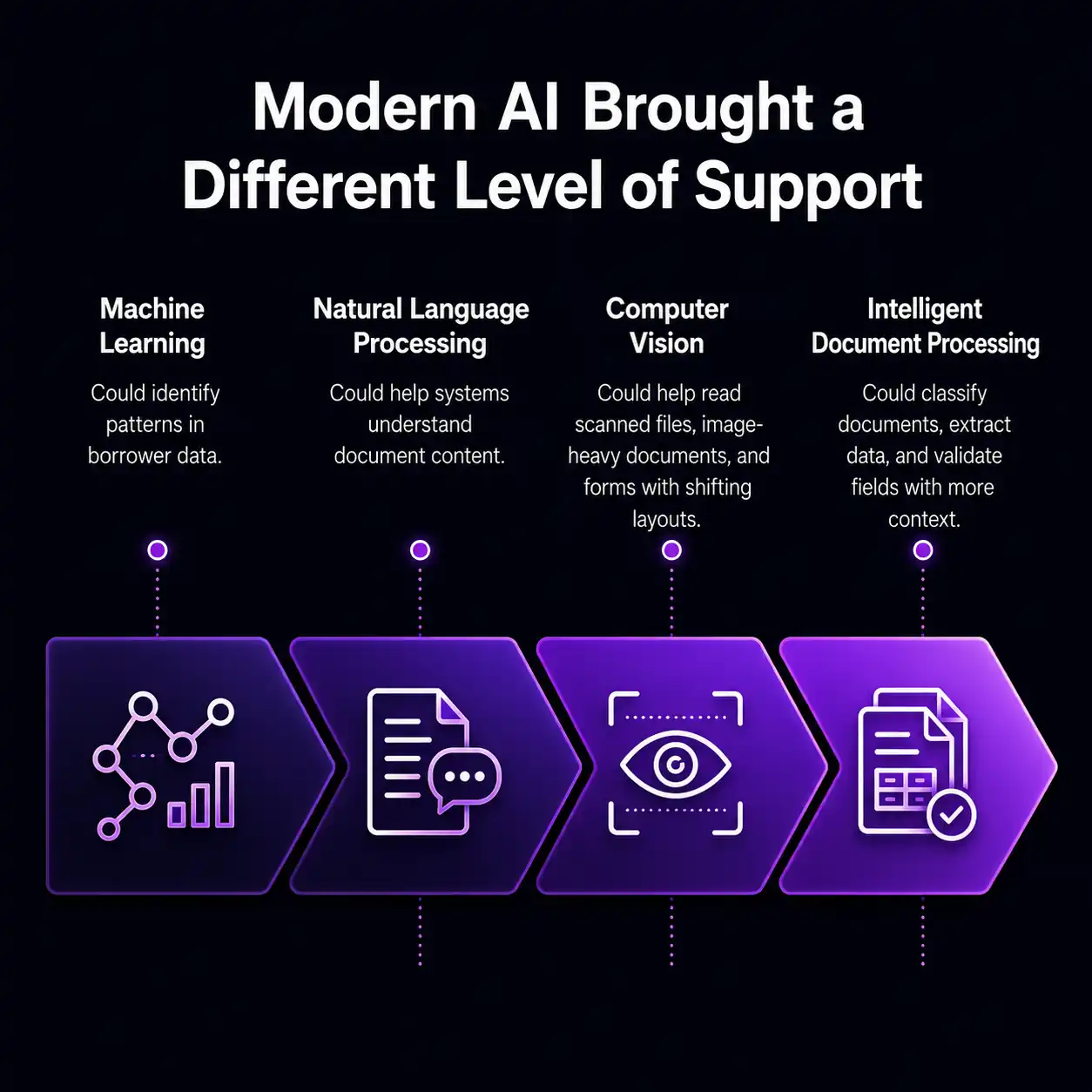

Modern AI brought a different level of support.

- Machine learning could identify patterns in borrower data.

- Natural language processing could help systems understand document content.

- Computer vision could help read scanned files, image-heavy documents, and forms with shifting layouts.

- Intelligent document processing could classify documents, extract data, and validate fields with more context.

This changed how teams viewed automation.

Instead of asking, “Can the system read this page?” lenders started asking, “Can the system understand what this document is, what data matters, and whether something is wrong?”

That is a much bigger shift.

AI can now help mortgage teams identify missing documents, compare borrower names across the file, detect income differences, find missing signatures, validate key data points, and flag cases that need human review.

It also supports a more practical division of labor where AI handles the repetitive scan-and-check work, and humans handle judgment, borrower conversations, exceptions, and final decisions.

What More Can Be Expected With AI in the Mortgage Industry?

The next stage of AI in mortgage will focus less on single tasks and more on connected workflows.

Today, many AI tools help with document classification, data extraction, fraud signals, underwriting support, and borrower communication. The next step is AI that can connect these pieces into a larger workflow.

For example, an AI system may review a loan file, identify missing data, compare extracted fields, raise policy exceptions, draft an audit summary, and route the case to the right person. It may also explain why it flagged an issue and shows the source document behind the flag.

This is where agentic AI becomes important.

Agentic AI refers to systems that can plan steps, use tools, take action, and adapt within defined boundaries. In mortgage, that could mean AI that does more than read a document. It could prepare a file for review, check it against rules, summarize the exceptions, and help the human reviewer move faster.

The future will not be “AI approves every loan alone.”

The future will be AI-supported mortgage operations where every team member has better information earlier.

Common Misconceptions With AI in the Mortgage Industry

AI creates excitement, but it also creates confusion.

Some people hear “AI in mortgage” and imagine a black-box system making loan decisions without people. Others think AI is only a better OCR tool. Some worry that AI increases fraud risk or weakens audits.

These concerns are valid, but many come from a narrow view of how AI works in mortgage.

AI can be risky when it is poorly built, poorly monitored, or used without clear controls. But when it is designed for mortgage workflows, it can add structure, traceability, and speed. The key is to separate myth from practical use.

Will AI Take Jobs of Lenders, Brokers, Mortgage Advisors, and Underwriters?

No, AI will indeed change mortgage roles, but it is not likely to remove the need for people.

Mortgage is a decision-heavy and relationship-heavy business. Borrowers often need advice, especially in cases involving self-employment, complex income, first-time buying, refinancing, credit issues, or changing financial conditions.

AI can support the work behind the scenes.

It can prepare files, identify missing items, summarize borrower data, compare documents, and flag exceptions. That reduces manual pressure on lenders, brokers, advisors, and underwriters.

But it does not replace the human role of explaining options, applying judgment, managing borrower trust, and making accountable decisions.

The better question is not, “Will AI take mortgage jobs?”

The better question is, “Which parts of the loan processing job should people stop doing manually?”

No underwriter wants to spend hours hunting for a number buried across multiple documents. No broker wants to chase basic status updates all day. No lender wants delays caused by missing or mismatched information that could have been flagged earlier. AI can remove that friction.

Is AI Making the Final Decision Regarding a Loan Application?

No, in responsible mortgage operations, AI should support decisions, not act as the sole decision-maker.

This matters because mortgage lending is regulated. Lenders must be able to explain decisions, manage risk, and follow fair lending rules. AI cannot be treated as a mystery box that says yes or no without clear reasoning.

The CFPB has stated that lenders using AI or other advanced models must still provide specific and accurate reasons when taking adverse action against consumers.

That means lenders cannot hide behind a model. If a borrower is denied, the lender must be able to explain why. If AI supports the process, its role must be traceable and governed.

In practice, AI is often used to collect signals, check data, and flag risk. Humans still review the output, apply policy, and make the final call. This model gives lenders speed without removing accountability.

Does AI Bring More Vulnerability Since Fraud Detection and Audit Can Be Misleading or Absent?

No, AI can create risk if it is used without oversight. But AI can also improve fraud detection and audit readiness when it is built with controls.

Mortgage fraud often hides in small differences.

A name may appear differently across documents. Income may not match the stated amount. Bank statement patterns may raise questions. A document may look valid at first glance but include signs of tampering. A file may be complete on paper but still fail a deeper check.

AI can scan across documents faster than a person can. It can flag mismatches, missing fields, unusual patterns, and data points that need review.

That does not mean AI should be trusted blindly.

A strong mortgage AI workflow should include confidence scores, source-level traceability, audit logs, validation rules, and human review for exceptions. Human-in-the-loop review matters because some cases need context that a model may not fully capture.

The goal is not to remove the auditor. The goal is to give the auditor a cleaner file, clearer flags, and better evidence.

Can AI Be Used Only for Data Extraction and Not Validation?

No. Data extraction is only one part of AI’s role in mortgage. AI can read data from documents, but it can also compare, validate, classify, summarize, route, and flag. This is where modern mortgage AI becomes more useful than basic OCR.

For example, AI can extract income from a paystub. But validation asks a deeper question: does that income align with other documents in the file? AI can extract dates. But validation checks whether those dates make sense in the loan timeline.

This matters because mortgage errors often happen between documents, not inside one document. AI becomes more valuable when it connects data points across the file and tells the reviewer where attention is needed.

How AI Actually Works in the Real World?

In real mortgage workflows, AI works best as a support layer across the loan lifecycle.

It is not magic. It is structured automation with learning, pattern detection, and review controls.

AI works better when trained on real mortgage documents because, through the feedback loop, the model learns and executes in future runs. Mortgage files are not clean lab samples. They include poor scans, multi-page PDFs, handwritten notes, inconsistent layouts, duplicate documents, and missing pages.

A system that works well in a demo may still struggle in production if it has not seen enough real-world variation.

That is why lenders should judge AI by production outcomes, not sales slides.

Can it handle real loan files? Can it flag exceptions clearly? Can it show where the data came from? Can it improve over time? Can it fit into existing LOS, QC, audit, and servicing workflows?

Those are the questions that matter.

- AI Is Optimizing Work for Lenders, Brokers, and Underwriters

AI improves mortgage work by removing low-value manual effort.

For lenders, AI can reduce delays caused by document backlogs, missing data, and manual checks. It can help teams process more files without pushing people into longer hours.

For brokers, AI can improve speed and transparency. A broker can spend less time chasing basic updates and more time advising the borrower. That makes the borrower journey smoother.

For underwriters, AI can make files easier to review. Instead of starting from a raw document stack, the underwriter can start with organized data, key flags, and supporting evidence.

This does not make the work less important. It makes the work more focused and also supports consistency.

- AI Is Helping Humans Take a Call Regarding Loans Faster

Speed matters in mortgage, but speed without control is dangerous. AI helps by bringing the right information to the human reviewer faster.

Instead of reviewing every page with equal attention, a mortgage professional can focus on the parts of the file that need action. AI can highlight missing documents, mismatched data, unclear income, expired documents, policy exceptions, or possible fraud signals.

This helps humans make faster calls. It also helps borrowers.

Borrowers do not want vague delays. They want to know what is missing, what needs review, and what comes next. AI can support better communication by giving teams cleaner information sooner.

This is especially valuable in underwriting, QC, and audit workflows.

A reviewer can see what the system found, what it could not confirm, and what needs a human decision. That is more useful than a pile of documents and a checklist.

The best AI systems do not hide their work. They show confidence levels, source documents, extracted fields, and exception reasons.

That makes the review process faster and easier to defend.

- AI Now Has Strong Flagging Mechanisms and Human-in-the-Loop Review

A good AI system does not treat every output as final. It should know when to pause.

That is where flagging and human-in-the-loop review matter.

If the system reads a field with high confidence, it can move the file forward. If the field is unclear, missing, mismatched, or suspicious, it should send that item to a person. This approach protects quality.

It also helps mortgage teams avoid the false choice between manual work and full automation. The best model is often selective automation. AI handles what it can prove. Humans review what needs judgment.

The U.S. Treasury has also noted that fair lending laws apply regardless of the technology used to make a credit decision, and institutions remain responsible for legal compliance when using AI.

That point is important.

AI does not remove responsibility. It increases the need for clear governance, model monitoring, documentation, and review paths. In a mortgage loan application process, trust comes from evidence.

- AI Can Do More Than Just Data Extraction

Data extraction is where many mortgage teams start. But it should not be where they stop.

AI can support the full document-to-decision journey.

It classifies loan documents, extracts borrower and loan data, compares information across files, detects missing pages, validates numbers, identifies exceptions, summarizes issues, and prepares audit-ready outputs, reducing manual effort while improving accuracy and compliance.

This is where mortgage AI begins to deliver real value. The value is not just faster reading. The value is fewer blind spots.

A lender does not need another tool that creates more data for people to clean. A lender needs a system that turns messy files into clear action.

AI can help answer practical questions:

- Is the document present?

- Is the data readable?

- Does the field match across the file?

- Is there a missing signature?

- Is the borrower's information consistent?

- Is there an exception that needs review?

- Is the file ready for the next step?

These are the questions mortgage teams face every day. AI delivers when it helps answer them faster, with proof.

Conclusion

AI is delivering in mortgage, but its biggest value is practical, not flashy.

It is not replacing lenders, brokers, underwriters, advisors, processors, or auditors. It is helping them work with better speed and control. It reads documents, organizes files, extracts data, validates information, flags issues, and prepares teams to make faster decisions.

The mortgage industry does not need AI that acts like a black box. It needs AI that shows its work.

That means clear source links, confidence scores, exception flags, audit trails, human review paths, and governance. It also means using AI in the right places: document-heavy, rules-heavy, and review-heavy workflows where manual effort slows the business down.

AI will not remove the human side of mortgage. Borrowers still need advice. Lenders still need accountability. Underwriters still need judgment. Auditors still need evidence. But AI can remove the repetitive work that keeps mortgage teams stuck in slow cycles.

That is where AI is already delivering in the mortgage industry. And for lenders that use it well, the result is simple: faster files, cleaner reviews, better decisions, and more time for the work that truly needs people.