Every business carries risk. Construction firms face on-site injuries, retailers worry about customer accidents, and manufacturers fear product liability claims. No matter the industry, liability can strike anywhere with serious financial consequences. That’s why commercial liability insurance is essential. At the heart of how insurers evaluate and price that coverage lies one key document: the ACORD 126 form.

The numbers highlight its importance. The global liability insurance market stood at USD 291.86 billion in 2024 and is on track to reach USD 524.66 billion by 2034, growing at a steady 6.04% CAGR. Yet growth brings new challenges: rising litigation, soaring claim costs, and “nuclear verdicts” that are reshaping underwriting strategies. Insurers are under more pressure than ever, making the accuracy of the forms that guide their decisions vital.

This is why the conversation around ACORD 126 processing and its automation matters now more than ever. Getting it wrong can mean higher premiums, slower coverage, and costly disputes. Managing related workflows, including ACORD 27 automation also requires consistent extraction, validation, and routing across ACORD form submissions.

Let’s uncover what ACORD 126 really is, why it matters, and how automation is transforming the way it’s handled.

What is Acord 126?

ACORD 126 is a standardized form provided by the Association for Cooperative Operations Research and Development (ACORD). It is used primarily for Commercial General Liability (CGL) applications, helping carriers assess a business’s liability risks.

The form includes detailed questions about business operations, products, employee exposure, contractual obligations, premises details, and prior loss history. These data points allow underwriters to evaluate potential risks and price coverage appropriately.

In practice, ACORD 126 acts as a bridge between brokers, insured businesses, and carriers—streamlining communication and ensuring underwriting decisions are based on consistent, comparable information.

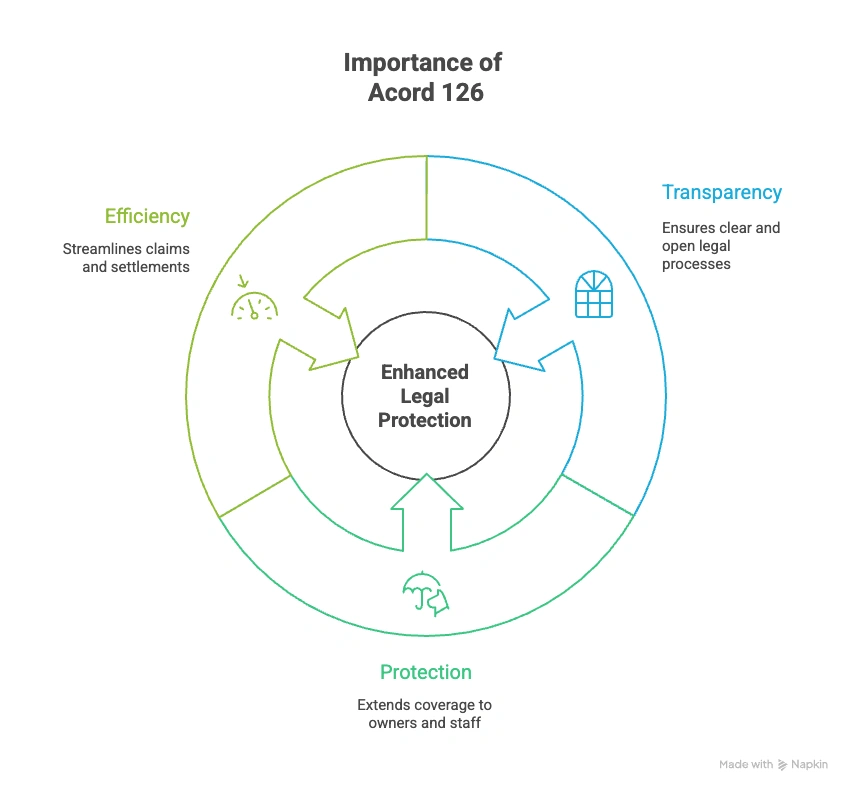

Importance of Acord 126

The significance of ACORD 126 is tied to the growing role of general liability insurance in global markets. General liability is the largest segment within liability coverage (Precedence Research), reflecting its central role in protecting businesses against third-party claims. In the U.S., commercial lines account for about half of all property/casualty premiums, with CGL forming the cornerstone of these commercial lines (Insurance Information Institute).

ACORD 126 ensures that the right data flows into these underwriting processes, helping businesses secure appropriate coverage while giving insurers the visibility they need. Its importance can be broken down further into three dimensions:

Transparency in Legal Liability

General liability insurance is built to cover third-party bodily injury, property damage, and related claims. Completing ACORD 126 thoroughly shows clear disclosure of risks, which not only supports compliance but also prevents gaps in coverage caused by missing or incorrect information.

Extending Protection to Owners and Staff

Everyday operations bring potential risks—slip-and-fall accidents, product-related disputes, or service errors. A properly completed ACORD 126 ensures insurers capture these exposures, enabling policies that safeguard both business owners and employees against costly legal and financial consequences.

Smoother Claims and Faster Settlements

In the event of a claim, underwriters and insurers rely heavily on the original application forms. A detailed ACORD 126 form gives them the clarity they need to evaluate claims quickly, reduce disputes over terms, and accelerate settlement timelines.

How to Read Acord 126

Reading ACORD 126 requires familiarity with insurance terminology and an understanding of underwriting data needs. The form is structured into sections covering:

General Applicant Information

Captures the basics of the business name, contact details, and organizational structure. This helps insurers verify the entity applying for coverage and understand whether it’s a sole proprietorship, partnership, or corporation.

Nature of Operations

Describes what the business actually does, the services it provides, and its industry classification codes. This tells underwriters where the main risks may come from for example, a construction firm carries very different exposures than a retail store.

Exposure Details

Includes payroll size, total sales, use of subcontractors, and employee categories. These figures directly influence premium calculations since they show the scale of operations and potential liability exposure.

Premises and Contracts

Lists owned or leased business locations and any contracts that transfer or share liability. This section signals property-related risks and contractual obligations that may affect coverage needs.

Products and Services

Identifies manufactured, distributed, or serviced products that could create liability if something goes wrong. For instance, a defective product could lead to lawsuits that the insurer must account for.

Loss History

Provides records of prior claims or incidents. A history of frequent or severe claims may indicate recurring risks, which underwriters use to assess insurability and pricing.

Each field directly informs underwriting judgment. Incomplete or inaccurate data can lead to delays, coverage disputes, or higher premiums.

How to Automate Acord 126 Processing

Manual handling of ACORD 126 comes with delays, inconsistencies, and risk of errors. Automation via Intelligent Document Processing (IDP) addresses many of these issues.

Here’s how automation typically works:

- Ingestion & Classification: The system accepts documents in various formats (PDFs, scans, images), classifies them as ACORD 126 or another submission form, such as the ACORD 140 Property Section.

- Pre‐processing: Standardizing orientation, cleaning up scanned pages, handling noise, and identifying layout variations.

- Field detection & Extraction: Using machine learning / template‐agnostic / layout heuristic methods to detect fields like coverage limits, hazards, dates, etc. Also handling checkboxes and handwritten entries.

- Validation & cross‐checking: Validating extracted data against rules (e.g., “if Claims Made is checked, a retroactive date may be required”) or reference data.

- Post-processing/Business logic: Aggregating exposures, computing totals, flagging unusual or missing items.

- Integration: Feeding the validated structured data into underwriting, policy administration, or claims systems.

IDP platform supports all these steps. For example, Infrrd’s IDP Product Overview datasheet describes how the platform handles complex layouts, tables/graphs, multiple languages, layout variations, and noisy backgrounds, and supports guaranteed accuracy.

Also, the Insurance Document Automation blog gives a detailed walkthrough of how document classification, AI‐extraction, validation, and integration can work in insurance workflows.

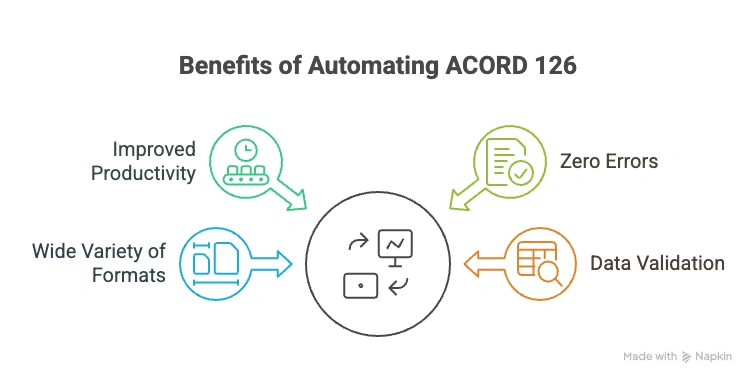

Benefits of Acord 126 Automation

Automation brings measurable benefits to ACORD 126 processing. These include:

1. Improved Productivity and Efficiency

Forms that once required hours of manual review can now be processed in minutes. This efficiency allows underwriters to focus on higher-value tasks such as analyzing risk trends rather than rekeying data.

2. Zero Errors

Manual entry is prone to mistakes, which can have costly downstream effects. Automation minimizes errors by ensuring that extracted data is consistent, validated, and aligned with submission requirements.

3. Wide Variety of Formats

Businesses may submit ACORD 126 forms as PDFs, faxes, or electronic versions. Automation tools handle this variability seamlessly, reducing the need for manual intervention.

4. Data Validation

Automated validation checks flag missing, inconsistent, or inaccurate data before the form reaches underwriting. This ensures cleaner submissions, fewer delays, and faster binding of policies.

Frequently Asked Questions (FAQs) on ACORD Forms

What is ACORD 126?

ACORD 126 is the Commercial General Liability (CGL) Section of the ACORD insurance application forms. It is used to collect detailed underwriting information, such as business operations, exposures, and loss history to help insurers evaluate liability risks and price coverage accurately.

What is the difference between ACORD 125 and ACORD 126?

ACORD 125 is the general liability application form that provides an overview of a business's basic details, operations, and prior losses. ACORD 126, on the other hand, is a supplemental form specifically for liability coverages. It digs deeper into exposures, premises, contracts, and other details that underwriters need to properly assess risk.

What does “exposure” mean on an ACORD 126?

Exposure refers to the elements of a business that could result in liability claims. Common exposure factors include payroll, sales, use of subcontractors, and employee roles. These numbers help insurers estimate how likely a business is to face claims and set appropriate premiums.

Why is loss history important on ACORD 126?

Loss history shows prior claims or incidents involving the business. A strong history with few or no claims may lead to more favorable terms, while repeated claims can raise red flags and increase costs.

Who typically completes an ACORD 126 form?

Agents or brokers usually fill out ACORD 126 on behalf of their clients. They gather information from the business, ensure accuracy, and submit the form to insurers as part of the underwriting process.

Market Context: Why Automation is Timely?

The push for automating ACORD 126 is tied to broader market trends. The global general liability insurance market is projected to grow from USD 291.86 billion in 2024 to nearly 495.51 billion by 2033, at a CAGR of 5.9%.

At the same time, underwriting is becoming more complex. Rising litigation, “nuclear” jury verdicts, and increased regulatory exposure are forcing insurers to scrutinize submissions more carefully. Automation ensures that forms are accurate, complete, and ready for evaluation, making the underwriting process both faster and safer.

In a Nutshell

Manual processing of ACORD 126 slows down underwriting, risks errors, and leaves insurers vulnerable to incomplete submissions. By adopting automation through Intelligent Document Processing (IDP), brokers and carriers can turn ACORD 126 into a streamlined, high-accuracy workflow.

With Insurance Document Automation, organizations gain the ability to:

- Process ACORD forms across multiple formats

- Reduce errors through automated validation

- Free underwriters from manual data entry to focus on decision-making

In an industry facing tougher litigation, stricter regulation, and rising claims costs, smarter ACORD form processing is a strategic necessity and that includes workers compensation form automation guide for insurance teams for a fully streamlined commercial submission workflow. Take your pick wisely.

Bhavika Bhatia is a Product Copywriter at Infrrd who blends curiosity with clarity to craft content that makes complex tech feel simple and human. With a background in philosophy and a knack for storytelling, she turns big ideas into meaningful narratives. Outside of work, you’ll find her chasing the perfect café corner, binge-watching a new series, or lost in a book that sparks more questions than answers