The ACORD 27 (Evidence of Property Insurance) is a standardized document used to verify that a property has active insurance coverage and to provide key details of that coverage, such as policy limits, insurer information, and effective dates.

Even though the ACORD 27 is widely used across commercial real estate and lending, it often creates confusion. It’s frequently mixed up with similar forms like the ACORD 25 or ACORD 28, and many teams still rely on manual data processing, which slows things down and increases the risk of errors and compliance issues.

In this guide, we’ll break down what the ACORD 27 is, walk through its key sections, explain how it fits within the broader ACORD ecosystem, and explore how intelligent document processing (IDP) and automation can simplify and scale high-volume form handling.

What Is the ACORD 27?

The ACORD 27 is the standardized Evidence of Property Insurance form developed by ACORD (Association for Cooperative Operations Research and Development). It provides written evidence that a named insured holds an active commercial property insurance policy, documenting coverage type, limits, and policy terms for the benefit of a designated interested party, typically a lender or mortgagee.

Think of ACORD 27 as the property insurance equivalent of a bank statement lenders need standardized, verified evidence their systems can process and IDP platform for high-volume insurance evidence form processing is what makes that processing fast, accurate, and scalable. The ACORD 27 is that document.

One distinction matters here: the ACORD 27 is an evidence form, not a certificate. That is not just a semantic difference; it carries meaningful legal weight, as discussed below.

ACORD 27 and Other Related Forms

The ACORD 27 lives within a family of property insurance documents. Knowing which form applies when prevents costly misrouting and compliance failures.

The Critical Distinction

ACORD 27 and 28 are evidence forms, intended specifically for lenders and mortgagees who have a financial interest in the insured property.

ACORD 24 is a certificate form, used when the requester holds no financial interest, such as a landlord confirming a tenant's property coverage. Issuing the wrong form for the wrong audience is a common operational error with real downstream consequences.

Why the ACORD 27 Matters to Insurance and Lending Teams?

Commercial property insurance touches nearly every corner of real estate finance, corporate real estate operations, and risk management. The ACORD 27 sits at the intersection of all of them.

Loan Origination and Servicing

Mortgage lenders and commercial real estate lenders require evidence of property insurance as a condition of funding. An inaccurate or missing ACORD 27 can delay a closing or trigger a loan compliance flag. For large portfolios, this compounds fast.

Escrow and Title Requirements

Title companies and escrow agents routinely request ACORD 27 forms to confirm that property coverage is in place before disbursement. Delays in issuance translate directly to closing delays.

Portfolio Risk Management

Institutional property owners managing dozens or hundreds of properties rely on ACORD 27 evidence to track insurance compliance and ACORD 26 automation for insurance policy certification logs is what keeps the master record of every certificate issued across that same portfolio accurate and audit-ready. A lapse in coverage anywhere in the portfolio is a liability exposure for the whole organization.

Regulatory Compliance

In regulated lending environments, particularly federally backed mortgages, failure to maintain documented evidence of property insurance is a compliance violation, not just an oversight.

According to research by McKinsey & Company, the commercial insurance industry still relies heavily on manual document processing. This dependence slows operations and causes processing times to lag behind other financial services sectors by several years. For time-sensitive activities like loan closings, these delays translate directly into financial impact.

The same research shows that underwriters spend 30 to 40 percent of their time on administrative tasks. This includes re-entering data, reviewing documents manually, and performing routine analyses. As a result, less time is available for higher-value work such as risk assessment and decision-making, which further affects efficiency and turnaround times.

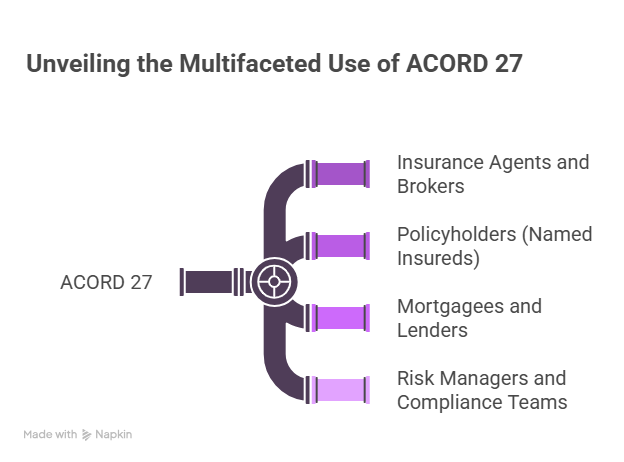

Who Uses the ACORD 27?

The ACORD 27 touches multiple parties across every property transaction. Understanding each party's role clarifies why accuracy and speed both matter.

Insurance agents and brokers issue the ACORD 27 on behalf of their policyholders whenever a lender or financial institution requests evidence of coverage. This is a recurring, high-volume task, especially for agents serving commercial real estate clients with active lending relationships.

Policyholders (named insureds) provide the form to lenders, escrow agents, and other interested parties as evidence that their property is insured. Delays in obtaining the form from their agent can put transactions at risk.

Mortgagees and lenders receive and review the ACORD 27 to confirm that their collateral, the insured property, carries adequate coverage and that they are properly noted as an interested party. They are the primary audience the form is designed to serve.

Risk managers and compliance teams use ACORD 27 documentation to track insurance requirements across large real estate portfolios, ensuring every property meets lender and regulatory standards at all times.

How to Complete the ACORD 27: A Section-by-Section Breakdown

The ACORD 27 is organized into clearly defined sections. Each field serves a specific compliance or verification function. Errors or omissions in any section can result in rejection or require reissuance, neither of which is acceptable when a closing is on the line.

Section 1: Agency / Producer Information

This block identifies the insurance agency or brokerage issuing the evidence. It includes the producer's name, mailing address, contact number, and email. This section establishes accountability; if the lender needs to verify coverage or request changes, they know exactly who to contact.

Section 2: Named Insured Information

The named insured's legal name and address must appear exactly as they appear on the underlying policy. Any mismatch, even a missing "LLC" or a misspelled street name, can trigger a compliance rejection from the lender's insurance review team. Precision here is non-negotiable.

Section 3: Insurer Information

The full legal name of the insurance carrier and its NAIC code are required. The NAIC code allows the lender to independently verify the carrier's licensing status and A.M. Best financial rating, which many lenders require to meet a minimum threshold. Carriers that do not meet the lender's rating requirements will trigger a coverage flag regardless of the policy limits.

Section 4: Policy Information

This section documents the core policy terms: policy number, effective date, expiration date, and coverage type. Coverage types typically include:

- Special Form (All Risk): Covers all perils not explicitly excluded, the broadest and most commonly required coverage type for commercial mortgages.

- Basic Form: Covers only specifically named perils, generally insufficient for most lenders.

- Broad Form: A middle ground between Basic and Special.

The coverage form type matters to lenders. Most commercial mortgage agreements require Special Form coverage. Issuing evidence for a Basic Form policy against a Special Form requirement is a document error that will stall funding.

Section 5: Coverage and Limits

This is the most scrutinized section by lenders and compliance teams. It documents:

- Building limit: Represents the total replacement cost value (RCV) of the physical structure, which lenders verify against the outstanding loan balance to ensure full collateral protection.

- Business personal property limit: Specifies the maximum coverage amount for tangible assets and contents located within the insured premises, applicable when the loan includes non-real estate collateral.

- Blanket or scheduled coverage: Identifies if insurance limits are aggregated across multiple properties (blanket) or individually allocated to specific locations (scheduled), determining how loss payouts are distributed.

- Coinsurance percentage: Defines the mandatory threshold of insurance (relative to total value) that the policyholder must maintain to avoid financial penalties during a partial loss claim.

- Deductible: Indicates the specific out-of-pocket cost the insured must pay per occurrence before the carrier begins indemnification, used by lenders to assess the borrower's immediate liquidity risk.

Lenders compare the building limit directly against the outstanding loan balance or required replacement cost value. If the limit is insufficient, the lender will require coverage to be increased before funding.

Section 6: Mortgagee / Additional Interest Information

This section identifies the lender or interested party receiving the evidence. Their legal name, loan or account number, and mailing address must be listed precisely. The mortgagee clause, the specific language protecting the lender's interest in the event of a claim, is applied here.

The mortgagee clause is not optional. It is the mechanism that protects the lender's collateral. Missing or incorrectly worded mortgagee language is one of the most frequently cited errors in property insurance evidence issuance.

Section 7: Description of Premises

This section identifies the specific property being insured: address, building description, and any location identifiers used in the policy. For blanket policies covering multiple locations, this section must clearly identify which property or properties the evidence applies to.

Section 8: Special Conditions or Other Coverage

A free-text field for noting special endorsements, additional coverages, or conditions relevant to the lender's requirements. Flood, earthquake, and windstorm coverage, if carried, are often noted here, as these are commonly required by lenders in high-risk zones and are not included in standard commercial property policies.

Section 9: Authorized Signature

The evidence must be signed by an authorized representative of the issuing agency. An unsigned ACORD 27 is not valid evidence of coverage.

Common Challenges Teams Face With ACORD 27 Processing

The form is standardized. The problems teams run into are not.

Mortgagee clause errors

The lender's legal name and loan number must be exact. Financial institutions frequently update their legal entity names following mergers and acquisitions. Agents working from outdated contact records issue evidence with incorrect mortgagee language, a compliance failure that requires reissuance and delays the transaction.

Coverage form mismatches

When the underlying policy carries Basic or Broad Form coverage but the lender requires Special Form, the discrepancy does not surface until the evidence is reviewed. Catching this at issuance, rather than at the lender's desk, requires careful policy-to-form verification.

Building limit adequacy

Replacement cost values shift with construction costs. An insured who has not updated their coverage limits in two or three years may be significantly underinsured relative to the lender's requirement. Issuing evidence for an inadequate limit causes a compliance flag and requires coverage updates before evidence can be reissued.

Flood and special hazard coverage

Properties in FEMA-designated flood zones require separate flood insurance. Many agents issue the ACORD 27 for the base property policy without noting whether flood coverage is in place, leaving the lender's compliance team to chase that documentation separately.

Volume and turnaround pressure

Commercial real estate transactions move fast. Lenders frequently request evidence with same-day or next-day turnaround. For agents managing large portfolios, the combination of volume and urgency creates the conditions for errors that would not occur under normal processing time.

Industry data from Quality Magazine indicates that the typical error rate for manual data entry is approximately 1%. While this figure of error rate appears marginal, the impact scales significantly in high-volume environments where teams process thousands of documents weekly. The issuance of the ACORD 27 fits this high-risk profile precisely, as time-pressured workflows often amplify the consequences of these manual entry errors.

Automating ACORD 27 Processing With IDP

Intelligent Document Processing (IDP) leverages AI, machine learning, and Optical Character Recognition (OCR) to automate data workflows for insurance documents. The technology extracts, validates, and routes data from both inbound evidence requests and the source policy documents used to populate those requests.

Here is how IDP transforms the ACORD 27 workflow:

Step 1: Classify and Route the Incoming Request

When a lender's evidence request arrives via email, portal upload, or electronic request, the IDP system classifies it automatically. It identifies it as an ACORD 27 request, extracts the lender's stated requirements (coverage type, limits, mortgagee information), and routes it to the appropriate workflow without manual triage.

Step 2: Extract Policy Data From Source Documents

The IDP engine reads the underlying policy documents: declarations pages, endorsements, and schedules. Extracts the relevant data: coverage form, building limits, deductibles, coinsurance, and effective dates. Structured and semi-structured policy formats are handled without manual re-keying.

Step 3: Validate Coverage Against Lender Requirements

Extracted policy data is compared against the lender's stated requirements. If the coverage form is Basic but the lender requires Special Form, the system flags the mismatch before the evidence is issued, not after it is rejected. If the building limit falls short of the required minimum, an alert goes to the agent for resolution.

Step 4: Populate Mortgagee and Interested Party Fields

The system cross-references the lender's legal entity name from a maintained database of mortgagee clause language. Accurate, current mortgagee clause text is auto-filled without requiring the agent to look it up manually. This single step eliminates one of the most frequent and consequential ACORD 27 errors.

Step 5: Issue and Deliver

Once validated, the completed ACORD 27 is generated and delivered to the requesting party through their preferred channel. End-to-end processing time drops from hours to minutes. The entire workflow is logged, creating a complete audit trail for compliance purposes.

Advantages of Automating ACORD 27 Processing

Beyond efficiency, automation shifts the nature of agent work. Instead of spending the majority of their time on evidence issuance, agents focus on coverage analysis, renewal management, and client relationships; work that requires judgment that no system can replace.

How Infrrd Automates ACORD 27 Processing?

Infrrd’s Intelligent Document Processing (IDP) automates ACORD 27 (Evidence of Property Insurance) processing by converting policy documents into structured, usable data with minimal manual effort. The platform is pre-trained on ACORD property forms, so teams can process different formats without templates or setup.

Infrrd’s IDP reads source documents such as declarations pages and endorsement schedules, extracts key coverage details, and maps them directly to ACORD 27 fields. This eliminates manual lookup and data entry, reducing delays and errors.

The system also validates extracted data against lender requirements before issuance. Coverage gaps, missing details, or mismatches are flagged early, helping teams avoid rework and back-and-forth with lenders.

Summary

The ACORD 27 is the foundational document for property insurance evidence in commercial lending and real estate. Its standardized structure makes it universally readable across carriers, lenders, and title companies, but that standardization does not make it simple to produce accurately at scale, under closing-day pressure, across a large and constantly changing portfolio.

Teams that continue to rely on manual ACORD 27 processing will find that the bottleneck only grows as loan volumes and portfolio complexity increase. Automation built on purpose-trained IDP models gives lending operations teams the throughput, accuracy, and compliance consistency that manual processing cannot reliably deliver.

FAQs

Q. What is the ACORD 27 form used for?

The ACORD 27 is the Evidence of Property Insurance form. It provides lenders, mortgagees, and other interested parties with standardized written evidence that a named insured holds an active commercial property insurance policy with specified coverage and limits.

Q. What is the difference between ACORD 27 and ACORD 28?

Both are evidence forms for property insurance intended for lenders. The ACORD 28 is the Evidence of Commercial Property Insurance and includes additional fields specific to commercial lending requirements. The ACORD 27 is the more broadly used form and covers both personal and commercial property contexts.

Q. What is the difference between ACORD 27 and ACORD 24?

The ACORD 24 is a certificate form, used when the requester has no financial interest in the property, such as a landlord confirming a tenant's coverage. The ACORD 27 is an evidence form, used specifically for lenders and mortgagees who hold a financial interest in the insured property. Issuing the wrong form can create compliance issues for the requesting party.

Q. Does the ACORD 27 create or modify insurance coverage?

No. The ACORD 27 documents existing coverage; it does not create, extend, alter, or guarantee any insurance policy. All coverage terms are governed entirely by the underlying policy.

Q. What is a mortgagee clause on an ACORD 27?

The mortgagee clause identifies the lender as an additional interested party and protects their financial interest in the insured property. It ensures that in the event of a covered loss, the lender's claim to insurance proceeds is recognized. Incorrect or missing mortgagee language is one of the most common ACORD 27 errors.

Q. What types of coverage are documented in the ACORD 27 form?

The ACORD 27 documents commercial property coverage, including building limits, business personal property limits, coverage form type (Special, Broad, or Basic), coinsurance percentage, and deductible. Special hazard coverage, such as flood or earthquake, can also be noted in the special conditions section.

Q. Can the ACORD 27 be issued electronically?

Yes. Electronic issuance and delivery of the ACORD 27 is standard practice. The form must still carry an authorized representative's signature, which can be electronic in most jurisdictions.

Q. How long is an ACORD 27 valid?

The evidence is valid for the period of the underlying policy. Once the policy expires or is cancelled, the ACORD 27 is no longer valid. Lenders typically require updated evidence at each policy renewal.

Q. What is the most common reason an ACORD 27 gets rejected by a lender?

The most frequent rejection causes are incorrect or outdated mortgagee clause language, insufficient building limits, the wrong coverage form type (Basic instead of Special Form), and missing flood or special hazard coverage documentation for properties in designated risk zones.

Q. What happens if there are multiple properties on one policy?

For blanket policies covering multiple locations, the ACORD 27 must clearly identify the specific property or properties to which the evidence applies, along with the applicable limits for each location. Blanket limit documentation without location-specific breakdowns is often insufficient for commercial lender requirements.