Insurance has always been a slow-moving industry; by design. Managing risk for millions of people requires caution. But the pace of change today is different.

Digital disruption in insurance is not a distant trend. It is actively changing how carriers price policies, how customers file claims, and how companies compete.

The numbers reflect this shift. 74% of insurance executives ranked digital transformation and technology adoption as their top priority in 2025. The global digital insurance platform market is projected to reach USD 148.16 billion by 2025, with strong growth expected through 2030. Early adopters are pulling ahead. The gap between them and slower-moving carriers is growing.

What Digital Disruption in Insurance Really Is?

Digital disruption in insurance refers to the fundamental changes in how insurance products are built, sold, underwritten, and serviced, which is driven by technology. It's not just adding a mobile app or digitizing paper forms. It means rethinking core processes from the ground up using tools like artificial intelligence, machine learning, cloud computing, and real-time data.

Traditional insurance operates on historical data, manual reviews, and batch processing. Disruption replaces those with live data feeds, automated decisions, and customer experiences that feel less like bureaucracy and more like a modern app. The result is faster quotes, better risk assessment, lower costs, and products that actually fit how people live today.

Examples of Digital Disruption in the Insurance Industry

Some of the clearest examples of digital disruption are already mainstream:

- Usage-Based Auto Insurance: Companies like Root and Metromile track driving behavior through telematics and price policies based on actual driving patterns rather than demographic averages.

- AI-Powered Claims Processing: Lemonade uses an AI-powered claims adjuster to process certain insurance claims in under three seconds. The system requires no phone calls and no paperwork.

- Embedded Insurance: Coverage is now sold directly inside the purchase flow. When you buy a laptop or book a flight, insurance is offered at checkout, so no separate policy is needed.

- Predictive Underwriting: Rather than relying solely on credit scores and medical history, insurers now incorporate data from wearable devices, social signals, and IoT inputs to price risk more precisely.

Each of these examples represents a process that used to require human review, now handled faster, cheaper, and often more accurately through technology.

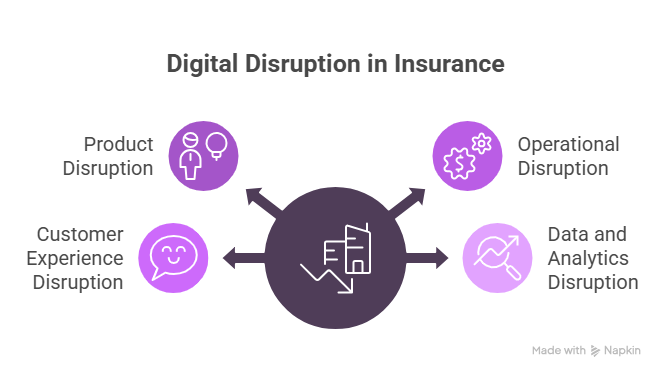

Types of Digital Disruption in Insurance

Digital disruption in insurance doesn't come from a single direction. It shows up across several distinct categories:

- Product Disruption: New insurance products designed around digital lifestyles: cyber insurance for individuals, gig economy coverage, parametric policies that pay out automatically when a defined event occurs.

- Distribution Disruption: Direct-to-consumer platforms and digital brokers that bypass traditional agent networks entirely, giving customers more control and lower acquisition costs for carriers.

- Operational Disruption: Back-office automation through robotic process automation (RPA), AI-based document processing, and cloud-native systems that replace legacy infrastructure.

- Customer Experience Disruption: Conversational AI, self-service portals, and mobile-first claims that meet customers where they are instead of forcing them through outdated contact centers.

- Data and Analytics Disruption: The shift from annual actuarial models to real-time, continuous risk assessment using new data sources.

Challenges of Digital Disruption in Insurance

Digital disruption creates real opportunities. It also creates real friction. Most insurers don't have a clean path from where they are to where they want to be.

Key Challenges Faced by the Insurance Sector

Legacy Infrastructure

Many large carriers still run core systems built in the 1970s and 1980s. Those systems were not designed to connect with modern APIs, process real-time data, or support cloud-based architecture. Replacing them is expensive and risky. Working around them is inefficient and limits progress.

Data Quality And Governance

Digital transformation depends on clean, accessible data. Most insurers store data across dozens of separate systems with inconsistent formats and little standardization. Before AI can produce reliable outputs, the data must be organized. This work is time-consuming and often deprioritized.

Regulatory Compliance

Insurance is one of the most heavily regulated industries in the world. Requirements vary by state and country. AI-based underwriting and claims decisions raise questions about fairness, transparency, and accountability. Regulators are still developing frameworks to address these concerns. Moving quickly is difficult when the rules are not yet settled.

Talent Shortages

Building and maintaining digital insurance platforms requires skills in data science, cloud engineering, and AI. These skills are in short supply globally. They are even harder to find in an industry that has not historically attracted technology talent.

Customer trust remains a real barrier. Many policyholders are skeptical of automated decisions. When an algorithm denies a claim or raises a premium, customers want a clear explanation. That explanation is harder to deliver without a human in the process.

Why Companies Are Slow to Adopt Digital Disruption in Insurance?

Slow adoption is not always irrational. For large, established carriers, moving too fast carries real risks. Those risks can outweigh the short-term benefits.

Legacy Systems

Many carriers have spent hundreds of millions of dollars building and customizing core policy administration systems over decades. Replacing those systems is not a simple decision, even when a modern alternative would perform better. The transition risks alone are substantial. Data migration failures, system outages, and compliance gaps can all result from a poorly managed replacement. For many carriers, caution is the more defensible position.

Prioritization

Most insurers manage several competing demands at once. Regulatory changes, pricing pressures, catastrophic loss events, and workforce challenges all require attention and budget. Digital transformation is important, but it competes directly with immediate operational needs. It often loses that competition in the short term.

Internal Culture

Insurance has historically rewarded stability and risk avoidance. An underwriter with 20 years of experience does not easily defer to an AI recommendation. That shift requires more than policy changes or training sessions. It requires sustained change management over time.

Digital Investments

Many companies cannot build a clear return on investment case. This insurance often takes three to five years to produce measurable results. When failure costs are high and leadership is accountable to short-term financial targets, committing to a long-term transformation program is difficult to justify.

How Insurers Can Successfully Implement Digital Transformation

Companies making the most progress do not try to transform everything at once. They identify high-value starting points and build from there.

Start with Claims: Claims processing is where technology produces the fastest and most measurable results. Automating document extraction, fraud detection, and routine approvals reduces cycle times and lowers costs. Customers notice these improvements directly. That visibility makes claims an effective place to demonstrate the value of digital investment.

Invest in Data Infrastructure Before AI: Many AI initiatives stall because the underlying data is not reliable enough to produce accurate outputs. Organizing, standardizing, and making data accessible is the foundational step. Without it, AI tools cannot perform consistently, regardless of how advanced they are.

Use APIs and Microservices to Modernize Incrementally: Replacing legacy systems all at once is high-risk and expensive. Leading insurers are instead building modern API layers on top of existing infrastructure. This approach allows them to launch new products and connect new data sources without a full system replacement.

Partner Selectively With Insurance-Tech Firms: Not every capability needs to be built in-house. Established carriers can work with specialized companies that have already developed solutions for specific problems, such as telematics, AI underwriting, or digital claims intake. The priority is selecting partners whose technology integrates cleanly with existing systems and can scale over time.

Build For The Customer, Not The Process: Successful digital insurance initiatives start from the customer's point of view. What does filing a claim require? What makes getting a quote difficult? Designing from those experiences outward produces better outcomes than simply digitizing existing internal workflows.

Advantages of Digital Disruption in Insurance

Digital disruption in insurance produces measurable benefits across operations, customer experience, and revenue. These advantages grow stronger as adoption deepens.

Speed: AI-assisted underwriting can process applications in minutes rather than days. Automated claims can pay out in hours rather than weeks. Faster service reduces the cost of each transaction and improves customer satisfaction directly.

Accuracy: Machine learning models trained on large datasets identify patterns that human reviewers miss. This applies to both risk pricing and fraud detection. Lemonade's AI system has identified fraud schemes by analyzing behavioral patterns in claims submissions. Better accuracy means fewer errors and lower losses over time.

Personalization: Traditional insurance prices risk by averaging across large customer pools. Digital tools allow carriers to price and structure policies based on individual behavior and preferences. Low-risk customers benefit directly. They no longer subsidize higher-risk customers the way they do under traditional pooled pricing models.

Operational Costs: Straight-through processing moves a claim or application from start to finish without human intervention. This reduces the cost per transaction substantially. For high-volume, low-complexity work, automation handles the same output at a fraction of the cost of manual processing.

New Revenue Streams: Digital capabilities allow carriers to launch embedded insurance products, offer micro-coverage options that were not previously economical, and reach customer segments that traditional distribution channels could not serve efficiently.

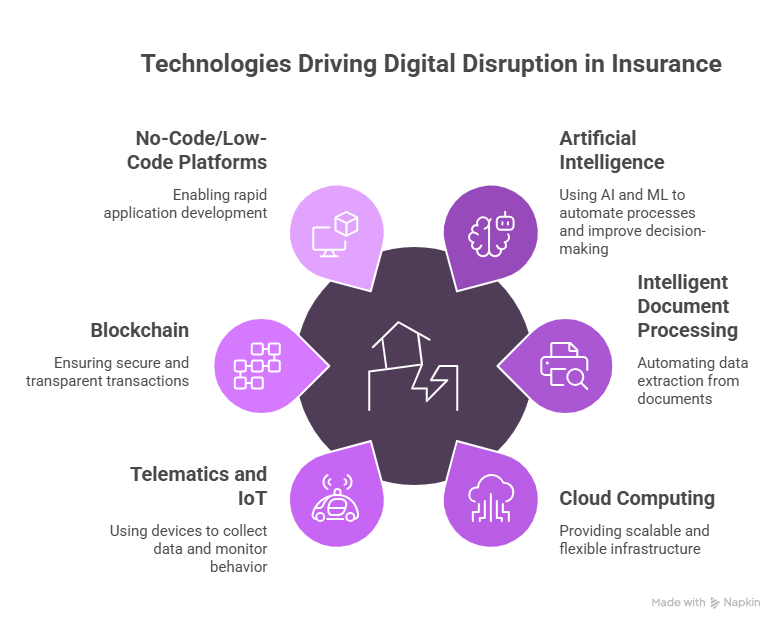

Top Technologies Driving Digital Disruption in Insurance

Several technologies are actively reshaping how insurance companies operate, price risk, and serve customers.

Artificial Intelligence And Machine Learning

They power underwriting models, claims adjudication, fraud detection, customer service automation, and predictive analytics. The accuracy of these systems depends directly on the quality of the data they are trained on.

Intelligent Document Processing (IDP)

IDP addresses one of the most persistent bottlenecks in insurance operations: unstructured data. Claims arrive as PDFs, photographs, handwritten notes, and emails. IDP systems extract and classify that information automatically. The data then flows into downstream systems without manual re-entry, reducing processing time and human error.

Cloud Computing

It gives insurance platforms the infrastructure flexibility they require. Carriers can scale capacity during high-demand periods, run global operations from centralized systems, and connect third-party services through APIs. This removes the need to maintain costly on-premise infrastructure.

Telematics And IoT Devices

This technology feeds real-time data into pricing and risk monitoring. Auto insurers use driving behavior data to price policies. Home insurers use smart sensors to detect water leaks and fire risks. Life insurers integrate data from wearable devices to monitor health metrics. Each additional data source produces a more accurate picture of individual risk.

Blockchain

Blockchain is gaining practical use in reinsurance, where multiple parties must share data and settle transactions with a verifiable record. It is also being applied to parametric insurance products, where claims pay out automatically when a defined external event is confirmed.

No-Code And Low-Code Platforms

This allows business teams to build and update digital workflows without depending on development resources. Insurance products and regulations change frequently. These platforms allow teams to respond to those changes faster than traditional development cycles permit.

How Infrrd Can Help with Digital Disruption in Insurance

Infrrd specializes in intelligent document processing for insurance, which is one of the hardest and highest-value problems in the industry. Insurance workflows are document-heavy: applications, policies, endorsements, claims, medical records, and legal correspondence. Getting information out of those documents quickly and accurately is a prerequisite for almost every other digital initiative.

Infrrd's platform uses AI to extract, classify, and validate data from structured and unstructured insurance documents at scale. That means insurers can process claims faster, reduce manual review, and feed cleaner data into downstream systems, whether those are legacy core platforms or modern cloud-based solutions.

iTrackPro, Infrrd’s next-gen automation solution designed to enhance data tracking in insurance-specific domains, is a data extraction and management solution built specifically for insurance tracking. It includes 60+ extraction form fields and industry-specific documentation capabilities, delivering fast and accurate data extraction where manual and traditional IDP solutions fall short.

The technology handles the variability that makes insurance documents difficult: different layouts, inconsistent formatting, handwritten fields, and multi-page packages that need to be parsed holistically rather than page by page.

For carriers looking to modernize without a full infrastructure overhaul, intelligent document processing is often the highest-leverage starting point.

Conclusion

Digital disruption in insurance is not a future problem. It is a present reality. Carriers that invest in the right technologies, fix their data foundations, and build around the customer will operate faster, price more accurately, and serve more people. Those who wait will find the gap harder to close. The tools exist. The use cases are proven. The next step is execution.

FAQs about Digital Disruption in Insurance

Q. What are the risks of digital disruption in insurance?

The primary risks include technology implementation failures, data security and privacy breaches, regulatory non-compliance, and the risk of moving too fast in ways that alienate existing customers or outpace an organization's change management capacity. There's also model risk — AI systems that perform well in training can behave unexpectedly on real-world data, particularly in markets or conditions they haven't seen before.

Q. What is the process of digital disruption in the insurance industry?

Digital disruption typically follows a pattern: new technology enables a capability that wasn't previously possible or economical; startups or tech-forward incumbents deploy it first; customer expectations shift; competitors respond; and the industry eventually reaches a new normal. In insurance, this process is playing out across underwriting, distribution, claims, and customer service simultaneously, though at different speeds in each area.

Q. What technologies are used in digital disruption?

The most impactful technologies currently shaping digital disruption in insurance include artificial intelligence, machine learning, intelligent document processing, telematics and IoT sensors, cloud computing, APIs and microservices, blockchain, and no-code/low-code development platforms. The combination of these tools — rather than any single one — is what drives meaningful change.

Q. What are the use cases of digital disruption in the insurance sector?

Use cases span the entire insurance value chain. In underwriting: AI-assisted risk scoring, real-time data integration, and automated application processing. In claims: AI triage, automated document extraction, fraud detection, and straight-through processing for simple claims. In distribution: digital brokers, embedded insurance at the point of sale, and direct-to-consumer platforms. In customer service: conversational AI, self-service portals, and proactive policyholder communication. Each use case delivers measurable value on its own, and they compound when built on a shared digital foundation.