Die manuelle Dateneingabe ist nach wie vor eines der größten Hindernisse für Branchen, die stark auf Dokumente angewiesen sind. Hypothekengeber verarbeiten Tausende von Seiten pro Kreditdatei. Versicherungsträger bearbeiten unzählige Ansprüche und Versicherungsformulare. Finanzteams prüfen täglich Rechnungen und Quittungen. Ingenieurbüros überprüfen Zeichnungen, Schaltpläne und technische Diagramme.

In all diesen Sektoren ist die Herausforderung dieselbe: Wichtige Informationen sind in Dokumenten eingeschlossen, und die manuelle Eingabe verlangsamt alles.

Hier hilft Datenextraktionssoftware.

Angesichts der Tatsache, dass Dutzende von Plattformen verfügbar sind, kann es sich im Jahr 2025 jedoch überwältigend anfühlen, die beste Datenextraktionssoftware zu finden.

In diesem Handbuch wird beschrieben, was Datenextraktionssoftware ist, warum sie wichtig ist, wie sie funktioniert und welche Top-Plattformen es heute wert sind, in Betracht gezogen zu werden.

Was ist RPA bei Versicherungsansprüchen?

RPA bei der Bearbeitung von Versicherungsansprüchen verwendet Bots, Softwareroboter, die menschliche Tastatureingaben und Klicks nachahmen, um sich wiederholende Schadensaufgaben zu erledigen. So gibt ein RPA-Bot beispielsweise die Versicherungsnummern automatisch ein und validiert sie systemübergreifend, anstatt dass ein Sachbearbeiter die Versicherungsnummern manuell erneut eingibt.

Wo es in dokumentenintensive Arbeitsabläufe passt (FNOL → Adjudication → Settlement)

Bei einer Schadensabwicklung voller Dokumente: ACORD-Formulare, Ausweise, Rechnungen, Kostenvoranschläge, Polizeiberichte und Policenakten, fungiert RPA als Koordinator. Es erfasst eingehende Nachrichten aus E-Mails und Portalen, dedupliziert sie, benennt und indexiert Dateien und überträgt Metadaten in das zentrale Schadensystem. Außerdem werden die richtigen Aufgaben gestartet (Deckungsprüfungen, Inspektionen, Lieferantenbestellungen) und der Status aller Tools wird synchronisiert. In Kombination mit KI zum Lesen von Dokumenten werden Felder wie Versicherungsnummer, Verlustdatum, Einzelposten und Summen extrahiert. In Kombination mit Validierungsregeln werden Namen, Adressen, Limits und Selbstbehalte abgeglichen. In Kombination mit Risikomodellen bewertet es Schweregrad- oder Betrugssignale, um die Arbeit an die richtige Warteschlange weiterzuleiten. Das Ergebnis sind kürzere Zykluszeiten, sauberere Übergaben, weniger Wiederholungen und ein vollständiger Audit-Trail, sodass die Sachbearbeiter ihre Zeit mit Ausnahmen und Entscheidungen verbringen, während einfache Fälle direkt bearbeitet werden.

Hier finden Sie eine kurze Aufschlüsselung der Frage, an welcher Stelle RPA in den Bearbeitungszyklus von Schadensfällen passt. Einige Schritte spiegeln das zukünftige Potenzial wider und sind möglicherweise noch nicht verfügbar.

FNOL (Erste Verlustmeldung)

Sammelt, was ankommt: Überwacht E-Mails, Portale und Agenten-Uploads und speichert dann alles, was im Antrag enthalten ist.

- Richtet den Anspruch ein: Erstellt den Datensatz im Kernsystem und hängt die richtigen Dateien an.

- Liest die Dokumente: Sendet Formulare an KI, um grundlegende Informationen wie Versicherungsnummer, Verlustdatum und Informationen zum Antragsteller abzurufen.

- Findet, was fehlt: Wenn eine Seite oder Signatur fehlt, wird automatisch danach gefragt.

Deckungscheck

- Schlägt die Richtlinie nach: Ruft Erklärungen und Vermerke ab.

- Vergleicht Details: Ordnet Gefahren, Grenzwerte, Selbstbehalte, Namen und Adressen den gemeldeten Daten zu.

- Führt ein Protokoll: Versieht jede Aktion mit einem Zeitstempel für die Prüfung.

Triage und Zuordnung

- Hilft beim Routing: Sendet wichtige Fakten an ein Bewertungsmodell und fügt die Punktzahl dem Antrag hinzu.

- Weist das richtige Team zu: Leitet je nach Bedarf an Schreibtisch, Feld, Straight-Through oder SIU weiter.

- Bücher funktionieren: Plant Inspektionen und Lieferanten; sendet Updates an alle.

Untersuchung

- Sammelt Beweise: Ruft Kostenvoranschläge, Reparaturrechnungen und Arztrechnungen ab.

- Ruft Einzelposten ab: Verwendet KI zum Lesen von Tabellen (Teile, Arbeit, Codes, Summen).

- Prüft die Preise: Vergleicht Gebühren mit Preislisten oder Gebührentabellen und kennzeichnet Ausreißer.

- Hinweise zur Aktualisierung: Fügt der Antragsdatei klare, verknüpfte Notizen hinzu.

Entscheidung (Entscheidung und Höhe)

- Macht die Mathematik: Wendet Limits, Selbstbehalte und Abschreibungen an.

- Erstellt ein Paket: Bündelt die wichtigsten Dokumente und extrahierten Felder für den Adjuster.

- Erzeugt Buchstaben: Bereitet Genehmigungs-, Ablehnungs- oder Erklärungsschreiben mit den richtigen Beträgen vor.

Abrechnung und Zahlung

- Startet die Zahlung: Richtet ACH ein oder checkt Finanzsysteme ein und aktualisiert Reserven.

- Schließt sauber: Überprüft, ob alle erforderlichen Dokumente vorhanden sind, und schließt dann den Antrag.

- Sendet Bestätigungen: Benachrichtigt den Antragsteller und die Verkäufer und speichert Kopien.

Nach der Abrechnung

- Berichte: Erstellt termingerecht Berichte über Zykluszeiten, Denial-Reason und Leckagen.

- Qualitätskontrollen: Ruft zufällige Fälle zur Qualitätssicherung ab und verpackt sie für Auditoren.

- Verbessert das System: Führt die Ergebnisse an die KI zurück, sodass Extraktion und Routing mit der Zeit besser werden.

Von der FNOL bis zur Abrechnung kümmert sich RPA um die Klicks und Übergaben. Dokumente werden schneller übertragen, Systeme bleiben synchron und die Sachbearbeiter erhalten übersichtlichere Dateien mit weniger Verzögerungen.

RPA im Vergleich zu IDP im Vergleich zu Agentic AI (wann sollte welche verwendet werden)

RPA bei Versicherungsansprüchen = Automatisiert regelbasierte Schritte

Robotic Process Automation (RPA) wurde entwickelt für strukturierte, sich wiederholende, regelgesteuerte Aufgaben. Bei Versicherungsansprüchen bedeutet das, dass Bots automatisch:

- Extrahieren Sie Policenzahlen aus strukturierten Formularen.

- Geben Sie die Antragsdetails in mehrere Systeme ein.

- Führen Sie routinemäßige Überprüfungen durch, z. B. die Überprüfung des Versicherungsschutzes anhand der Versicherungsgrenzen

Wann sollte RPA verwendet werden

RPA ist ideal, wenn die Daten bereits strukturiert sind (z. B. Tabellen, digitale Formulare) und die Schritte kein Urteilsvermögen erfordern, sondern nur Geschwindigkeit, Genauigkeit und Konsistenz. Stellen Sie es sich wie den „digitalen Fließbandarbeiter“ für Schadensfälle vor.

IDP = Extrahiert und interpretiert unstrukturierte Daten

Intelligent Document Processing (IDP) erweitert die Automatisierung auf unstrukturierte oder halbstrukturierte Daten. Bei der Schadenbearbeitung ist nicht alles in einer ordentlichen Form, viele Dokumente sind PDFs, Bilder oder handschriftliche Notizen. IDP verwendet OCR (Optical Character Recognition), NLP (Natural Language Processing) und maschinelles Lernen, um:

- Extrahieren Sie wichtige Datenfelder aus ACORD-Formularen, Rechnungen oder Krankenhausberichten.

- Interpretieren Sie handschriftliche Aussagen oder Arztnotizen.

- Analysieren Sie unstrukturierte E-Mails und Anlagen, die im Rahmen von Ansprüchen eingereicht wurden.

Wann sollte IDP verwendet werden

IDP ist unerlässlich, wenn Ansprüche unterschiedliche Dokumenttypen und Formate betreffen, die RPA allein nicht verarbeiten kann. Es ist der „Leser und Interpreter“ im Automatisierungs-Toolkit und wandelt unübersichtliche, reale Dokumente in saubere, strukturierte Daten um, auf die RPA reagieren kann.

Agentic AI = Verwaltet durchgängige Schadensfälle im Kontext

Agentic AI geht über die Automatisierung hinaus — sie fügt hinzu Entscheidungsfindung, Kontext und Koordination. Im Gegensatz zu RPA oder IDP, die diskrete Aufgaben erledigen, kann agentische KI:

- Koordinieren Sie mehrere Bots und IDP-Engines über den gesamten Schadenzyklus hinweg.

- Entscheiden Sie anhand des Antragskontextes über die nächstbeste Vorgehensweise (z. B. potenziellen Betrug melden, fehlende Dokumente anfordern oder eine Zahlung auslösen).

- Lernen Sie aus historischen Behauptungen, um die Genauigkeit und Entscheidungslogik im Laufe der Zeit zu verbessern.

Wann sollte Agentic AI verwendet werden

Agentic AI ist am wertvollsten, wenn Sie wollen Automatisieren Sie den gesamten Schadenprozess, nicht nur einzelne Schritte. Anstatt beispielsweise auf die Überprüfung durch einen Gutachter zu warten, kann eine künstliche Intelligenz Dokumente validieren, Betrugsprüfungen durchführen, eine Entscheidung treffen und eine Auszahlungsempfehlung ausarbeiten, sodass Mitarbeiter nur Ausnahmen überprüfen können. Sie fungiert als „Schadensmanager“ und stellt sicher, dass alle wichtigen Teile zusammenarbeiten.

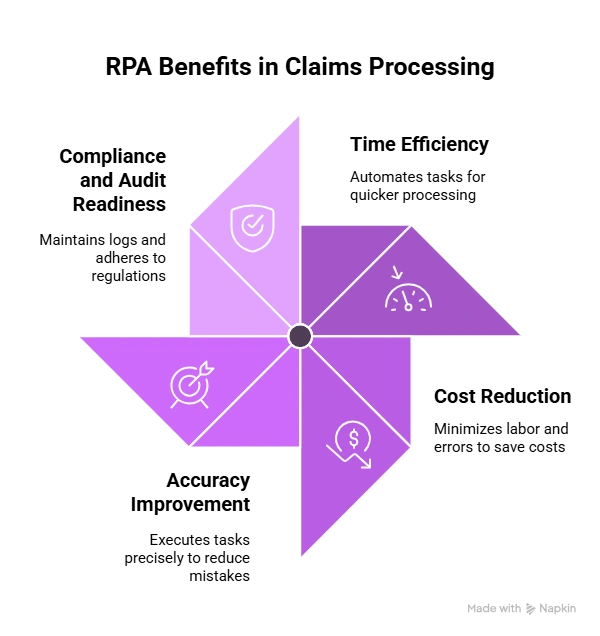

Warum RPA in Claims Matters?

Schadenteams jonglieren mit Bergen von Dokumenten und wiederholen den ganzen Tag über dieselben Schritte — Kopieren, Prüfen, Weiterleiten, Wiederholen. RPA nimmt ihnen diese routinemäßigen Klicks ab, verschiebt Daten zwischen Systemen und löst automatisch die nächste Aufgabe aus. Der Nutzen ist einfach: schnellere Zykluszeiten, niedrigere Kosten, weniger Fehler und zufriedenere Kunden.

Zeit

RPA verschiebt Dateien, füllt Felder aus und startet Aufgaben, ohne auf Mitarbeiter warten zu müssen. Es leitet saubere Anträge direkt durch und schiebt Ausnahmen in die richtige Warteschlange. Dadurch wird der Weg vom FNOL über die Entscheidung bis zur Zahlung verkürzt und die Zykluszeit oft drastisch verkürzt, insbesondere bei Schadensfällen mit hohem Volumen und geringer Komplexität. Mit RPA bei der Bearbeitung von Versicherungsansprüchen verkürzen sich die Zykluszeiten um bis zu 75%.

Kosten

Die Bearbeitung von Schadensfällen ist arbeitsintensiv. Bots übernehmen wiederholbare Schritte wie Dateneingabe, Suche nach Richtlinien und Dokumentenabgleich. Das reduziert die Anzahl manueller Minuten pro Schadensfall, Überstunden und Nacharbeit. Sie erhöhen die Kapazität, ohne die Mitarbeiterzahl zu erhöhen, was die Stückkosten bei steigendem Volumen senkt.

Genauigkeit

RPA wendet jedes Mal dieselben Regeln auf die gleiche Weise an. Es zieht Daten direkt aus Dokumenten und Systemen ab und reduziert so Fehler beim Kopieren und Einfügen. Dank der integrierten Validierungen (Namen, Adressen, Limits, Selbstbehalte) fallen weniger Über- oder Unterzahlungen, weniger Wiederholungen und übersichtlichere Dateien für Sachbearbeiter an.

Konformität und Auditbereitschaft

Jede Bot-Aktion wird mit einem Zeitstempel versehen und protokolliert, wodurch ein vollständiger Audit-Trail erstellt wird. Standardprüfungen und konsistente Ergebnisse machen es einfacher nachzuvollziehen, wie eine Entscheidung getroffen wurde. Wenn Aufsichtsbehörden oder Auditoren nach Nachweisen fragen, können Sie innerhalb von Sekunden angeben, wer was wann getan hat.

Beispiele aus der Praxis und Fallstatistiken

- 65% Rückgang der Kundendienstkosten nachdem RPA die Anzahl der Anrufe reduziert hatte.

- 30-Punkt-NPS Verbesserung im Durchschnitt, mit 88% der Kunden bevorzugen automatische Schadensfälle für Schnelligkeit und Konstanz

So funktioniert RPA bei der Schadensbearbeitung

Im Folgenden finden Sie eine schrittweise Übersicht über den Schadenverlauf mit RPA bei der Bearbeitung von Versicherungsansprüchen. Stellen Sie sich den Bot als Orchestrator vor: Er überwacht Kanäle, verschiebt Daten, ruft Dienste (wie OCR/IDP) an, wendet Regeln an, aktualisiert Kernsysteme und teilt Personen Ausnahmen aus.

1) Aufnahme und FNOL: Kanäle und Identitätsprüfungen

Was der Bot macht

- Überwacht alle Einlasskanäle. Überwacht E-Mail-Posteingänge, Webportale, mobile Uploads, Callcenter-Warteschlangen und SFTP-Drops.

- Erstellt die Claim-Shell. Öffnet im Kernsystem einen neuen Schadensdatensatz mit grundlegenden Metadaten (Antragsteller, Datum des Schadens, Ort des Schadens).

- Erfasst und katalogisiert Dokumente. Speichert Anlagen, benennt Dateien nach einer Standardkonvention, kennzeichnet sie (ACORD, ID, Rechnung, Kostenvoranschlag, Foto) und verknüpft sie jeweils mit dem Antrag.

- Startet Richtlinien- und Ausweiskontrollen. Ruft APIs für die Policenverwaltung auf, um den aktiven Versicherungsschutz, den Selbstbehalt und die Limits zu bestätigen; löst bei Bedarf KYC-/ID-Prüfungen aus.

- Jagt nach fehlenden Gegenständen. Wenn eine erforderliche Seite oder Signatur fehlt, sendet automatische Anfragen und verfolgt die Antworten.

Bot-Mechanik

- Zeitpläne und Auslöser basieren auf SLAs.

- Wiederholte Versuche bei Netzwerk-Timeouts.

- Protokolliert jeden Schritt für das Audit (wer/was/wann).

2) Verständnis der Dokumente: OCR → IDP → Validierungsregeln

Was der Bot macht

- Sendet Dateien zur Extraktion. Sendet PDFs/Bilder an OCR/IDP Endpunkte und empfängt strukturierte Daten (JSON/CSV).

- Normalisiert Felder. Ordnet die Feldnamen der Anbieter internen Standards zu (z. B. „Policy #“, „PolicyNumber“, „PolNo“ → policy_number).

- Wendet Validierungsregeln an. Prüft erforderliche Felder, Formate und Bereiche (Daten, Beträge, Versicherungsnummern).

- Vollständigkeit der Ergebnisse. Markiert jedes Dokument als „bestanden“, „muss überprüft werden“ oder „fehlende Informationen“ und aktualisiert dann den Antragsdatensatz.

Bot-Mechanik

- Ruft den Status des Extraktionsjobs ab, bis er abgeschlossen ist.

- Behandelt Teilergebnisse sicher (schreibt, was verfügbar ist; markiert Lücken).

- Versionskontrolle der extrahierten Nutzlast aus Gründen der Rückverfolgbarkeit.

Hinweis: Die Bot „liest“ nicht. Es Anrufe OCR/IDP, validiert dann und leitet die Ergebnisse weiter.

3) Dokumentenübergreifende Prüfungen: ACORD-Formulare, Rechnungen, Fotos

Was der Bot macht

- Querverweise auf Felder zwischen Dateien. Vergleicht Namen, Adressen, VINs, Versicherungsnummern, Verlustdaten und Schadensbeträge in ACords, Rechnungen, Schätzungen, Fotos und Versicherungsdokumenten.

- Führt Konsistenzprüfungen durch. Überprüft, ob ein Rechnungsbeleg in einem Kostenvoranschlag enthalten ist oder ob die Fotometadaten mit der angegebenen Uhrzeit/dem angegebenen Ort übereinstimmen.

- Kennzeichnet Unstimmigkeiten mit dem Kontext. Erstellt einen eindeutigen Ausnahmehinweis (z. B. „ACORD-Verlustdatum 02/11 versus Rechnungsdatum 01/28; überschreitet die Wartezeit der Police“) und fügt die Nachweise bei.

- Bereitet Adjuster-Pakete vor. Bündelt die relevanten Seiten, hebt die betreffenden Felder hervor und weist die Aufgabe zu.

Bot-Mechanik

- Verwendet Regelbibliotheken für die Abgleichslogik (exakt, unscharf oder schwellenwertbasiert).

- Schreibt Querverweisergebnisse zurück zum Antrag auf Prüfung und Analyse.

4) Human-in-the-Loop: Maker-Checker und Ausnahmen

Was der Bot macht

- Leitet saubere Fälle direkt durch. Wenn die Regeln eingehalten werden und die Schwellenwerte eingehalten werden, wird der Antrag ohne menschliches Zutun zur nächsten Stufe weitergeleitet.

- Eskaliert Grenzfälle. Öffnet Aufgaben für Gutachter mit vorgefüllten Notizen, direkten Vergleichen und Links zu den Originaldokumenten.

- Sammelt Entscheidungen. Liest die Genehmigung/Ablehnung oder die angeforderten Änderungen durch den Einsteller aus und aktualisiert alle Systeme entsprechend.

- Schließt die Schleife. Prüft erneut, wenn neue Dokumente eintreffen; weist Aufgaben neu zu, wenn SLAs gefährdet sind.

Bot-Mechanik

- Erzwingt die Trennung zwischen Hersteller und Prüfer (kein einzelner Benutzer kann gleichzeitig etwas erstellen und genehmigen).

- Führt einen unveränderlichen Prüfpfad mit Zeitstempel für jede Aktion und Entscheidung.

5) Integrationen mit Guidewire, Duck Creek, Salesforce, FSC

Was der Bot macht

- Stellt eine Verbindung zu Kernplattformen her. Lies/schreibt Forderungen, Policen, Notizen, Aufgaben, Reserven und Zahlungen in Führungsdraht oder Duck Creek.

- Synchronisiert mit CRM/Portalen. Verschiebt Statusmeldungen und Aufgaben in Salesforce oder Cloud für Finanzdienstleistungenund löst Benachrichtigungen über Antragsteller und Vertreter aus.

- Überbrückt alte Lücken. Wenn keine API vorhanden ist, automatisiert sicher die Benutzeroberfläche (Bildschirmautomatisierung) mit rollenbasierten Anmeldeinformationen und geschützter Sitzungsverwaltung.

- Sorgt dafür, dass Systeme ausgerichtet sind. Stellt sicher, dass jedes Update (z. B. Deckungsentscheidung, Zahlungsauslöser) nahezu in Echtzeit auf allen verbundenen Systemen wiedergegeben wird.

Bot-Mechanik

- Priorisiert API-Aufrufe, sofern verfügbar; greift mit Resilienz (Selektoren, Wartezeiten, Checkpoints) auf die Benutzeroberflächenautomatisierung zurück.

- Implementiert Ratenbegrenzung und Backoff, um Drosselungen zu vermeiden.

- Verwendet geheime Tresore für Anmeldeinformationen; verschlüsselt Daten während der Übertragung und im Ruhezustand.

Die wichtigsten Herausforderungen beim Einsatz von RPA bei der Bearbeitung von Versicherungsansprüchen

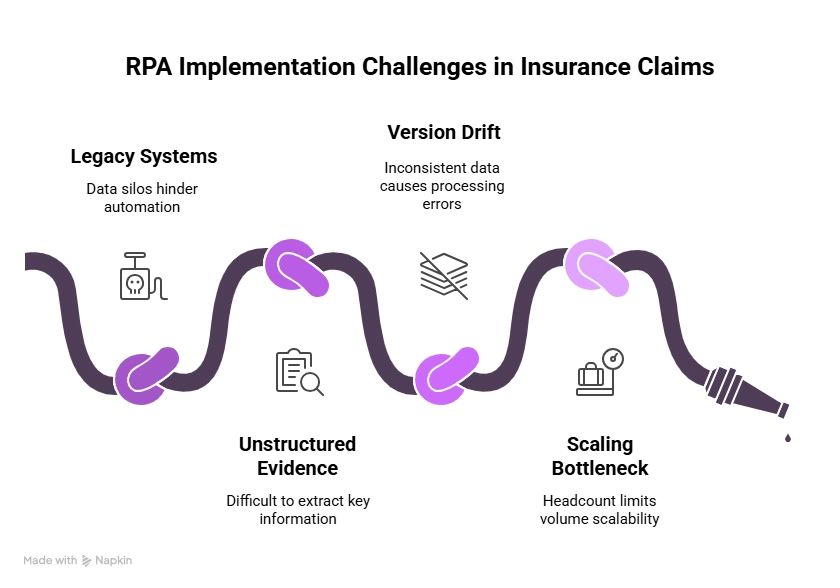

1. Altsysteme und fragmentierte Daten

Viele Versicherer verlassen sich immer noch auf Mainframes und Systeme, die vor Jahrzehnten gebaut wurden. Diese Plattformen wurden nicht für die Integration mit modernen Tools entwickelt, wodurch Silos entstehen, in denen Schadens-, Versicherungs- und Kundendaten an getrennten Orten gespeichert werden. Wenn RPA eingeführt wird, muss es oft als Brücke dienen und Daten zwischen diesen Altsystemen kopieren und verschieben, ohne bestehende Arbeitsabläufe zu unterbrechen.

- Warum es eine Herausforderung ist: Bei älterer Software fehlen möglicherweise APIs, sodass Bots menschliche Tastatureingaben nachahmen müssen, was bei Systemaktualisierungen fragil sein kann.

- Auswirkung: Automatisierungsprojekte erfordern möglicherweise Orchestrierungsplattformen, die Daten systemübergreifend vereinheitlichen, was die Komplexität und die Kosten erhöht.

2. Unstrukturierte Beweise (Handschrift, Bilder, Stempel)

Nicht bei allen Antragsdokumenten handelt es sich um saubere Formulare. Viele enthalten Arztbriefe, Polizeiberichte, unterschriebene eidesstattliche Erklärungen oder gescannte Belege, die Handschriften, Bilder oder Stempel enthalten. Herkömmliches RPA kann diese Formate nicht interpretieren.

- Warum es eine Herausforderung ist: Ohne die Hilfe fortschrittlicher OCR und KI können Bots keine Handschrift „lesen“ oder visuelle Daten verstehen.

- Auswirkung: Versicherer müssen IDP- (Intelligent Document Processing) und KI-Modelle zusätzlich zu RPA hinzufügen, um diese Daten zuverlässig zu extrahieren. Selbst dann können Handschrift und Bildqualität die Genauigkeit beeinträchtigen.

3. Versionsabweichung und fehlende Dokumente

An Schadensfällen sind häufig mehrere Parteien beteiligt, Versicherungsnehmer, Vertreter, Reparaturwerkstätten und Krankenhäuser, die jeweils zu unterschiedlichen Zeiten Dokumente einreichen. Das erzeugt mehrere Versionen derselben Datei oder unvollständige Antragsunterlagen.

- Warum es eine Herausforderung ist: Ohne Automatisierung verbringen Mitarbeiter Stunden damit, Versionen abzugleichen, fehlende Dokumente anzufordern und deren Richtigkeit zu überprüfen.

- Auswirkung: RPA kann helfen, indem es Versionen automatisch abgleicht, Unstimmigkeiten kennzeichnet und Teams alarmiert, wenn erforderliche Dokumente fehlen. Dies erfordert jedoch ausgefeilte Regeln für die Behandlung von Ausnahmen, um Verzögerungen zu vermeiden.

4. Volumen skalieren, ohne die Mitarbeiterzahl zu skalieren

Das Volumen von Versicherungsansprüchen kann im Laufe der Zeit dramatisch ansteigen Naturkatastrophen, Pandemien oder katastrophale Ereignisse. Beispielsweise kann ein Hurrikan innerhalb weniger Tage Tausende von Sachschadensersatzansprüchen nach sich ziehen.

- Warum es eine Herausforderung ist: Manuell arbeitende Teams können nicht schnell genug skalieren, um plötzliche Überlastungen zu bewältigen, was zu Verzögerungen und schlechtem Kundenerlebnis führt.

- Auswirkung: RPA bietet flexible Skalierbarkeit — Bots können sofort eingesetzt werden, um erhöhte Arbeitslasten zu bewältigen, ohne dass neue Mitarbeiter eingestellt oder geschult werden müssen. Dennoch müssen Versicherer bei komplexen Fällen ein Gleichgewicht zwischen Automatisierung und menschlicher Aufsicht finden.

Checkliste für die Implementierung von RPA in Claims

Bei der Implementierung von RPA in Schadenfällen geht es nicht nur um den Einsatz von Bots, sondern auch darum, Mitarbeiter, Prozesse und Technologien so aufeinander abzustimmen, dass sie nahtlos zusammenarbeiten. Ein strukturierter Rollout stellt sicher, dass die Automatisierung messbare Ergebnisse liefert, ohne den laufenden Betrieb zu stören.

- Eignungsbeurteilung (Umfang, SLAs, Dokumente)

Prüfen Sie vor der Implementierung, ob Ihr Schadenumfeld bereit ist:

- Volumen der Dokumente: Identifizieren Sie häufig auftretende Schadensarten: FNOLS, ACORD-Formulare, Rechnungen und Korrespondenz, die reif für eine Automatisierung sind.

- SLAs und Prozesszeitpläne: Machen Sie sich ein Bild von bestehenden Bearbeitungszeiten und Service-Level-Zielen, um messbare Verbesserungsziele festzulegen.

- Vielfalt dokumentieren: Katalogisieren Sie die verschiedenen Eingabeformate (PDFs, gescannte Bilder, Formulare, E-Mails), um sicherzustellen, dass Ihre RPA-Lösung die Aufnahme mehrerer Formate unterstützt.

Diese Basisbewertung setzt realistische Erwartungen und bestimmt, wo die Automatisierung zuerst die größte Wirkung erzielen kann.

- Pilotplan (KPIs, Golden Dataset, Kriterien)

Eine erfolgreiche RPA-Reise beginnt mit einem eng umrissenen Pilotprojekt.

- Definieren Sie KPIs: Konzentrieren Sie sich auf messbare Kennzahlen — Genauigkeitsrate, Verkürzung der Zykluszeit, behandelte Ausnahmen und Kosten pro Schadensfall.

- Goldener Datensatz: Verwenden Sie eine repräsentative Mischung von Behauptungen, um die Automatisierungspipeline in einfachen, moderaten und komplexen Fällen zu trainieren und zu testen.

- Erfolgskriterien: Legen Sie Schwellenwerte für Automatisierungsgenauigkeit, Ausnahmeraten und manuelle Kontaktpunkte fest, bevor Sie weiter skalieren.

Die Pilotphase schafft Vertrauen in die Technologie und bildet interne Champions heraus, die sich für eine Expansion einsetzen können.

- Rollout-Playbook (Menschen, Prozesse, Plattform)

Sobald das Pilotprojekt erfolgreich ist, planen Sie eine schrittweise Einführung.

- Leute: Definieren Sie Rollen für Schadenexperten, IT- und RPA-Administratoren. Erstellen Sie eine Feedback-Schleife, in der menschliche Prüfer Ausnahmen behandeln und die Bot-Logik kontinuierlich verfeinern.

- Prozess: Dokumentieren Sie den gesamten Arbeitsablauf — von der Datenaufnahme bis zur Entscheidungsfindung — und stellen Sie sicher, dass die Schritte zur Ausnahmebehandlung standardisiert sind.

- Plattform: Integrieren Sie Ihre RPA-Tools in bestehende Claim-Management-Systeme, Data Lakes und Audit-Dashboards, um eine durchgängige Transparenz zu gewährleisten.

Ein starkes Playbook hilft dabei, die Automatisierung zu skalieren und gleichzeitig die Kontrolle und Einhaltung der Vorschriften in allen Regionen und Geschäftsbereichen aufrechtzuerhalten.

ROI und Geschäftsvorteile von RPA

Der Wert von RPA bei Schadensfällen geht weit über die Zeitersparnis hinaus — sie definiert Effizienz, Genauigkeit und Kostenkontrolle über den gesamten Schadenszyklus hinweg neu.

Kosten- und Zykluszeiteinsparungen

Die Automatisierung reduziert die manuelle Handhabung und macht wiederholte Dateneingaben überflüssig, wodurch die Betriebskosten um bis zu 60% in einigen Versicherungsabläufen. Anträge, deren Registrierung, Validierung und Genehmigung früher Tage gedauert haben, können jetzt innerhalb von Minuten bearbeitet werden, sodass sich die Teams auf wichtigere Ausnahmen und die Kundenkommunikation konzentrieren können.

Messgenauigkeit und Durchsatz

RPA gewährleistet die Datenkonsistenz, indem menschliche Fehler minimiert und die Validierungsschritte standardisiert werden. Zu den wichtigsten zu überwachenden Kennzahlen gehören:

- Straight-Through-Verarbeitungsrate (STP%) — der Prozentsatz der Anträge, die ohne menschliches Eingreifen bearbeitet wurden.

- Genauigkeit der Datenextraktion — Vergleich automatisierter Daten mit Ground Truth.

- Durchsatz pro Agent oder Bot — Bewertung der Produktivitätsverbesserungen nach der Automatisierung.

- Kontinuierliche Überwachung hilft dabei, das Gleichgewicht zwischen Automatisierung und menschlicher Kontrolle zu finden.

SLA-Verbesserungen vor und nach dem Vergleich

Vor RPA bedeutete die Einhaltung von SLAs oft, die Anzahl der Mitarbeiter zu erhöhen oder die Schichten zu verlängern. Nach der Automatisierung berichten Versicherer von dramatischen SLA-Verbesserungen — die Bearbeitungszeiten verkürzen sich um 30— 70%, Genauigkeit oben stabilisiert 95%, und die Warteschlangen für Ausnahmen wurden um die Hälfte reduziert. Diese Ergebnisse verbessern nicht nur die betriebliche Leistung, sondern auch die Kundenzufriedenheit und die Einhaltung der Vorschriften.

KI-gestütztes IDP: Die moderne Alternative für RPA bei der Bearbeitung von Versicherungsansprüchen

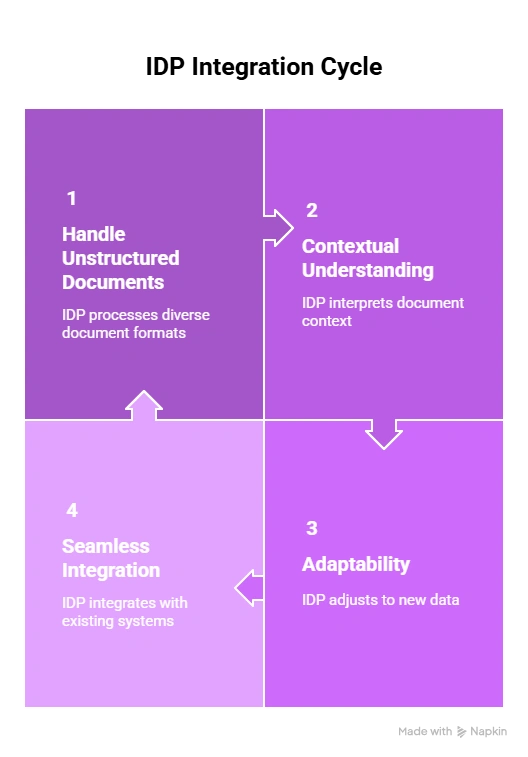

Wie bereits erwähnt, ist RPA bei der Bearbeitung von Versicherungsansprüchen äußerst effektiv für die Automatisierung strukturierter, regelbasierter Aufgaben. RPA ist jedoch mit natürlichen Einschränkungen verbunden. Es hat mit unstrukturierten Daten zu kämpfen, kann kaputt gehen, wenn sich ältere Systeme ändern, und erfordert eine umfangreiche Regelcodierung, um Ausnahmen zu behandeln. Das ist wo KI-gestützte intelligente Dokumentenverarbeitung (IDP) tritt als moderne Alternative ein.

Wie IDP die Lücke bei der Bearbeitung von Versicherungsansprüchen schließt

Unterstützt durch maschinelles Lernen IDP für die Bearbeitung von Schadensfällen geht über die Automatisierung hinaus. Es interpretiert, lernt und passt sich an. So schließt IDP die Lücke, die beim herkömmlichen RPA bei der Bearbeitung von Versicherungsansprüchen besteht:

- Umgang mit unstrukturierten Dokumenten: IDP extrahiert und interpretiert Text, Tabellen und Handschrift aus verschiedenen Dokumenten wie ACORD-Formularen, Rechnungen, Laborergebnissen und Reparaturschätzungen.

- Kontextuelles Verständnis: Mithilfe von NLP (Natural Language Processing) und ML erkennt IDP Absichten, Klauseln und Verpflichtungen — etwas, das RPA allein nicht erreichen kann.

- Anpassungsfähigkeit: Im Gegensatz zu statischen RPA-Regeln lernt IDP kontinuierlich aus neuen Dokumenten und Ausnahmen und verbessert so die Genauigkeit im Laufe der Zeit.

- Nahtlose Integration: IDP speist strukturierte Daten in nachgelagerte RPA-Bots oder Schadenmanagementsysteme (Guidewire, Duck Creek, Salesforce FSC) ein und sorgt so für eine reibungslose, durchgängige Pipeline.

Die Marktlücke: Warum IDP bei der Bearbeitung von Versicherungsansprüchen wichtig ist

Es gibt heute auch eine große Marktlücke. Gleichzeitig steigt die Nachfrage der Verbraucher nach Automatisierung. Studien zeigen das 73% der Versicherungskunden wünschen sich eine vollständig digitale Schadenbearbeitung, aber nur etwa 31 Prozent der Versicherer haben ihre Schadenplattformen ausreichend modernisiert, um dies zu gewährleisten. Diese Diskrepanz verdeutlicht, warum es nicht ausreicht, sich allein auf RPA zu verlassen. Versicherer benötigen IDP und KI-gestützte Lösungen, um den steigenden Erwartungen an Geschwindigkeit, Transparenz und digitale Erlebnisse gerecht zu werden.

Auf den Punkt gebracht

RPA bei der Bearbeitung von Versicherungsansprüchen ist nicht mehr optional; es ist eine Notwendigkeit für Spediteure, die Wert auf Geschwindigkeit, Genauigkeit und Effizienz legen. Die Ergebnisse sind bereits bewiesen: schnellere Abwicklungen, Verbesserungen bei der Betrugserkennung, enorme Senkung der Servicekosten und höhere Kundenzufriedenheitswerte.

Angesichts der Tatsache, dass 73% der Kunden digitale Forderungen stellen und nur 31% der Spediteure modernisiert haben, liegt der Wettbewerbsvorteil auf der Hand. Durch die Kombination von RPA mit IDP und agentischer KI können Versicherer endlich das Versprechen eines berührungslosen Schadens einlösen.

Häufig gestellte Fragen

Welche Teile von Schadensfällen kann RPA ohne Menschen automatisieren?

Dateneingabe, Eignungsprüfungen, Betrugserkennung, ACORD-Formularverarbeitung und Statusaktualisierungen.

Wie unterscheidet sich RPA von IDP und agentischer KI?

RPA verarbeitet regelbasierte Schritte, IDP interpretiert unstrukturierte Daten und agentische KI orchestriert den gesamten Arbeitsablauf.

Welche Schadenarten profitieren zuerst am meisten von RPA?

Rechnungen für Auto-, Immobilien- und Krankenversicherungsabrechnungen mit sich wiederholenden, umfangreichen Aufgaben.

Kann RPA ACORD-Formulare, Rechnungen und Fotos verarbeiten?

Ja. Bots verarbeiten strukturierte Formulare und integrieren sie in KI, um bildgestützte Beweise zu erhalten.

Wie gewährleistet RPA die Überprüfbarkeit und regulatorenfreundliche Protokolle?

Es erstellt mit Zeitstempeln versehene Protokolle über jede Aktion und bietet klare Audit-Trails.

Welche KPIs sollten Versicherer in Pilotprojekten verfolgen?

Zykluszeiten, Kosten pro Schadensfall, Betrugserkennungsraten, Fehlerquoten und Kundenzufriedenheit.

Wie lässt sich RPA in die wichtigsten Versicherungssysteme integrieren?

Über Konnektoren und APIs für Guidewire, Duck Creek, Salesforce FSC und ältere Systeme.

Wie werden Ausnahmen eskaliert und genehmigt?

Ausnahmen werden in Maker-Checker-Workflows an die Einsteller weitergeleitet.

Welche Rentabilitätsspannen sehen Versicherer bei RPA?

Der ROI variiert von 3x bis 11x, abhängig von der Art der Reklamation und dem Umfang der Automatisierung.

Wie geht RPA mit Datensicherheit und PII/PHI um?

Verschlüsselung, Zugriffskontrollen und SOC 2/HIPAA/DSGVO-konforme Workflows schützen sensible Daten

Priyanka Joy ist Produktautorin bei Infrrd und nähert sich Automatisierungstechnik wie eine neugierige Detektivin. Mit ihrer Liebe zur Recherche und zum Geschichtenerzählen verwandelt sie technische Tiefe in Klarheit. Wenn sie nicht schreibt, vertieft sie sich in Tanz, Theater oder schreibt an ihrer nächsten Erzählung.

Häufig gestellte Fragen

Software zur Überprüfung und Prüfung von Hypotheken ist ein Sammelbegriff für Tools zur Automatisierung und Rationalisierung des Prozesses der Kreditbewertung. Es hilft Finanzinstituten dabei, die Qualität, die Einhaltung der Vorschriften und das Risiko von Krediten zu beurteilen, indem sie Kreditdaten, Dokumente und Kreditnehmerinformationen analysiert. Diese Software stellt sicher, dass Kredite den regulatorischen Standards entsprechen, reduziert das Fehlerrisiko und beschleunigt den Überprüfungsprozess, wodurch er effizienter und genauer wird.

Eine QC-Checkliste vor der Finanzierung besteht aus einer Reihe von Richtlinien und Kriterien, anhand derer die Richtigkeit, Einhaltung und Vollständigkeit eines Hypothekendarlehens überprüft und verifiziert werden, bevor Mittel ausgezahlt werden. Sie stellt sicher, dass das Darlehen den regulatorischen Anforderungen und internen Standards entspricht, wodurch das Risiko von Fehlern und Betrug verringert wird.

KI verwendet Mustererkennung und Natural Language Processing (NLP), um Dokumente genauer zu klassifizieren, selbst bei unstrukturierten oder halbstrukturierten Daten.

Ja, IDP kann Dokumenten-Workflows vollständig automatisieren, vom Scannen über die Datenextraktion und Validierung bis hin zur Integration mit anderen Geschäftssystemen.

Eine QC-Checkliste vor der Finanzierung ist hilfreich, da sie sicherstellt, dass ein Hypothekendarlehen vor der Finanzierung alle regulatorischen und internen Anforderungen erfüllt. Das frühzeitige Erkennen von Fehlern, Inkonsistenzen oder Compliance-Problemen reduziert das Risiko von Kreditmängeln, Betrug und potenziellen rechtlichen Problemen. Dieser proaktive Ansatz verbessert die Kreditqualität, minimiert kostspielige Verzögerungen und stärkt das Vertrauen der Anleger.

Wählen Sie eine Software, die fortschrittliche Automatisierungstechnologie für effiziente Audits, leistungsstarke Compliance-Funktionen, anpassbare Audit-Trails und Berichte in Echtzeit bietet. Stellen Sie sicher, dass sie sich gut in Ihre vorhandenen Systeme integrieren lässt und Skalierbarkeit, zuverlässigen Kundensupport und positive Nutzerbewertungen bietet.