ACORD 130 is the cornerstone of workers’ compensation submissions. It standardizes how critical details, like payroll, class codes, loss history, and state exposure, are collected and shared among agencies, carriers, and clients. For professionals managing form intake, review, and submission, the accuracy of ACORD 130 directly influences underwriting speed, compliance quality, and overall policy turnaround.

This guide serves as the definitive resource for ACORD 130 processing, designed for those who handle workers’ compensation applications daily, reviewing data, correcting class code errors, reconciling payroll figures, and resubmitting incomplete files.

It focuses on the real challenges that slow teams down: outdated form versions, manual entry errors, long validation cycles, and limited visibility after submission. It also explores automation strategies that streamline data extraction, validation, and tracking, enabling faster, more reliable, and audit-ready workers’ compensation processing.

What is ACORD 130?

ACORD 130 is the Workers’ Compensation Application form developed by the Association for Cooperative Operations Research and Development (ACORD). Think of it as the official handshake between an insurance agent and a carrier for workers’ comp coverage.

It collects details about a company’s operations, payroll, class codes, prior losses, and safety measures, everything an underwriter needs to evaluate risk and issue a quote. Without this form, workers’ compensation submissions would look like a pile of sticky notes written in different languages.

The goal is standardization. ACORD 130 makes sure everyone, from the smallest local agent to the biggest national carrier, speaks the same data language.

Relation between ACORD 125, 130, and 133 forms

ACORD 125 is the Commercial Insurance Application, used as the base form for most property and casualty lines. ACORD 130 builds on it specifically for workers’ compensation, while ACORD 133 is the Workers’ Compensation Supplement for additional coverage details.

Think of ACORD 125 as the foundation, ACORD 130 as the framework for workers’ comp, and ACORD 133 as the finishing touches. When combined, they paint a complete picture of the insured’s operations, payroll exposure, and loss history.

Importance of ACORD 130 in Workers’ Compensation

The ACORD 130 form plays a central role in workers’ compensation insurance. It captures the essential business, payroll, and loss information that underwriters rely on to assess risk and price coverage accurately. A well-completed ACORD 130 not only accelerates quote turnaround but also minimizes underwriting questions, data discrepancies, and compliance gaps, making it the foundation for efficient and reliable workers’ compensation submissions.

Why brokers, agents, and underwriters rely on ACORD 130

For brokers and agents, ACORD 130 is a must-have. It keeps every submission organized and consistent. Underwriters use it to assess exposure, verify class codes, and decide premium rates. Without this shared structure, every submission would require guesswork, and that’s a recipe for delayed quotes and costly errors.

The form also acts as a single source of truth. Agents attach loss runs, safety documents, and supplemental notes, giving carriers everything they need upfront. That helps prevent the back-and-forth emails that drive everyone slightly mad.

How ACORD 130 streamlines submission and underwriting

When filled out correctly, ACORD 130 shortens underwriting time dramatically. It allows carriers to review risk details, payroll by class code, and experience modifications in one place. Many carriers even auto-import the data directly into their policy systems.

Imagine it as the “speed lane” for workers’ comp submissions, where data moves cleanly, and quotes return faster.

How to Complete ACORD 130 Form (Step-by-Step)

Filling out ACORD 130 isn’t rocket science, but accuracy matters. A single wrong class code or missing signature can send a submission back to square one. Let’s walk through each section.

Applicant and agency information

Start with the basics: business name, contact information, FEIN, and agency code. Double-check spelling. Misspelling a company name might sound trivial, but it can cause claim mismatches later.

Include the producer’s details, agency name, email, and phone number. If multiple offices are involved, list the main contact handling the submission.

Submission and billing details

Specify whether this is a new business, renewal, or rewrite. Mention billing type: direct, agency, or payroll reporting. Many underwriters rely on this field to determine which team handles the application, so clarity helps.

Locations and policy information

List every location where employees work. For companies with multiple states, note each state separately. Workers’ comp laws differ across state lines, so precision here avoids compliance trouble.

Policy information includes effective dates, estimated annual premiums, and proposed carrier. Remember: even rough estimates help underwriters price faster.

Individuals included/excluded.

This section clarifies who is covered under the policy. Owners and officers can often opt in or out of workers’ comp coverage. Clearly mark these boxes; forgetting them may trigger manual clarification calls from carriers.

State rating worksheet and payroll breakdown

Here lies the beating heart of ACORD 130. The payroll table captures class codes, descriptions, and estimated annual payroll for each. Match the class codes to the correct state manual. A single misplaced digit can cause rate miscalculations and re-quotes.

For multi-state operations, attach separate sheets if needed. Underwriters love clean data—they’ll thank you silently.

Prior carrier and loss history

Here, you document prior carriers, policy numbers, and loss runs for the past three years. If a business had zero claims, write “no known losses.” Leaving it blank might raise red flags.

Attach formal loss runs whenever possible. It builds trust and speeds up approvals.

General information (24 standard questions)

This section feels like a pop quiz for workplace safety. Questions cover subcontractors, out-of-state work, safety programs, and employee duties. Each answer guides how an underwriter views risk.

Answer truthfully and completely. Skipping questions leads to “incomplete application” notes—a polite way of saying “please start over.”

Finalizing and signatures

Finally, check every page number. Signatures are required from both the applicant and the agent. A missing signature equals an unsigned check; nobody processes it.

Once complete, review the form for legibility. Handwritten entries still happen, but typed forms reduce interpretation errors.

Common Challenges When Filling Out ACORD 130

Even experienced insurance professionals encounter difficulties when completing the ACORD 130 form. Its detailed structure demands precision, and even small errors, like outdated versions, missing payroll data, or inconsistent class codes, can delay underwriting decisions. Understanding these common challenges helps teams strengthen data accuracy, reduce rework, and maintain smoother submission workflows across all workers’ compensation accounts.

Missing pages or outdated form versions

Using an outdated version is surprisingly common. Carriers update requirements regularly. Always download the latest form from ACORD or your agency management system before filling it out.

Submitting only part of the form is another pitfall. A missing back page can delay binding or force re-submission. Think of it like turning in half a tax return; no one’s happy until it’s complete.

Mismatched class codes and payroll data

Class codes are tricky. A small typo can assign a clerical employee a heavy-machinery rate, inflating premiums overnight. Always cross-check codes with the current NCCI or state manuals.

Payroll estimates must match business realities. If the total payroll on ACORD 130 differs from other documents, underwriters will flag it. Consistency earns credibility.

Incomplete loss history or supporting documents

Many submissions get stuck waiting for loss runs or supplemental forms. Set reminders to collect these before submission. Missing details don’t just delay quotes—they signal a lack of diligence.

Manual data errors and resubmission delays

Manual entry is still the leading cause of submission slowdowns. Typos, missing decimals, and misread handwriting are daily headaches. Each correction restarts the underwriting clock.

Automation can fix that, but we’ll get to it soon.

Why Manual ACORD 130 Processing Slows Teams Down

Manual processing of ACORD 130 forms often turns routine submissions into time-consuming tasks. Re-entering data, verifying fields across multiple systems, and correcting avoidable errors consume hours that could be spent on higher-value work. These repetitive steps not only increase turnaround times but also raise the risk of inaccuracies and missed opportunities for faster, more consistent underwriting decisions. The following are some of the most common pitfalls of manual ACORD 130 form processing.

High error rates and long validation cycles

Paper or PDF-based forms require human review at every step. Agents type data, underwriters re-enter it, and someone else validates it again. Every handoff introduces risk.

Studies show manual insurance data processing can reach error rates of 15–20%, while automated workflows drop that to around 2%. Those errors don’t just waste time—they can mean mispriced policies or rejected quotes.

Inconsistent submissions across agencies

Not all agencies follow the same checklist. Some send every attachment perfectly labeled; others forget key pages. That inconsistency makes carrier intake teams spend hours sorting and verifying each submission.

It’s like trying to assemble furniture without matching screws; everything takes longer.

Limited visibility into submission status

Once an agent emails a PDF, it often disappears into the carrier’s inbox abyss. Tracking status means more phone calls, more spreadsheets, and less time selling. Real-time visibility remains one of the biggest manual pain points in insurance operations.

Automating ACORD 130 Form Processing

Automation is changing how insurers and agencies manage ACORD forms. Instead of treating them as static PDFs, companies now use AI systems to read, extract, and verify data automatically.

Intelligent Document Processing (IDP) and agentic AI explained

Intelligent Document Processing (IDP) combines optical character recognition (OCR), natural language processing, and machine learning to identify and capture data from forms.

Agentic AI adds another layer—it doesn’t just read data; it reasons through it. For instance, it can detect that “class code 8810” should link to clerical work and flag anomalies if payroll looks too high for that category.

Together, they turn ACORD 130 from a static form into a live data source.

Auto-extraction of form data and validation rules

Modern IDP systems, such as Infrrd for Insurance Document Automation, can extract data fields, like business names, payroll totals, and loss dates, directly from ACORD 130 in seconds.

Validation rules check that totals add up, class codes match known categories, and state selections are logical. Instead of hunting through pages, underwriters receive structured data instantly.

Cross-document verification with ACORD 125 and payroll systems

Automation tools can compare ACORD 130 with ACORD 125 and external payroll systems. If the same business lists different payroll totals or operations, the system flags it automatically.

That kind of cross-check reduces friction between underwriting and compliance teams. It also prevents premium leakage caused by data mismatch.

Maker-checker workflows and audit-ready trails

AI-driven systems maintain maker-checker approval loops. The AI acts as the “maker,” pre-filling and verifying data, while human reviewers act as “checkers,” confirming accuracy before submission.

Every edit gets logged, creating a full audit trail, something auditors and regulators love almost as much as coffee.

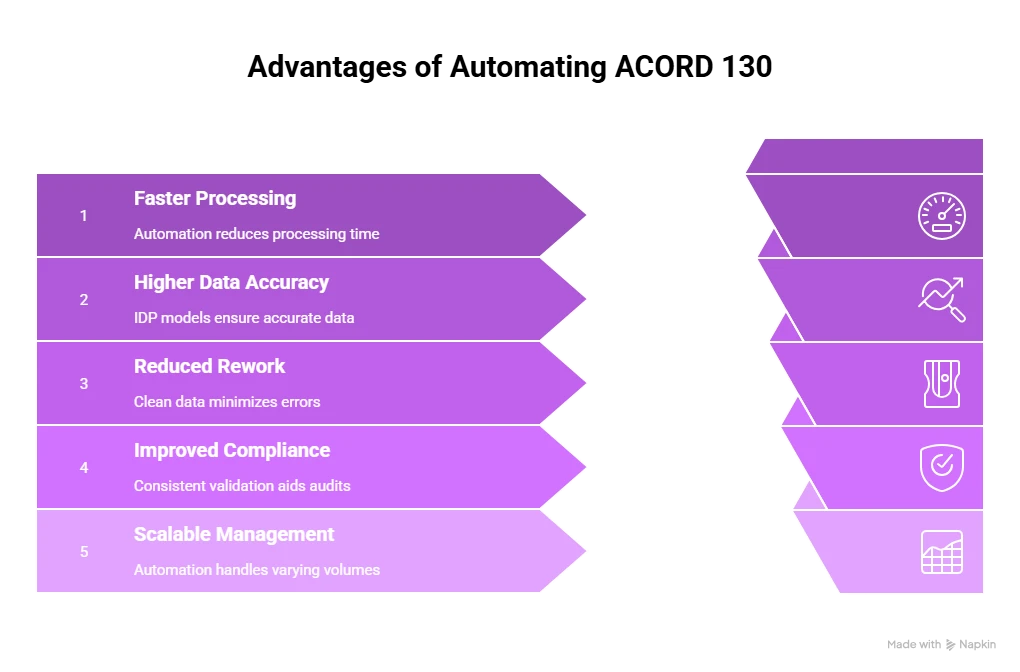

Advantages of Automating ACORD 130

Manual processing of ACORD 130 forms slows down submissions, introduces errors, and ties up valuable time across insurance teams. Automation changes that. By extracting, validating, and routing data automatically, teams can process submissions faster, improve accuracy, and reduce the back-and-forth that typically delays underwriting. This section outlines the key benefits that automation brings to ACORD 130 workflows, helping agencies and carriers scale with consistency and control.

Faster processing and higher data accuracy

Automation reduces processing time dramatically. Submissions that once took hours can now be completed in minutes. With trained IDP models, accuracy rates often hit 90% or higher, outpacing manual review by a wide margin.

That means agencies can handle more accounts without expanding staff—a rare win-win in insurance operations.

Reduction in rework and rejected submissions

Clean data means fewer re-quotes. Carriers don’t need to send back “please clarify” emails, and agents don’t waste time re-keying information.

Improved compliance and audit readiness

Automation enforces consistency. Each field follows the same validation logic, making it easier to prove compliance during audits. Every step is timestamped, ensuring a transparent digital trail.

Scalable submission management

Whether handling ten submissions a day or ten thousand, automation scales effortlessly. The system doesn’t tire, doesn’t miss fields, and doesn’t take a vacation.

Agencies can also integrate automated ACORD 130 processing with CRM and policy-admin tools, creating an end-to-end digital workflow.

How Infrrd Automates ACORD 130 Processing

Infrrd brings automation to life with AI-powered data extraction and agentic reasoning built specifically for complex insurance documents. Its Intelligent Document Processing platform reads, validates, and structures information from ACORD 130 forms and attachments automatically.

AI-powered data extraction from forms and attachments

Infrrd’s engine can recognize printed and handwritten text, detect checkboxes, and capture numeric fields accurately—even when scanned quality varies. It turns PDFs into structured data that’s ready for use in carrier or agency systems.

Instead of uploading forms one by one, users can process entire batches. The AI identifies each ACORD 130 automatically, extracts fields like payroll or FEIN, and aligns them to carrier templates.

Validation across ACORD 125, 130, and 133

Infrrd doesn’t stop at extraction. It cross-validates data between ACORD 125, 130, and 133 forms. For example, if the total payroll in ACORD 130 doesn’t match the commercial operations listed in ACORD 125, it flags the discrepancy for review.

This multi-document reasoning reduces re-submissions and helps maintain clean data across systems.

Real-time dashboards and automated audit reports

Insurance teams can view real-time dashboards showing submission status, accuracy scores, and exceptions. Every processed ACORD 130 generates an audit-ready report, capturing who reviewed what and when.

It’s like giving every submission its own GPS tracker, no more lost files or mystery delays.

Infrrd’s approach helps agencies cut manual effort by more than half while improving accuracy and compliance reporting. The result: faster quotes, happier clients, and fewer sleepless nights for operations teams.

Summary

ACORD 130 may look like just another form, but it’s a key pillar of modern insurance operations. Get it wrong, and submissions stall; get it right, and workflows hum.

With automation, agencies can turn what was once a time-consuming chore into a near-instant process. Infrrd’s platform brings speed, accuracy, and control to this everyday task—freeing teams to focus on what really matters: serving clients and growing business.

FAQs about ACORD 130

What is ACORD 130 used for?

It’s the standard form used to apply for workers’ compensation insurance. It gathers essential information, like payroll, class codes, and prior losses, needed to underwrite coverage.

Who needs to fill out an ACORD 130 form?

Any business applying for workers’ comp coverage, typically through its agent or broker, must complete ACORD 130.

What documents should be attached with ACORD 130?

Attach ACORD 125, ACORD 133 (if needed), and loss runs for the past three years. Some carriers may also ask for a safety program summary or subcontractor agreements.

Can the ACORD 130 be e-signed?

Yes. Most carriers and agency systems now accept electronic signatures, provided they comply with ESIGN and UETA regulations.

What are the common mistakes to avoid while filling out ACORD 130?

Using outdated versions, skipping payroll details, mismatching class codes, or forgetting signatures. Review before sending, it saves everyone’s time.

How does automation help insurance teams?

Automation extracts and validates data instantly, cutting errors and speeding up submissions. It also gives real-time visibility into status and audit history.

What is the difference between ACORD 130 and ACORD 133?

ACORD 130 covers the core workers’ compensation application. ACORD 133 adds supplemental information, such as subcontractor details or state-specific exposures.

What is IDP in insurance automation?

IDP stands for Intelligent Document Processing, a technology that reads and understands documents using AI. It’s what makes tools like Infrrd’s platform process ACORD forms without manual data entry.

Priyanka Joy is a product writer at Infrrd who approaches automation tech like a curious detective. With a love for research and storytelling, she turns technical depth into clarity. When not writing, she’s immersed in dance, theatre, or crafting her next narrative.