Every personal insurance application begins with two basic questions: who the applicant is and what coverage they need. To answer these questions consistently across agents, carriers, and markets, the industry relies on a standardized format. In personal lines insurance, that standard begins with ACORD 88.

For agents, underwriters, and operations teams, it is important to understand what ACORD 88 captures, how it fits into the overall submission process, and how it can be handled efficiently. A clear understanding of this form helps teams process applications faster and reduce unnecessary delays.

What Is ACORD 88?

ACORD 88 is the Applicant Information section of the personal lines application, used as the foundational layer across personal insurance submissions. Developed by the Association for Cooperative Operations Research and Development (ACORD), it is typically paired with companion forms such as ACORD 89 (Residential) or ACORD 90 (Personal Auto) to build a complete submission package.

The form captures the core underwriting data that every personal lines policy depends on: applicant details, prior coverage history, and loss history. Think of ACORD 88 as the starting point: it establishes who the insured is before additional forms define the specific risks being covered.

One of its key practical advantages is reusability. Because ACORD 88 captures applicant-level data rather than coverage-specific details, the same completed section can be used across multiple personal lines policies within a single submission, keeping applicant information consistent across all coverages without redundant data entry.

How ACORD 88 Relates to Other ACORD Forms

ACORD 88 is the anchor of the personal lines submission. It does not stand alone; it establishes the applicant context that companion forms build upon.

When an agent prepares a personal lines submission, whether for home, auto, or a combined package, ACORD 88 is completed first. The specific coverage forms follow. Missing or inconsistent ACORD 88 data creates downstream errors across every companion form in the package.

Why ACORD 88 Matters for Personal Lines Teams

Personal lines is a high-volume business. Agents submit hundreds of applications per week, and carriers need to move them through intake, underwriting, and policy issuance quickly and accurately.

ACORD 88 matters because it creates the consistent applicant record that everything else depends on. Without a complete and accurate foundational form, underwriters cannot reliably evaluate prior coverage gaps, assess loss history patterns, or confirm applicant eligibility for the coverage being requested.

It also matters for regulatory and compliance reasons. Personal lines carriers operate across multiple states, each with its own filing and documentation requirements. ACORD 88's standardized format satisfies documentation obligations consistently, regardless of the state or market.

According to industry research, data entry errors in personal lines applications contribute to significant rework and processing delays, problems that trace back, in many cases, to incomplete or inconsistent applicant information at the ACORD 88 stage.

Who Uses ACORD 88?

ACORD 88 moves through several hands between initial completion and policy issuance.

- Independent agents and brokers who gather applicant information and prepare personal lines submissions on behalf of their clients

- Captive agents working within a single carrier's system who use ACORD 88 as the standard intake form for new personal lines business

- Personal lines underwriters who rely on applicant data and loss history to assess eligibility and set terms

- Insurance operations and intake teams are responsible for receiving, digitizing, and validating incoming application packages before routing to underwriting

- Agency management system users whose platforms generate ACORD 88-compliant outputs as part of the standard application workflow

In practice, ACORD 88 is often completed by the agent but reviewed and validated by multiple parties, making data accuracy at the point of completion critical for every step that follows.

How to Complete ACORD 88: Section-by-Section Breakdown

ACORD 88 is organized into clearly defined sections. Each captures a distinct layer of applicant information. Here is what each section contains and why it matters.

Section 1: Applicant Information

This section captures the named insured's full legal name, date of birth, contact information, and mailing address. It also records the applicant's Social Security Number or Tax ID where required for underwriting or regulatory purposes.

Accuracy here is non-negotiable. The named insured on ACORD 88 must match exactly across all companion forms in the submission. Discrepancies between ACORD 88 and ACORD 89 or ACORD 90 are among the most common causes of submission rejections at intake.

Section 2: Policy Information and Coverage Requested

This section identifies the policy effective date, the term requested, and the carrier or market being approached. It also notes whether the application is for a new policy, a renewal, or a rewrite.

Carriers use this section to route the application correctly and to flag coverage continuity issues, particularly where a lapse in prior coverage may affect eligibility or pricing.

Section 3: Prior Insurance Information

Here, the applicant discloses their existing or most recent prior coverage, including the name of the prior carrier, policy number, coverage type, and expiration date.

Prior coverage history is a significant underwriting data point in personal lines. Continuous coverage with no lapses typically supports more favorable terms. Gaps or cancellations, particularly for non-payment, are flagged during underwriting review and may affect the offer made.

Section 4: Loss History

The loss history section requires disclosure of any claims filed within a defined lookback period, typically three to five years. Each entry should include the date of loss, a brief description of the incident, the coverage type under which the claim was filed, and the total amount paid.

Loss history is one of the primary drivers of personal lines underwriting decisions. A clean loss record supports standard market placement; a history of frequent or high-severity claims may require surplus lines placement or result in coverage restrictions.

Section 5: Applicant Signature and Authorization

The completed form must be signed by the applicant, confirming that the information provided is accurate and authorizing the carrier to use it for underwriting and policy issuance purposes.

Electronic signatures are accepted by most carriers where permitted under state law. Agents should verify carrier-specific requirements before submitting, particularly for states with stricter wet signature requirements on personal lines applications.

Common Challenges When Processing ACORD 88

Despite its standardized format, ACORD 88 creates real operational friction in personal lines workflows. The challenges that surface most often are consistent across carriers and markets.

Incomplete Prior Insurance Details

Agents frequently submit ACORD 88 with incomplete prior carrier information: missing policy numbers, incorrect expiration dates, or blanks where coverage type should be specified. This forces underwriters to follow up before the application can be evaluated, adding unnecessary days to the process.

Inconsistent Loss History Entries

Loss history is often the weakest section of a personal lines submission. Claim amounts, dates, and coverage types are frequently estimated or left vague. When the disclosed history does not align with loss runs pulled by the carrier, reconciliation is required, which delays binding.

Named Insured Mismatches Across Forms

The applicant's name on ACORD 88 does not always match the named insured on companion forms. Nicknames, maiden names, and middle name variations are common culprits. These mismatches create data integrity issues that require manual correction downstream.

Handwritten and Non-Standard Submissions

Many personal lines applications still arrive as scanned, handwritten forms or proprietary agency system exports that do not map cleanly to ACORD 88's field structure. Manual re-entry from these formats introduces errors and slows intake processing significantly.

Missing Signatures

Unsigned or improperly signed ACORD 88 forms cannot be processed. This is a surprisingly common issue, particularly in high-volume submission environments where agents are working through application packages quickly.

Why Manual Processing of ACORD 88 Slows Teams Down

Personal lines carriers handle enormous submission volumes. A standard intake workflow requires an analyst to receive the ACORD 88, review it for completeness, re-key the data into the policy administration system, and flag any issues for follow-up. For a single application, this can take several minutes. At scale, that time accumulates fast.

Manual processing is also error-prone. In personal lines, where thin margins make rework expensive, errors in applicant name, prior coverage details, or loss history can affect pricing accuracy, eligibility decisions, and ultimately, the carrier's loss ratio.

The challenge compounds as submission volumes grow. Personal lines carriers cannot simply add staff to keep pace; the economics do not support it, and the labor market for insurance operations roles remains tight. A different approach to intake processing is needed.

ACORD 88 Automation Using Intelligent Document Processing

Intelligent Document Processing (IDP) is the technology applied to ACORD form intake automation. IDP combines optical character recognition (OCR), machine learning, and AI-driven field extraction to convert incoming ACORD 88 documents, regardless of format, into structured, validated data.

Here is how automation applies specifically to ACORD 88 in a personal lines workflow.

Step 1: Document Ingestion and Classification

IDP systems receive incoming submissions through email, carrier portals, or API-connected agency management platforms. The system automatically identifies and classifies the ACORD 88 within a multi-form submission package, separating it from ACORD 89, ACORD 90, or other companion forms submitted together.

Step 2: Field Extraction Across All Sections

Trained extraction models capture data from every section of the form: applicant name, date of birth, contact details, prior coverage information, and loss history entries. Models trained on ACORD 88's specific field layout handle typed forms, handwritten applications, and non-standard agency system outputs with consistent accuracy.

Step 3: Validation Against Carrier Business Rules

Extracted data is validated in real time against configurable carrier rules. Missing signature fields, incomplete loss history entries, prior coverage gaps outside acceptable parameters, and named insured mismatches against companion forms are all flagged before the application reaches the underwriting queue.

Step 4: Cross-Form Data Consistency Checks

Because ACORD 88 feeds into the broader personal lines submission package, IDP systems cross-reference extracted data against companion forms: ACORD 89, ACORD 90, and others, automatically flagging discrepancies in named insured name, coverage period, or coverage type across forms.

Step 5: Exception Routing for Human Review

Applications with flagged issues are routed to the appropriate intake analyst with the extracted data pre-populated and the specific exceptions clearly highlighted. Analysts resolve issues in a fraction of the time it takes to process the form manually from scratch.

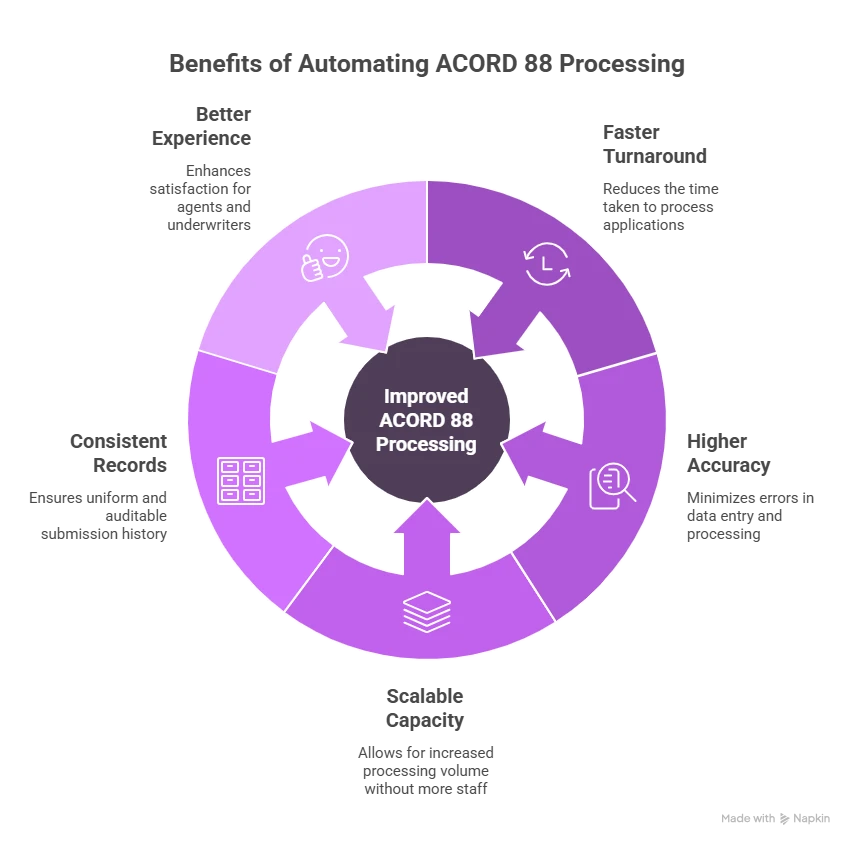

Advantages of Automating ACORD 88 Processing

Automating ACORD 88 intake produces measurable gains across the personal lines workflow.

Faster Application Turnaround

Automated processing reduces ACORD 88 intake time from minutes to seconds. Applications that once waited days in intake queues can move to underwriter review the same day they arrive.

Higher Data Accuracy

AI-driven extraction with built-in validation consistently outperforms manual data entry in terms of accuracy. Errors in prior coverage details and loss history, the sections most prone to manual error, are caught at intake rather than discovered during underwriting review.

Scalable Capacity Without Additional Headcount

Automated systems absorb volume spikes, new business campaigns, renewal seasons, and catastrophe-driven submission surges without requiring additional staff. Teams previously stretched thin during peak periods can redirect capacity toward higher-value work.

Consistent, Auditable Submission Records

Every extracted field is logged with its source, extraction confidence score, and validation status. This creates an auditable record that supports carrier compliance requirements and state regulatory documentation obligations.

Better Agent and Underwriter Experience

When submissions arrive pre-validated and cleanly structured, agents spend less time on follow-up calls, and underwriters spend less time chasing missing data. The entire workflow runs more smoothly for every stakeholder in the chain.

How Infrrd Automates ACORD 88 Processing

Infrrd is an intelligent document processing platform built for the insurance industry, with purpose-trained capabilities for ACORD personal lines form processing, including ACORD 88.

Pre-Trained Extraction Models for ACORD 88

Infrrd's extraction models are trained specifically on ACORD 88's field structure, covering applicant information, prior coverage details, and loss history sections. The models accurately extract data from typed forms, handwritten applications, and non-standard agency management system outputs, handling the format variability that defeats generic OCR tools.

Cross-Form Consistency Validation

Because ACORD 88 feeds into the broader personal lines submission package, Infrrd validates extracted data against companion forms: ACORD 89, ACORD 90, and others, automatically flagging named insured mismatches, coverage period inconsistencies, and other cross-form discrepancies before the submission reaches underwriting.

Configurable Carrier Rule Integration

Infrrd's validation layer is configurable to each carrier's specific underwriting rules. Prior coverage gap thresholds, loss history lookback periods, and required field completeness checks are all adjustable, ensuring that the validation applied at intake matches the carrier's actual requirements, not a generic standard.

Direct Integration with Policy Administration Systems

Validated ACORD 88 data flows directly into the carrier's policy administration system or submission management platform via API. No manual re-keying. No format translation. Intake teams stop functioning as data entry operations and start functioning as quality control checkpoints.

Summary

ACORD 88 is the foundation of every personal lines submission. It establishes who the insured is, documents their prior coverage history, and captures the loss history that underwriters depend on to evaluate risk and set terms. Getting it right at the point of submission shapes everything that follows.

Manual processing of ACORD 88 remains a bottleneck for most personal lines teams; slow, error-prone, and difficult to scale. Intelligent document processing closes that gap, turning ACORD 88 intake from a manual data entry task into a fast, accurate, automated step that accelerates the full application workflow.

FAQs About ACORD 88

What is ACORD 88 used for?

ACORD 88 is the standard personal insurance application form used to capture applicant information for personal lines coverage. It records the applicant's details, prior coverage history, and loss history, forming the foundational section of a personal lines submission.

What is the difference between ACORD 88 and ACORD 89?

ACORD 88 captures the applicant-level information that applies across all personal lines coverages, identity, prior insurance, and loss history. ACORD 89 is the residential supplement that adds property-specific risk data for homeowners or dwelling coverage. The two forms are typically submitted together for residential applications.

Is ACORD 88 used for auto insurance applications?

ACORD 88 provides the applicant foundation for personal auto submissions as well. It is used alongside ACORD 90 (Personal Auto Application), which captures vehicle details, driver information, and auto-specific underwriting data.

What loss history does ACORD 88 require?

Most carriers require three to five years of loss history on ACORD 88. Each entry should include the date of loss, a description of the incident, the coverage type under which the claim was filed, and the total amount paid.

What happens if ACORD 88 is incomplete?

An incomplete ACORD 88 typically causes the application to be returned to the agent or placed in a pending queue while missing information is gathered. Common gaps include incomplete prior insurance details, missing loss history entries, and unsigned authorization sections, all of which delay processing and policy issuance.

Can ACORD 88 be submitted electronically?

Yes. ACORD 88 can be submitted as a digital PDF through carrier portals, email, or agency management system integrations. Most carriers accept electronic signatures where permitted under state law, though requirements vary by state and carrier.

Why does prior coverage history matter on ACORD 88?

Prior coverage history is a key underwriting factor in personal lines. Continuous coverage with no lapses typically supports standard market placement and favorable terms. Coverage gaps or cancellations for non-payment are considered elevated risk indicators and may affect the carrier's offer or require non-standard market placement.

How does IDP improve ACORD 88 processing for carriers?

Intelligent document processing automates the extraction and validation of ACORD 88 data at intake, eliminating manual re-keying, catching errors and missing fields before the application reaches underwriting, and pushing clean, structured data directly into policy administration systems. Processing time drops significantly.

What is the named insured mismatch problem in ACORD 88 submissions?

Named insured mismatches occur when the applicant's name on ACORD 88 differs from the named insured recorded on companion forms like ACORD 89 or ACORD 90, often due to nicknames, maiden names, or middle name variations. These mismatches create data integrity issues requiring manual correction and can delay policy issuance if caught late in the workflow.